Inflation Repricing and Rising Yields Reshape Global Market Sentiment | Weekly Recap: 11 - 15 May 2026

Markets moved into a more cautious phase last week as persistent inflation, rising sovereign yields and renewed energy volatility challenged the softer “goldilocks” narrative that had supported risk appetite through April and early May.

While economic activity remained relatively resilient across major economies, stronger-than-expected US inflation data and surging oil prices forced investors to reassess the likelihood of near-term policy easing.

The result was a broad repricing across bonds, currencies and equity sectors, with markets increasingly focused on inflation persistence rather than growth optimism alone.

Economic Overview

Markets moved away from the relatively comfortable “soft landing” narrative that had supported risk appetite through April and early May. Instead, investors increasingly focused on inflation persistence, rising sovereign yields and the growing possibility that central banks may need to keep policy restrictive for longer than previously expected.

The main catalyst came from the United States, where April inflation data surprised to the upside. Headline CPI rose 0.6% month-on-month and 3.8% year-on-year, while core CPI increased 0.4% on the month and 2.8% annually. Producer prices also accelerated sharply, with PPI rising 6.0% year-on-year.

Importantly, inflation pressures appeared alongside still-resilient activity rather than signs of economic weakness. Retail sales rose 0.5%, industrial production increased 0.7%, and jobless claims remained relatively low near 211,000.

Equities, Bonds and Commodities

Equities

Equity-market performance became more selective as inflation concerns intensified throughout the week. US indices initially remained relatively resilient due to ongoing support from large-cap technology and AI-related sectors, although sentiment weakened following the inflation data and subsequent rise in bond yields.

The S&P 500 ended the week broadly flat, while the Nasdaq Composite and Dow Jones Industrial Average both moved modestly lower. European equities underperformed more clearly.

The STOXX Europe 600 declined around 0.9%, while Germany’s DAX and France’s CAC 40 posted sharper losses as higher yields and weaker regional growth expectations weighed on sentiment. The FTSE 100 also weakened, although its heavier exposure to energy-linked companies helped limit some downside pressure.

Asian markets also struggled. Japan’s Nikkei 225 fell more than 2% as higher global yields pressured growth-oriented sectors, while both the Hang Seng and Shanghai Composite ended the week lower as investors remained cautious around domestic demand conditions and broader trade uncertainty.

Bonds

Bond markets experienced some of the sharpest repricing of the week. The US 10-year Treasury yield climbed toward 4.6%, while the 2-year yield moved above 4.0% as investors adjusted Fed expectations higher.

Germany’s 10-year Bund yield rose above 3.1%, UK 10-year gilt yields approached 5.1%, and Japanese government-bond yields reached multi-decade highs near 2.7%.

The move reinforced the growing market view that central banks may need to keep policy restrictive for longer as inflation pressures remain persistent.

Commodities

Commodity markets became central to the macro narrative. Oil prices surged throughout the week as geopolitical risks and supply concerns intensified, reinforcing inflation fears across asset classes.

Gold, however, fell roughly 2.5% toward $4,557 per ounce as rising real yields and a firmer US dollar reduced demand for non-yielding defensive assets.

Overall, cross-asset performance reflected a market reassessing the balance between resilient growth and persistent inflation rather than pricing a straightforward risk-on environment.

Sector Performance

Sector performance reflected a clear rotation toward inflation-hedged and defensive areas as rising yields and higher energy prices weighed on broader risk appetite.

Energy was the strongest-performing sector during the week, rising 4.75% as crude oil prices surged amid renewed geopolitical concerns and supply risks. Consumer Staples and Health Care also outperformed, gaining 3.44% and 2.98% respectively, as investors rotated toward sectors viewed as more resilient during periods of inflation uncertainty and market volatility.

Financials delivered a more modest gain of 1.12%, supported by higher yields but constrained by concerns that tighter financial conditions could eventually pressure economic activity and credit growth.

Information Technology and Communication Services still finished higher overall, gaining 1.71%, although momentum weakened later in the week as rising bond yields pressured duration-sensitive growth sectors.

More economically sensitive Industrials declined 0.76%, reflecting growing caution around the global growth outlook. Utilities also underperformed, falling 1.58% as rising sovereign yields reduced demand for traditional bond-proxy sectors.

Overall, sector rotation suggested that investors increasingly prioritised inflation resilience and defensive earnings visibility over cyclical growth exposure.

Sector Performance May 11th – 15th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 15 May 2026.

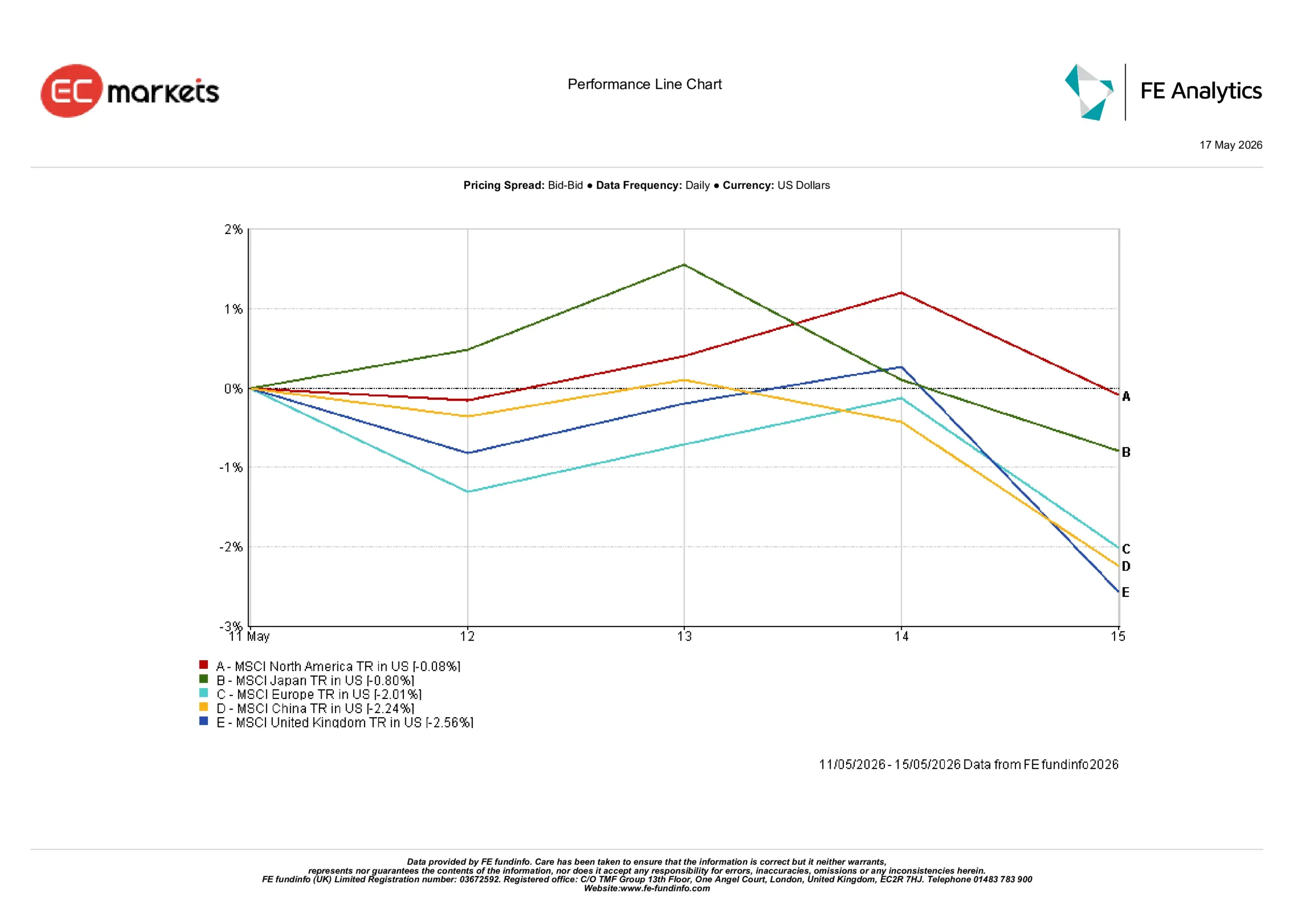

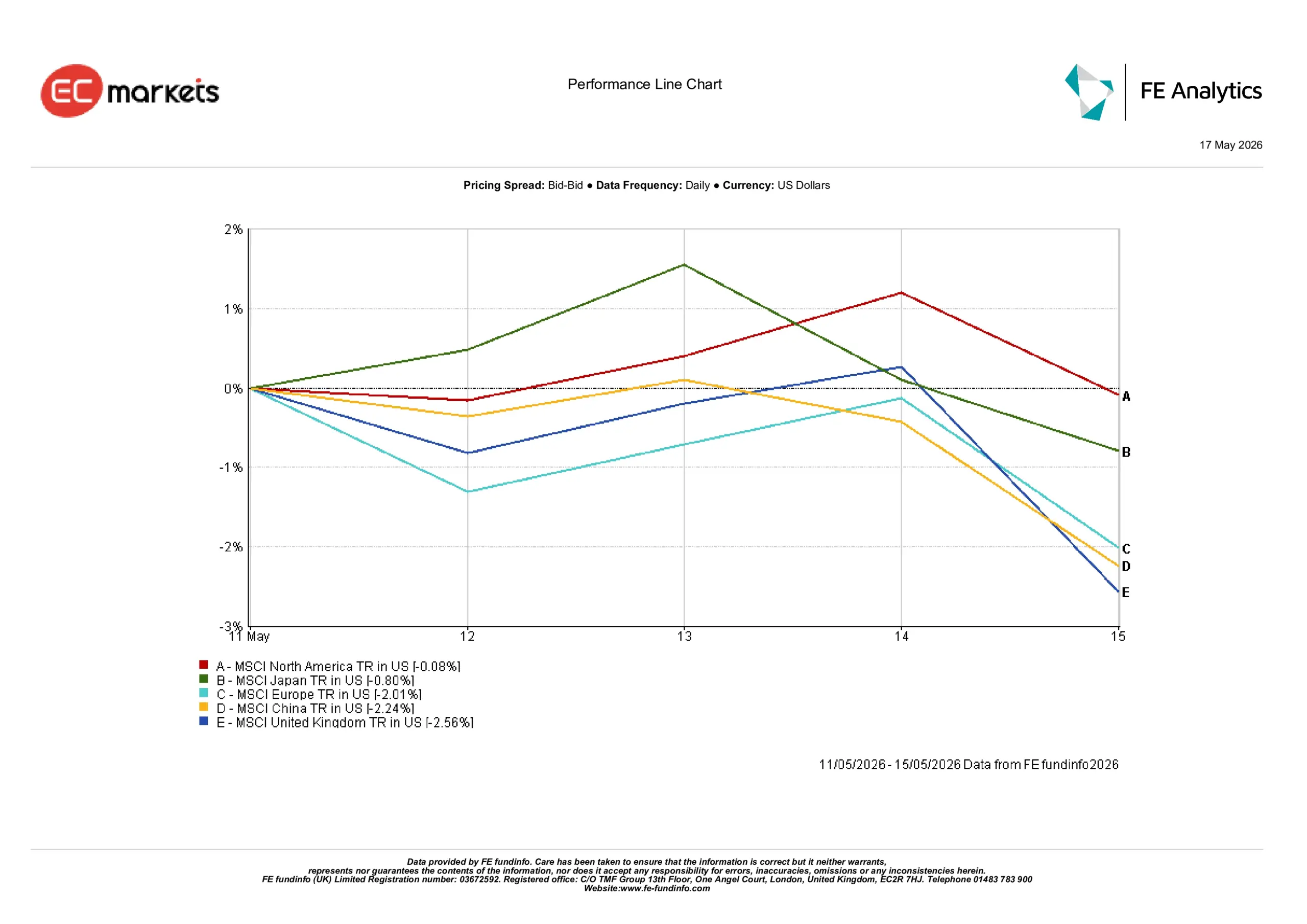

Regional Markets

Regional divergence became more pronounced as rising sovereign yields and inflation concerns reshaped global equity performance.

North America proved the most resilient major region, declining just 0.08% as large-cap technology strength helped cushion the impact of rising Treasury yields and tighter financial conditions. Japan also held up relatively well, with MSCI Japan falling 0.80% in USD terms as continued yen weakness reduced returns for international investors.

Elsewhere, losses were more pronounced. MSCI Europe declined 2.01% as weaker regional growth momentum combined with higher yields to weigh on sentiment. MSCI China fell 2.24%, with investors remaining cautious around the pace and sustainability of the country’s domestic recovery amid continued demand concerns.

The UK was the weakest-performing major region, declining 2.56%. The move reflected a combination of political uncertainty, sterling weakness and pressure across several of the market’s largest sectors.

Overall, global capital continued favouring markets with stronger technology leadership and relative economic resilience, while regions more exposed to weaker growth dynamics and currency pressure lagged.

Regional Performance May 11th – 15th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 15 May 2026.

Currency Markets

FX markets reflected a decisive move back toward US dollar strength as rising Treasury yields and shifting rate expectations supported defensive positioning.

EUR/USD weakened steadily during the week, falling from around 1.1783 to approximately 1.1626 by Friday as softer eurozone growth expectations and widening rate differentials weighed on the single currency.

Sterling also experienced heavy selling pressure, with GBP/USD declining from roughly 1.3611 to near 1.3325 as political uncertainty compounded broader dollar strength.

The yen remained under pressure despite rising Japanese bond yields. USD/JPY climbed from around 157.18 to approximately 158.77 during the week as higher US yields continued dominating relative-rate dynamics. GBP/JPY moved lower from around 213.93 to 211.54, reflecting sterling weakness against both the dollar and yen.

Overall, FX markets reinforced the dominant macro narrative seen across other asset classes, with markets rewarding yield advantage and economic resilience while currencies linked to weaker growth dynamics struggled to attract sustained support.

Outlook and The Week Ahead

Looking ahead, markets are likely to remain highly sensitive to incoming inflation and activity data following the sharp repricing seen in rates markets this week. Investors will closely monitor whether recent inflation pressures remain concentrated within energy markets or begin feeding more broadly into wages and consumer prices.

Upcoming CPI releases from Canada and the UK will be important for global rate expectations, while flash PMI data across the US, Europe and Asia will help investors assess whether tighter financial conditions are beginning to weigh more meaningfully on economic momentum.

Bond markets are also likely to remain central to overall sentiment. Further upward pressure in sovereign yields could continue challenging equity valuations, particularly within rate-sensitive growth sectors. At the same time, any stabilisation in oil prices or moderation in inflation expectations could help ease some of the pressure that emerged across global markets during the second half of the week.

For now, investors appear to be moving into a more cautious phase of the macro cycle, where inflation persistence and financial conditions matter more than simple growth resilience alone.