Record Highs Despite Inflation Concerns | Weekly Recap: 25 - 29 May 2026

Markets finished May on a strong footing as easing geopolitical tensions, falling oil prices, and continued confidence in corporate earnings helped support risk sentiment across global asset classes.

While inflation remained elevated and US growth data softened, investors largely looked through the macro headwinds. Instead, attention remained firmly focused on resilient earnings, artificial intelligence investment and signs that tensions surrounding the Strait of Hormuz may be easing following progress in US-Iran negotiations.

The result was another positive week for risk assets, with equities continuing to push higher, bond yields easing from recent highs and energy markets unwinding a significant portion of their geopolitical risk premium.

However, with inflation still above central-bank targets and June policy meetings approaching, questions around the sustainability of the rally remain firmly in focus.

Economic Overview

Economic data throughout the week painted a mixed picture of slowing growth alongside persistent inflation pressures.

In the United States, first-quarter GDP growth was revised lower to 1.6% annualised from 2.0% previously, signalling some moderation in economic momentum. At the same time, April Core PCE inflation remained elevated at 3.3% year-on-year, while headline PCE inflation held near 3.8%, its highest level since May 2023.

Labour market conditions remained relatively stable, with initial jobless claims rising to 215,000. Consumer confidence softened modestly, while personal income was broadly unchanged and the savings rate fell to a four-year low, highlighting growing pressure on household finances despite continued economic resilience.

Eurozone economic sentiment improved modestly during May, although attention remained focused on upcoming inflation data and the ECB’s June policy decision.

China’s economic recovery remained under pressure, with foreign direct investment contracting 10.3% year-to-date in April.

Japan delivered a more encouraging set of economic indicators. Industrial production rose 0.8% during April, while retail sales increased 2.1% year-on-year, supporting the view that domestic demand remains relatively resilient despite softer inflation trends.

In Australia, headline inflation eased to 4.2% year-on-year in April, coming in below expectations. Meanwhile, the Reserve Bank of New Zealand left its official cash rate unchanged at 2.25%, while maintaining a relatively hawkish stance as policymakers continued monitoring inflation risks.

Equities, Bonds, and Commodities

Equities

US equities continued their strong advance throughout the week, with all three major indices closing at fresh record highs.

The S&P 500 gained 1.43% to finish at 7,580.06, extending its winning streak to nine consecutive weeks and ending May up 5.0%. The Nasdaq Composite rose 2.77% for the week, delivering its strongest monthly performance of 2026 with an 8.0% gain in May. Meanwhile, the Dow Jones Industrial Average advanced 2.94%, closing above 51,000 for the first time and finishing the month nearly 3.0% higher.

Technology remained the primary market driver as continued enthusiasm surrounding artificial intelligence investment and infrastructure spending supported sentiment across the sector.

Corporate earnings remained broadly supportive. Approximately 84% of S&P 500 companies reporting first-quarter results exceeded analyst expectations, while overall earnings growth continued significantly outperforming forecasts.

European equities delivered a more mixed performance. While sentiment improved alongside easing geopolitical tensions, slower growth momentum and inflation concerns continued limiting upside across major regional indices.

Bonds

Bond markets reflected a more balanced assessment of inflation and growth risks during the week.

The yield on the US 10-year Treasury note declined from 4.56% to 4.45%, while the 2-year Treasury yield fell from 4.13% to 3.98%.

Despite inflation remaining elevated, investors increasingly focused on softer growth data and signs that economic momentum may be moderating. The decline in yields provided additional support for risk assets, particularly growth-oriented sectors such as technology.

Overall, bond markets continued balancing persistent inflation pressures against signs of slowing economic growth.

Commodities

Oil prices recorded sharp declines during the week as investors responded to reports of progress toward a ceasefire extension between the United States and Iran and the potential reopening of the Strait of Hormuz.

WTI fell approximately 9.0% to $87.90 per barrel, while Brent crude recorded its largest monthly decline since 2020, falling 1.08% to settle at $91.70.

Gold prices rose 0.75% during the week to approximately $4,544 as investors balanced easing geopolitical tensions against persistent inflation concerns and uncertainty surrounding future monetary policy.

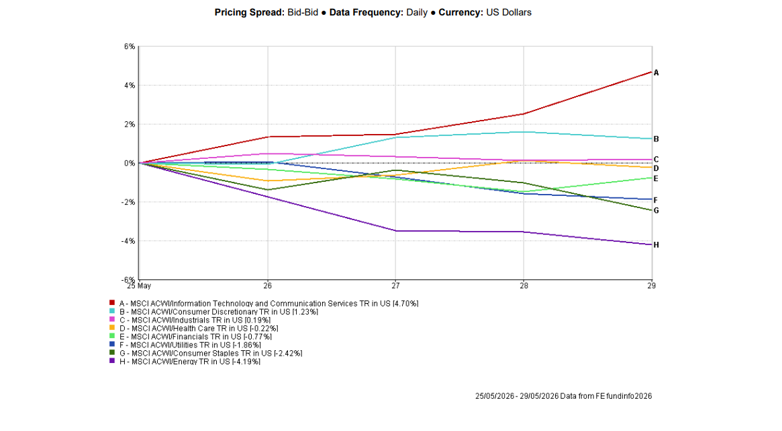

Sector Performance

Sector performance highlighted the market’s continued preference for growth-oriented assets.

Information Technology and Communication Services was the strongest-performing sector globally, rising 4.70% during the week as AI-related optimism and strong earnings continued supporting sentiment.

Consumer Discretionary gained 1.23%, while Industrials advanced 0.19%.

Meanwhile, Energy was the weakest-performing sector, falling 4.19% as oil prices recorded their sharpest decline in months. Consumer Staples declined 2.42%, while Utilities, Financials and Healthcare fell 1.86%, 0.77% and 0.22% respectively.

Overall, technology remained the clear market leader as investors continued favouring AI-related growth themes.

Sector Performance May 25th – 29th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 29 May 2026.

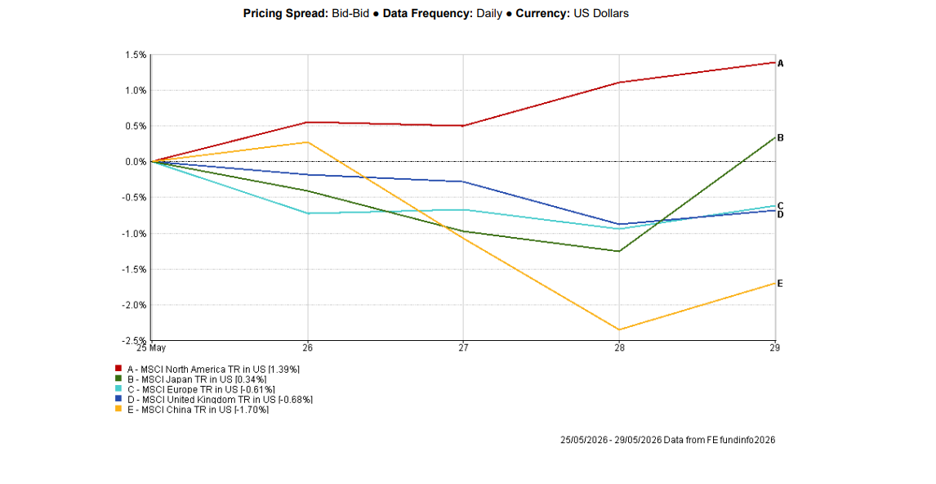

Regional Markets

Regional performance remained mixed, with North America continuing to lead global equity markets.

MSCI North America rose 1.39% as record highs across US equities supported broader regional performance.

Japan gained 0.34% following stronger industrial production and retail sales data, while Europe and the United Kingdom declined 0.61% and 0.68% respectively amid ongoing growth concerns and cautious positioning ahead of key inflation releases.

China remained the weakest major region, falling 1.70% as investors continued responding to disappointing economic data and ongoing concerns surrounding domestic demand and investment activity.

Regional Performance May 25th – 29th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 29 May 2026.

Currency Markets

Currency markets reflected improving risk sentiment and reduced demand for traditional safe-haven assets throughout the week.

The US dollar index (DXY) fell 0.31% to 99.00, recording a second consecutive weekly decline as easing geopolitical tensions surrounding a potential US-Iran ceasefire reduced defensive demand for the currency.

EUR/USD gained approximately 0.2% during the week, closing near 1.1662 after recovering from a multi-week low of 1.1576. The move higher was primarily driven by broader dollar weakness as investors reassessed safe-haven positioning.

Sterling also benefited from softer dollar sentiment, with GBP/USD closing near 1.3461 after trading between 1.3291 and 1.3575 throughout the week. While UK economic data remained mixed, the pound found support as Treasury yields moved lower and risk appetite improved.

Meanwhile, USD/JPY remained elevated near 159.32, with the yen continuing to face pressure from the significant interest-rate differential between the United States and Japan. The pair traded close to the 160 level that previously prompted intervention from Japanese authorities, highlighting ongoing sensitivity around currency markets.

Overall, FX markets were driven by easing geopolitical tensions, softer Treasury yields and shifting central-bank expectations.

Outlook and The Week Ahead

Markets now move into an important week dominated by labour-market data, inflation expectations and continued scrutiny of economic growth momentum.

Investors will closely monitor US Nonfarm Payrolls, ISM Manufacturing and Services PMIs, JOLTS Job Openings and eurozone inflation data for further signals on the health of the global economy and the outlook for central-bank policy.

Markets will also be watching developments surrounding the proposed SpaceX IPO, which could become the largest public offering in history and is expected to attract significant investor attention ahead of its anticipated June listing.

While record highs and strong earnings continue supporting risk appetite, inflation remains above target and growth momentum is showing signs of slowing. With June’s central-bank meetings approaching, upcoming labour-market and inflation data will be critical in determining whether the rally can extend further into the summer.