Central Bank Caution and Geopolitical Risks Shape Global Markets | Weekly Recap: 15 - 19 June 2026

Markets spent the third week of June navigating a combination of cautious central-bank messaging, uneven global growth and ongoing geopolitical uncertainty.

While expectations for eventual policy easing remain intact, policymakers continued emphasising patience, reinforcing the view that interest rates may remain restrictive for longer.

Against this backdrop, investors favoured selective areas of the market, with technology and Japanese equities outperforming while Europe, China and more defensive sectors struggled to gain traction.

Economic Overview

Markets entered the second half of June with investors navigating a combination of central-bank decisions, persistent geopolitical uncertainty, and signs that global growth momentum remained uneven.

While policymakers largely refrained from delivering major surprises, the tone from central banks reinforced expectations that monetary easing would proceed gradually, keeping financial conditions relatively restrictive.

In the US, the Fed maintained its cautious approach as policymakers continued to balance moderating inflation against a resilient labour market. Investors remained focused on the implications of higher policy rates for longer, particularly as recent data suggested that economic activity was slowing only gradually.

Across Europe, attention centred on the ECB’s policy outlook as officials continued to emphasise a data-dependent approach. In the UK, growth concerns persisted amid a backdrop of soft domestic activity and lingering uncertainty surrounding the pace of future BoE easing.

China continued to face challenges from weak domestic demand and ongoing pressures within the property sector. Although policymakers maintained supportive measures, investors remained unconvinced that stimulus efforts would be sufficient to generate a meaningful rebound in growth.

By contrast, Japan benefited from improving sentiment surrounding corporate profitability and expectations that the BoJ would continue its gradual normalisation process.

Equities, Bonds and Commodities

Performance across asset classes was mixed during the week, reflecting a market still balancing resilient growth pockets against restrictive financial conditions.

In the US, the Nasdaq Composite rose 0.69%, supported by large-cap semiconductor and computing names, while broader benchmarks were more mixed as investors reassessed the implications of higher-for-longer interest rates.

European equities struggled to maintain momentum as slower growth expectations weighed on sentiment, while the FTSE 100 underperformed amid weakness across defensive industries and energy-related names.

Japanese equities stood out as one of the stronger performers globally. The Nikkei 225 benefited from improving corporate earnings prospects and continued support from domestic investors.

Chinese equities remained under pressure as concerns surrounding growth and subdued consumer confidence continued to outweigh policy support measures.

Bond markets reflected a more restrictive policy backdrop. The US 2-year Treasury yield closed near 4.71%, while the 10-year yield remained around 4.26%, leaving the curve deeply inverted as investors prepared for prolonged policy restraint.

Commodity markets remained volatile. Brent crude settled near $80.05 per barrel after giving up earlier gains, while gold closed near $4,198.26 per ounce as fluctuations in real yields and a firmer US dollar influenced investor demand.

Overall, investors remained selective rather than broadly risk averse, favouring technology and earnings resilience while remaining cautious towards sectors exposed to slower growth and restrictive policy settings.

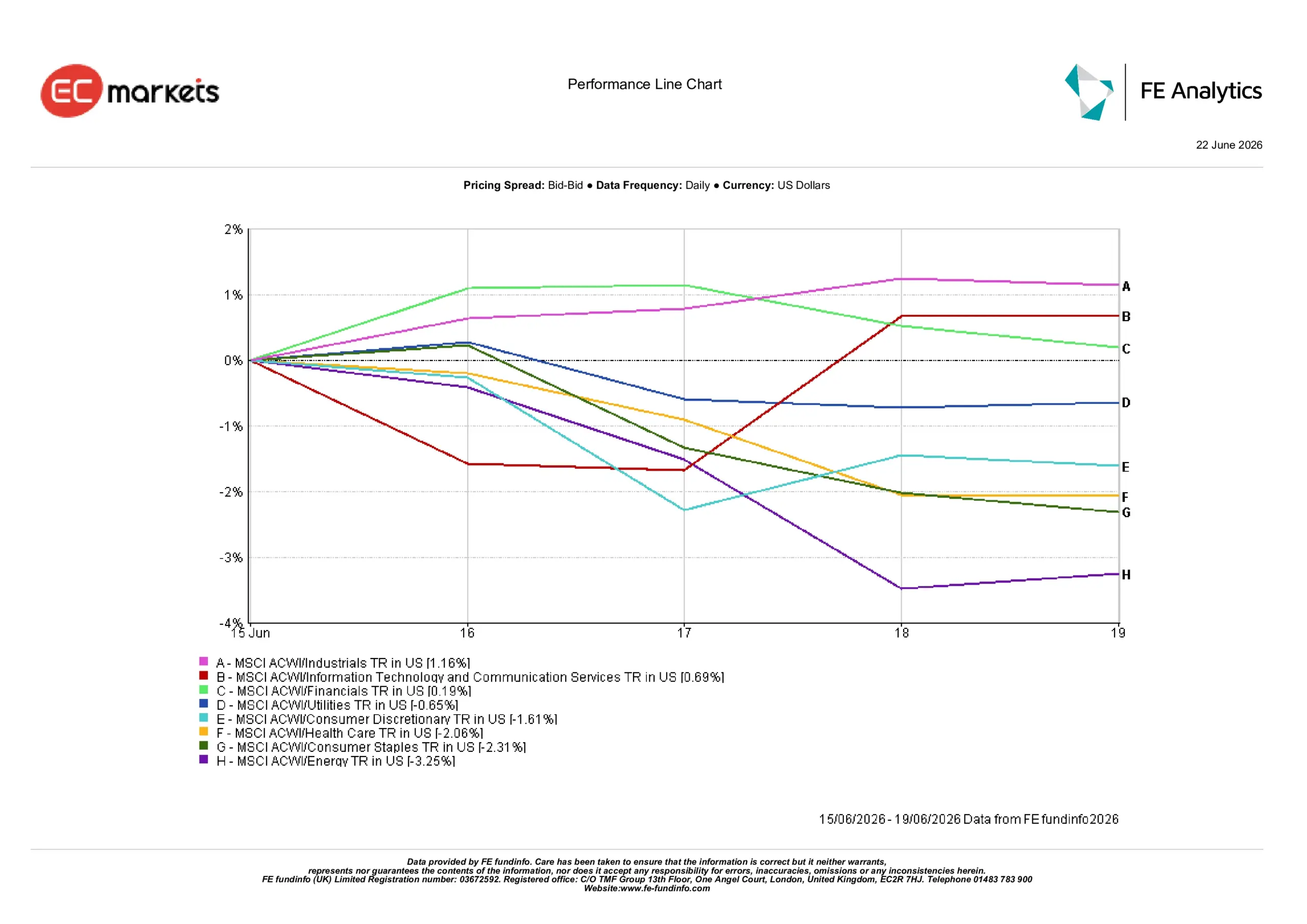

Sector Performance

Sector performance highlighted a notable shift in leadership as investors favoured areas with stronger earnings visibility while reducing exposure to sectors most vulnerable to slower economic growth and softer commodity prices.

Industrials delivered the strongest performance, rising 1.16% during the week. Continued investment spending and expectations that infrastructure-related activity would remain resilient supported the sector.

Information Technology and Communication Services gained 0.69%, reflecting continued interest in structural growth themes despite a more cautious market environment.

Financials rose 0.19% as elevated bond yields continued supporting banking profitability, although concerns surrounding slower economic growth limited stronger gains.

More defensive areas experienced weaker performance. Utilities declined 0.65%, while Consumer Discretionary fell 1.61% as investors became increasingly cautious regarding consumer spending trends. Health Care retreated 2.06%, and Consumer Staples declined 2.31%.

Energy recorded the weakest performance, falling 3.25% as softer oil prices and concerns surrounding global demand weighed on the sector.

Overall, sector performance highlighted a preference for earnings visibility and quality rather than a broad move into defensive positioning.

Sector Performance June 15th – 19th

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 19 June 2026.

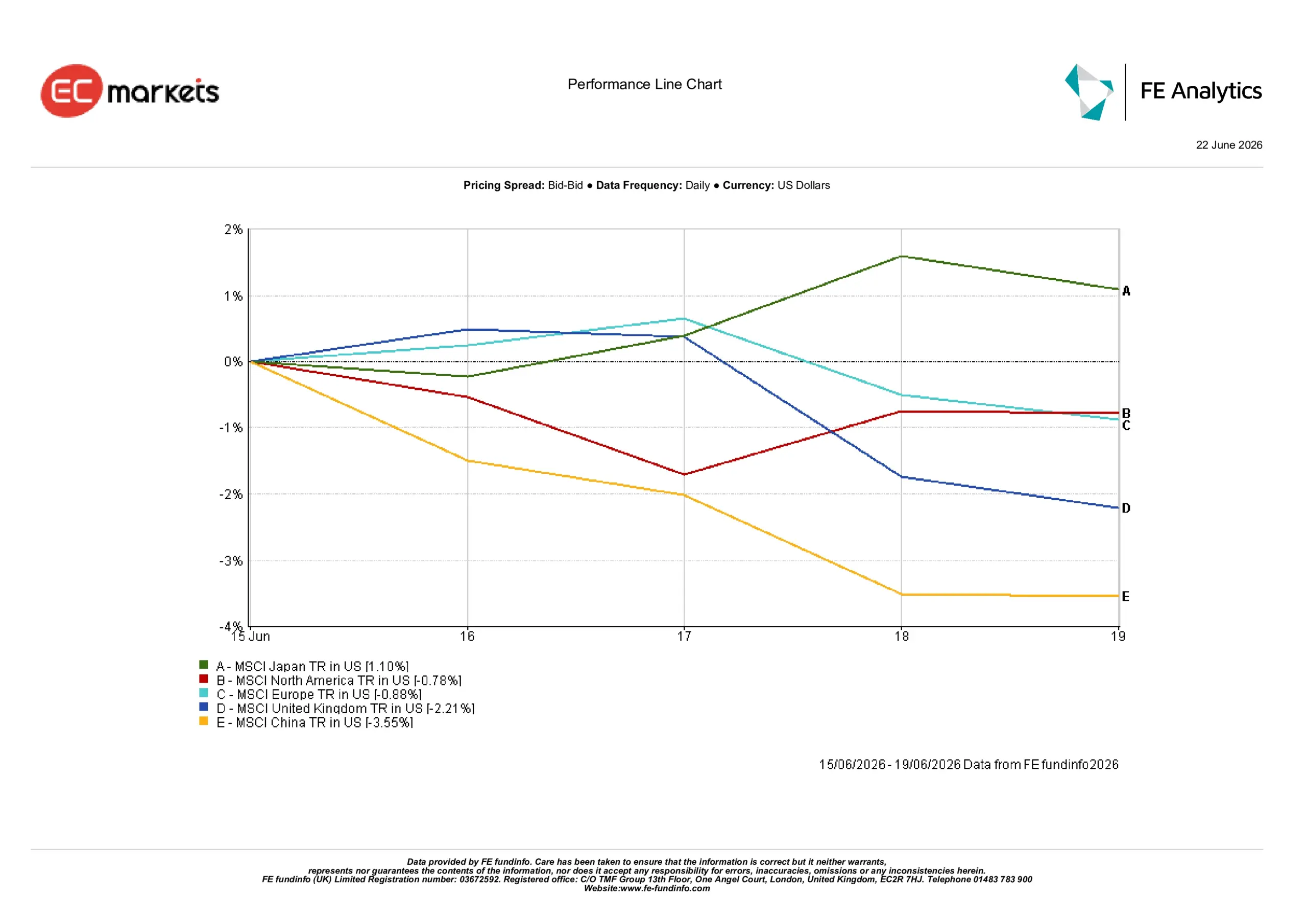

Regional Markets

Regional performance reflected significant divergence across global markets.

Japan emerged as the strongest-performing region, with the MSCI Japan Index advancing 1.10% in US dollar terms.

Support from corporate reforms, improving profitability and relatively stable domestic conditions helped Japanese equities outperform their peers.

North America declined 0.78%, reflecting a combination of elevated valuations and cautious sentiment surrounding the future path of US interest rates.

European equities also experienced weakness, with the MSCI Europe Index declining 0.88%. Sluggish economic growth and concerns surrounding industrial activity continued to weigh on investor confidence. The United Kingdom experienced a larger decline of 2.21%, reflecting the market’s exposure to weaker energy stocks and softer defensive sectors.

China remained the weakest-performing region, with the MSCI China Index falling 3.55%. Persistent concerns over domestic demand, ongoing pressures within the property sector and doubts regarding the effectiveness of policy support continued to weigh on sentiment.

Overall, regional performance highlighted the importance of domestic fundamentals and sector composition, with investors favouring markets supported by stronger earnings visibility and more resilient economic conditions.

Regional Performance June 15th – 19th

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 19 June 2026.

Currency Markets

Currency markets reflected the combination of higher US yields, cautious central-bank guidance and heightened geopolitical uncertainty.

EUR/USD declined from 1.1591 to 1.1469 as investors continued favouring the US dollar amid lingering uncertainty surrounding European growth prospects.

GBP/USD fell from 1.3414 to 1.3234 as concerns surrounding the UK economic outlook weighed on sentiment.

USD/JPY rose from 160.33 to 161.31, with yield differentials remaining a key driver of the pair.

GBP/JPY declined from 215.08 to 213.47 as sterling weakness outweighed softness in the Japanese yen.

Overall, currency markets continued to favour the US dollar as elevated Treasury yields and cautious central-bank guidance supported demand for US assets.

Outlook and The Week Ahead

Looking ahead, investors are likely to remain focused on incoming economic data and signals from central banks. Inflation releases, PMI surveys and labour-market indicators will be closely monitored for evidence regarding the underlying strength of global growth and the trajectory of monetary policy.

Markets will also continue to assess developments in the Middle East and their implications for energy markets and inflation expectations.

While expectations for eventual policy easing remain intact, central banks continue to emphasise caution. As a result, markets are likely to remain highly sensitive to economic surprises, inflation data and shifts in rate expectations. For now, investors appear focused on quality assets, earnings resilience and regions offering stronger growth visibility.