How Big a Threat Is the Debt Maturity Wall?

Higher interest rates are no longer just affecting consumers and housing markets. They are increasingly becoming a corporate balance-sheet story.

During the ultra-low-rate environment of 2020 and 2021, many companies borrowed heavily to lock in historically cheap financing. Now, much of that debt is approaching maturity at a time when borrowing costs remain significantly higher.

This refinancing cycle, often referred to as the “debt maturity wall”, is becoming an important theme for investors as markets assess how companies will manage higher funding costs over the coming years.

Understanding the Debt Maturity Wall

To understand why this matters, it helps to look at how corporate borrowing typically works.

Unlike a traditional mortgage, where debt is gradually repaid over time, companies often issue bonds or take loans with fixed maturity dates. When that debt matures, businesses usually refinance it by issuing new debt rather than repaying the full balance in cash.

This is standard practice in financial markets and allows companies to preserve liquidity for operations, investment, and expansion.

The challenge emerges when refinancing conditions become much more expensive than when the original debt was issued.

Companies that secured funding during the near-zero-rate environment now face the prospect of rolling over that debt at materially higher interest rates.

Why This Matters More Today

The macroeconomic backdrop has changed significantly since the start of the decade.

In 2020 and 2021, central banks maintained near-zero interest rates while injecting liquidity into financial markets. During that period, US investment-grade corporate bond yields were often close to 2% to 3%, allowing companies to borrow cheaply.

Today, borrowing conditions look very different.

As central banks maintain tighter policy to manage inflation, corporate financing costs have risen sharply. Recent estimates show investment-grade corporate bond yields moving closer to 5% or 6%.

That creates a major refinancing challenge because more than $1 trillion of US corporate debt is expected to mature annually between 2026 and 2028.

As this debt comes due, companies are effectively being forced to replace cheap capital with more expensive capital.

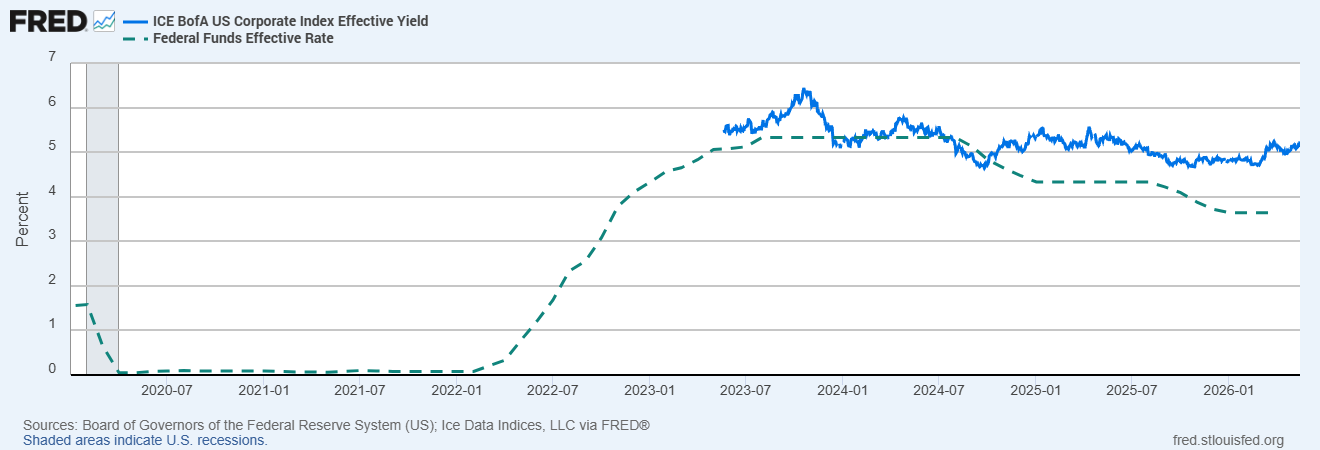

US Investment-Grade Corporate Bond Yields vs Federal Funds Rate

Sources: Board of Governors of the Federal Reserve System (US); Ice Data Indices, LLC via FRED®

A comparison of US investment-grade corporate bond yields and the Federal Funds Rate highlights how borrowing costs have risen sharply since the low-rate environment of 2020-2021, increasing refinancing pressure on corporate balance sheets.

What This Means For Profitability

Higher refinancing costs affect companies directly through rising interest expenses.

When debt is refinanced at higher rates, the cost of servicing that debt increases immediately, reducing profitability even if business activity remains relatively stable.

In practical terms, a company may continue generating similar revenue while seeing earnings weaken purely because financing costs have risen.

This can pressure profit margins, reduce cash flow flexibility and limit the amount of capital available for expansion, dividends or share buybacks.

A simple example highlights the scale of the issue.

If a company originally borrowed £100 million at 2.5% interest, the annual financing cost would be £2.5 million.

If that same debt must now be refinanced at 6.5%, the annual interest expense rises to £6.5 million, an additional £4 million in yearly costs created solely by higher interest rates.

Which Sectors Are Most Exposed?

Not all industries face the same refinancing risk.

Sectors with high capital requirements and larger debt loads are generally more sensitive to higher borrowing costs because they rely more heavily on external financing.

Commercial real estate and utilities are among the most exposed sectors, given their dependence on debt-funded infrastructure and property assets.

Highly leveraged growth companies that borrowed aggressively during the low-rate era may also face increasing pressure if interest expenses rise faster than revenues.

By contrast, companies with stronger balance sheets, lower leverage, and healthier free cash flow are typically better positioned to absorb higher financing costs.

Markets may also see greater divergence in credit quality as refinancing pressure increases.

Companies with weaker balance sheets could face credit-rating downgrades or widening corporate bond spreads, forcing investors to demand even higher returns to compensate for increased risk.

Why Markets Care About This Now

Financial markets are forward-looking, which means refinancing risks are often priced in long before debt actually matures.

Investors increasingly focus on balance-sheet quality because waiting until refinancing stress fully materialises may mean reacting too late.

As a result, markets are paying closer attention not only to earnings growth, but also to debt levels, interest coverage ratios, and refinancing schedules.

Concerns around refinancing risk can influence equities, credit markets, and broader risk sentiment simultaneously.

If investors believe a sector is approaching a refinancing cliff, those assets may come under pressure well before refinancing activity peaks.

Bottom Line

The debt maturity wall represents one of the key medium-term risks created by the higher-for-longer rate environment.

While many companies successfully locked in cheap financing during the low-rate era, refinancing that debt at materially higher rates may pressure profitability, investment activity and overall financial stability over the coming years.

For investors, understanding corporate balance sheets and refinancing exposure is becoming increasingly important in navigating today’s macro environment.