Growth Resilience Drives Equity Rotation as Energy Weakness Eases Inflation Pressure | Weekly Recap: 04 - 08 May 2026

Markets moved toward a more constructive tone last week, as resilient growth and moderating inflation supported a gradual rotation back into risk assets.

Economic Overview

Markets spent the week reassessing the balance between slowing inflation and still-resilient growth, increasingly leaning toward a soft-landing narrative rather than an imminent downturn.

The shift was not driven by a sharp improvement in data, but by growing confidence that major economies are slowing gradually, not collapsing.

In the US, labour-market data remained central. Job openings held near 6.9 million, while Non-Farm Payrolls showed +115,000 jobs added, with unemployment steady around 4.3%. Wage growth moderated only slightly.

The implication was clear:

- Demand remains strong enough to support growth

- But not strong enough to force tighter policy

The ISM Services PMI also stabilised, reinforcing resilience in domestic demand despite restrictive conditions.

Outside the US, policy divergence remained in focus. The RBA raised rates to 4.35%, signalling that inflation risks remain a priority for some central banks.

Across Europe and the UK, growth remained softer, limiting upside in regional markets.

In Asia, Japan benefited from improved sentiment and a weaker yen, while China’s recovery remained uneven, particularly across domestic demand.

Overall, markets increasingly priced moderation, not deterioration.

Markets Overview

Equities

Global equities moved higher, with leadership concentrated in growth sectors and US markets.

The S&P 500 rose ~2.4%, while the Nasdaq gained ~3.5%, driven by continued demand for technology and AI-linked exposure.

European markets participated but lagged, while Asia was more mixed, with Japan outperforming and China trailing.

Bonds

Bond markets reflected improving confidence in the soft-landing narrative.

The US 10-year yield eased from ~4.45% to ~4.36%, while the 2-year also moved lower, signalling reduced pressure on policy expectations.

European yields followed a similar pattern.

Commodities

Commodities diverged. Brent crude briefly moved above $114 before softening into the end of the week as demand expectations cooled and risk premia eased.

Gold traded unevenly near $4,500, initially weakening on higher real yields before stabilising.

Overall, cross-asset performance reflected growing comfort with slower, but still positive growth.

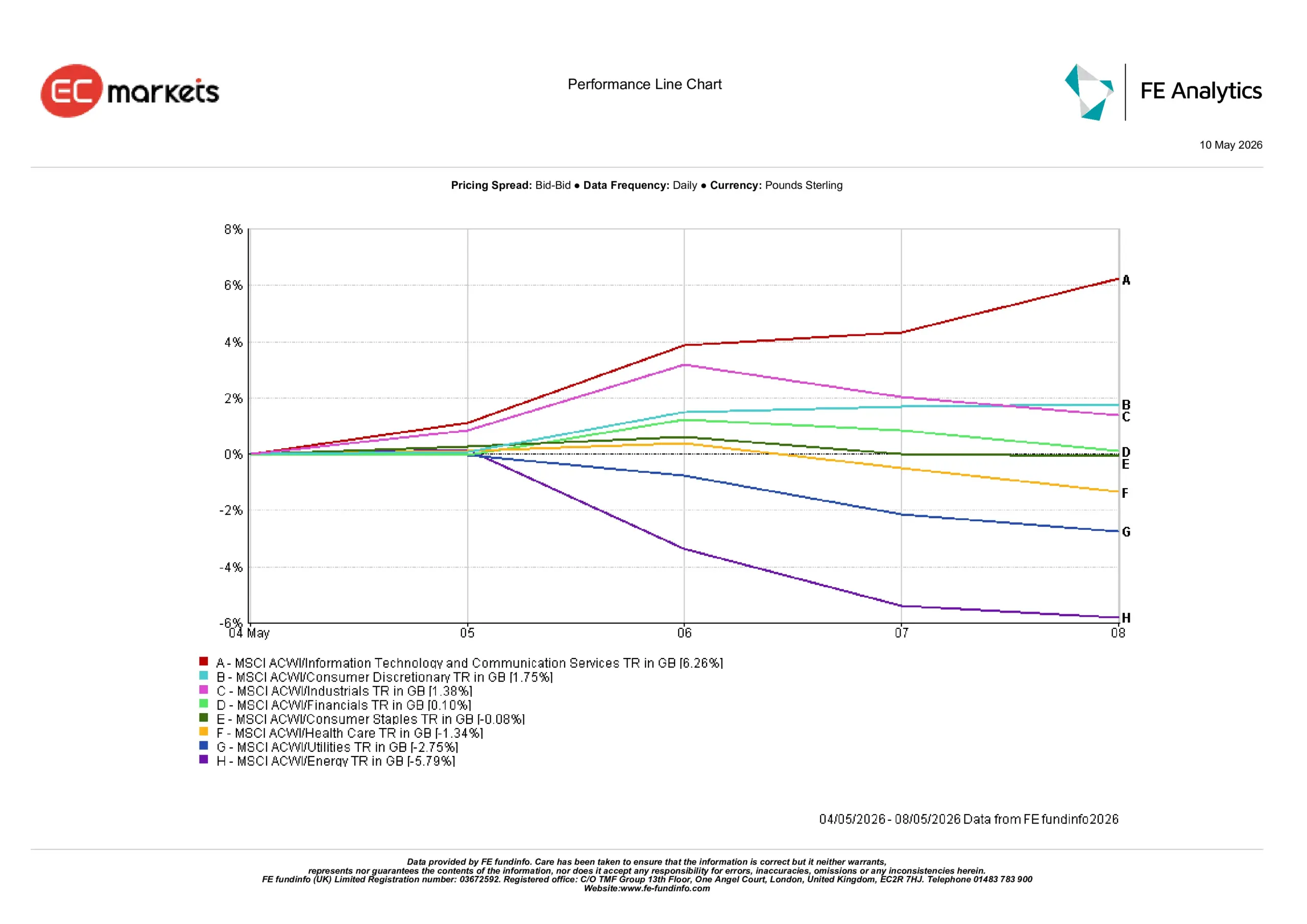

Sector Insights

Sector leadership strongly reflected renewed investor preference for growth and cyclical resilience over defensive positioning.

Technology and Communication Services led global sector performance, rising 6.26% during the week as easing bond yields and resilient US data improved sentiment toward duration-sensitive growth sectors. AI-related positioning also remained a significant driver of flows into large-cap technology exposure.

Consumer Discretionary performed strongly, gaining 1.75% as investors became more confident that consumer demand remains relatively resilient despite restrictive financial conditions. Industrials rose 1.38%, reflecting improving confidence around broader economic activity and stabilising growth expectations.

Financials delivered more modest gains of 0.10%, with investors balancing the support from elevated yields against concerns that tighter financial conditions could eventually weigh on credit growth.

Defensive sectors lagged the broader market move. Utilities declined 2.75%, while Healthcare fell 1.34%, as investors rotated away from bond-proxy sectors and back toward higher-beta growth exposure. Consumer Staples slipped marginally by 0.08%.

Energy was the weakest-performing sector by a wide margin, falling 5.79% during the week as oil prices softened into the end of the period and geopolitical risk premia eased.

Overall, sector rotation continued to reflect growing confidence in a soft-landing environment, although positioning remained selective rather than fully risk-on.

Sector Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 8 May 2026.

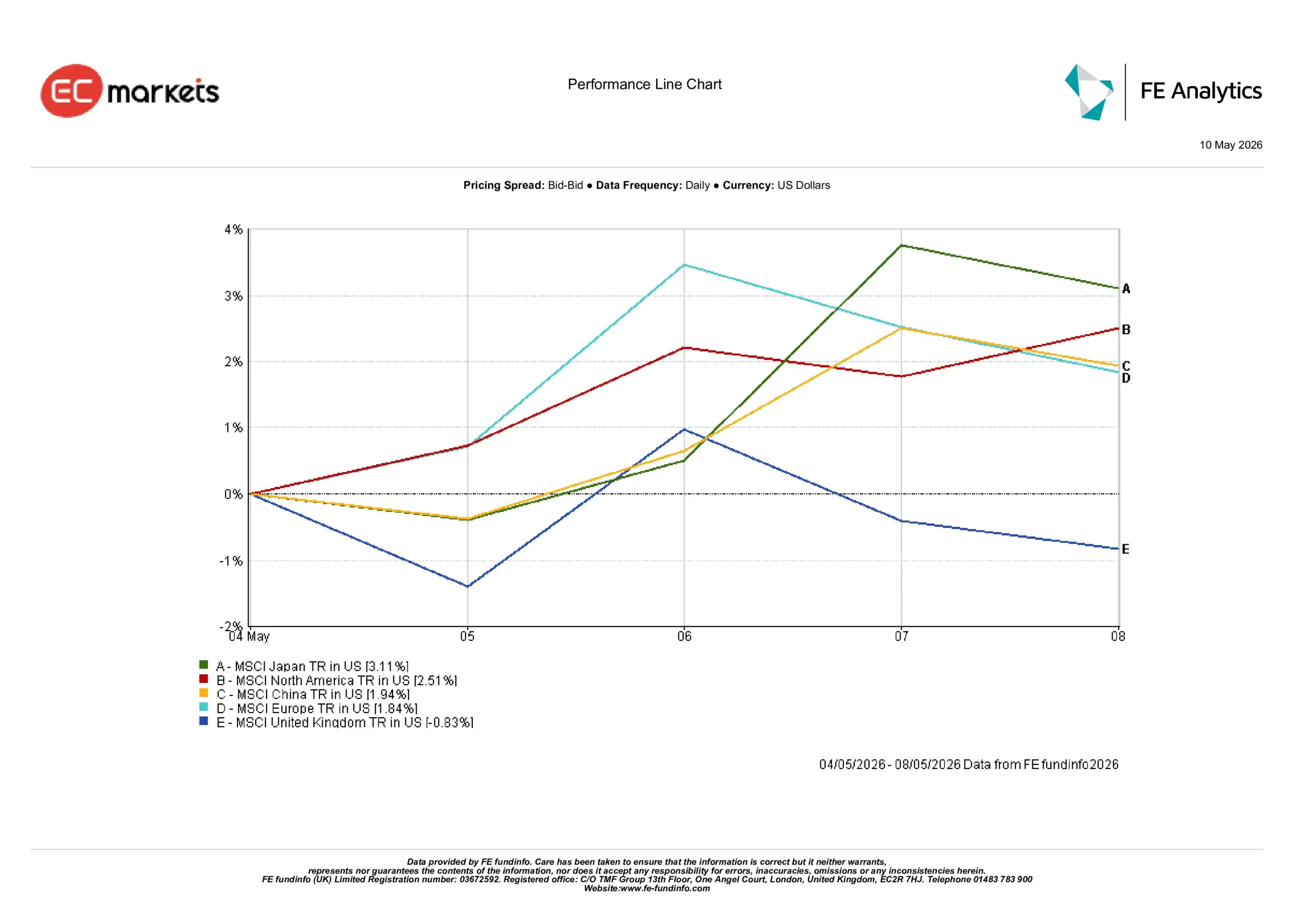

Regional Insights

Regional performance reinforced the dominance of growth-oriented and externally exposed markets during the week, with investors continuing to favour regions benefiting most from resilient global demand and technology leadership.

Japan was the strongest-performing major region, with MSCI Japan rising 3.11% in USD terms as improving global sentiment and continued yen weakness supported exporters and cyclical sectors.

MSCI North America gained 2.51%, supported by stronger US economic data and renewed leadership from large-cap technology. Continued resilience in US growth expectations remained a key driver of capital flows into the region.

MSCI China rose 1.94% during the week, recovering alongside broader global risk appetite. However, investors remained cautious around the sustainability of China’s domestic recovery, particularly across property and consumer demand trends.

MSCI Europe gained 1.84%, reflecting stabilising sentiment but also continued concerns surrounding weaker regional growth dynamics and softer economic momentum.

MSCI United Kingdom declined 0.83%, making it the weakest major region during the week. The weaker performance largely reflected the market’s heavier exposure to energy- and commodity-linked sectors following the decline in oil prices.

Overall, regional divergence continued to reflect differences in sector composition, policy flexibility, and sensitivity to global growth expectations.

Regional Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 8 May 2026.

Currency Markets

FX markets reflected a moderate unwind of defensive dollar positioning.

- EUR/USD: Strengthened ~0.7%, supported by stabilising sentiment and softer USD.

- GBP/USD: Rose ~1.5%, helped by improving risk appetite and firmer UK expectations.

- USD/JPY: Fell ~1.5%, as yields eased and the yen recovered modestly.

Commodity currencies remained volatile, with the AUD reacting to the RBA hike and CAD pressured by softer oil prices.

Overall, FX moves aligned with improving risk sentiment and easing inflation pressure.

Looking Ahead

The key focus now is whether inflation continues to moderate enough to allow central banks greater flexibility later in the year.

Upcoming inflation data, labour-market releases, and central bank communication will remain the primary drivers of market direction.

Oil also remains critical, any renewed strength could quickly reintroduce inflation concerns.

For now, markets continue to interpret weaker data as moderation, not contraction.

The key question:

Is this the start of a sustained recovery, or simply a more stable phase within a still-fragile environment?