How Investors Value Gold: Why Gold Doesn't Produce Cash Flow

Understanding how investors value gold begins with recognising that it is fundamentally different from shares or bonds. Investors usually value companies by analysing earnings, free cash flow, dividends and returns on capital. Gold generates no profits, dividends or cash flow, yet it has remained one of the world’s most important investment assets for centuries.

Looking Beyond Traditional Valuation

Investors usually value companies by analysing earnings, free cash flow, dividends and returns on capital. Gold is fundamentally different. It generates no profits, dividends or cash flow, yet it has remained one of the world’s most important investment assets for centuries.

If gold produces no income, how do investors assess whether it is expensive or cheap? Rather than valuing gold like a business, professional investors analyse a broader macroeconomic framework that includes real interest rates, inflation expectations, US dollar movements, central bank demand and investor sentiment.

How Investors Value Gold

Owning shares in a company means owning part of a business capable of generating future cash flows, allowing investors to estimate its intrinsic value using methods such as discounted cash flow analysis or earnings multiples.

Gold offers no such cash flows. Instead, its value derives from its scarcity, liquidity and long history as a store of value. Rather than analysing earnings or profit margins, investors focus on the macroeconomic conditions that influence demand.

Understanding Opportunity Cost

One of the most important concepts when analysing gold is opportunity cost.

Because gold produces no income, investors compare it with assets that do generate returns, such as savings accounts or government bonds. When interest rates rise, holding gold becomes relatively less attractive. Conversely, when rates fall, the opportunity cost of owning gold declines, making the metal comparatively more appealing.

For this reason, changes in interest rates often influence investor demand for gold.

Real Yields Matter More Than Interest Rates

Professional investors often pay closer attention to real interest rates than nominal interest rates.

Real yields measure the return investors receive after accounting for inflation, providing a clearer picture of the purchasing power generated by fixed income investments.

This distinction matters because investors are not simply comparing gold with bond yields. They are comparing gold with inflation adjusted returns available elsewhere.

Historically, falling or negative real yields have often supported higher gold prices because investors receive relatively little real return from holding bonds. Rising real yields have generally created headwinds for gold by increasing the attractiveness of income producing assets.

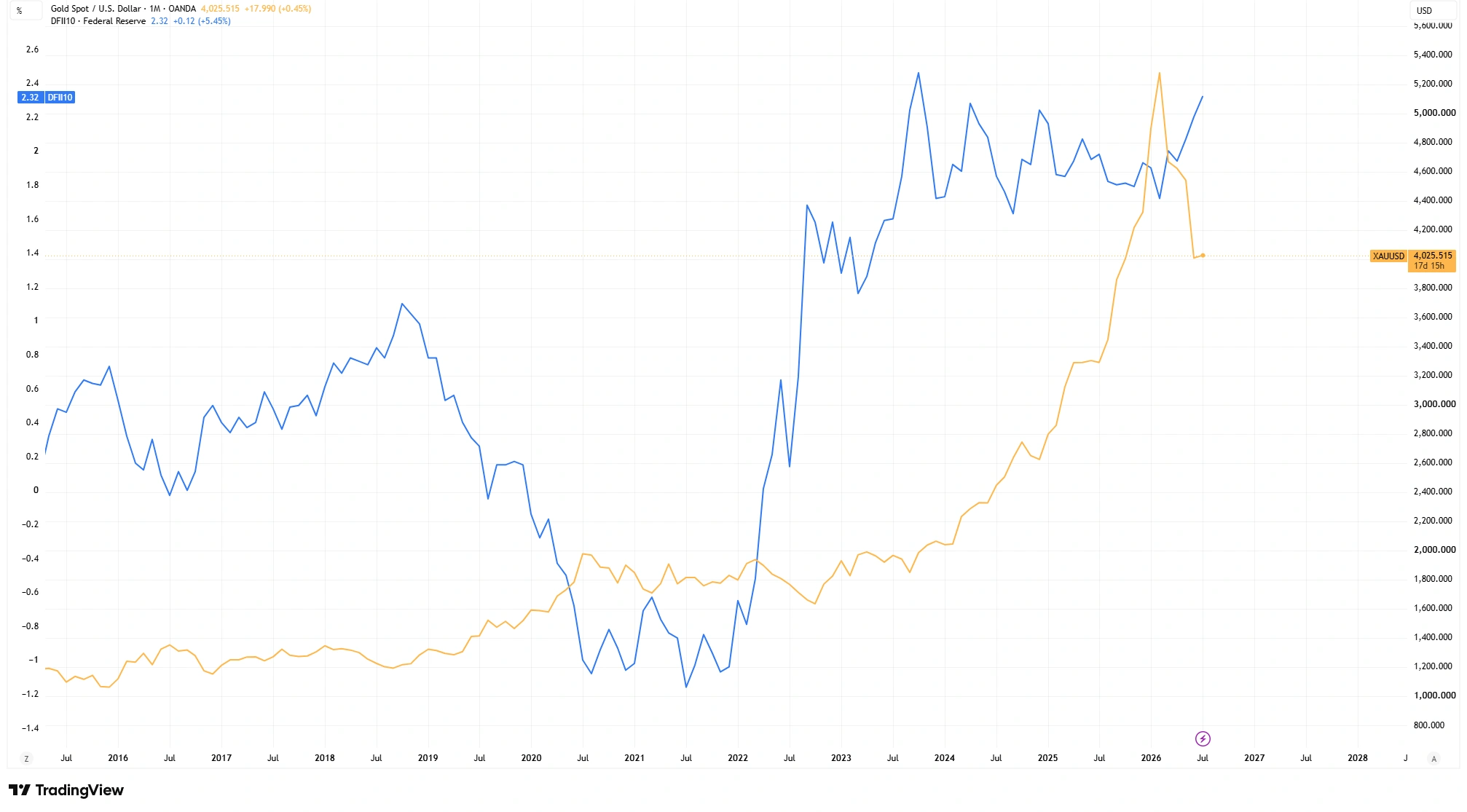

However, the relationship is not absolute. The below chart illustrates that while gold and real yields have often moved in opposite directions, there have also been periods when other macroeconomic forces became the dominant drivers of price. While real yields remain one of the most important influences on gold, they are only one part of a much broader picture.

Gold Spot Price and US 10-Year Real Treasury Yield (2015-Present)

Source & Methodology: TradingView. US 10-Year Real Treasury Yield data are sourced from the Federal Reserve Bank of St. Louis (FRED) using the DFII10 series. Gold prices are displayed on the right axis in US dollars per troy ounce, while real yields are displayed on the left axis as percentages. Past performance is not a reliable indicator of future performance. Data as of 14 July 2026.

Gold has historically shown a tendency to move inversely to real interest rates, although the relationship is not constant. Recent years illustrate how central bank demand, geopolitical uncertainty and other macroeconomic factors can outweigh the influence of real yields.

Why the US Dollar Matters

Another important influence is the strength of the US dollar.

Gold is primarily priced in US dollars. A stronger dollar makes gold more expensive for international buyers and can reduce demand, while a weaker dollar has historically tended to support prices.

Although the relationship is not always exact, many traders monitor movements in both the US Dollar Index and gold prices when assessing market conditions.

The Role of Central Banks

Central banks remain one of the largest long-term buyers of gold.

Gold forms part of many countries’ foreign exchange reserves alongside currencies and government bonds. In recent years, many central banks have increased their gold holdings to diversify reserves and strengthen financial resilience during periods of geopolitical and economic uncertainty.

According to the World Gold Council, central banks purchased more than 1,000 tonnes of gold in both 2022 and 2023, representing some of the strongest annual buying on record. Strong demand continued during 2024 as many central banks maintained elevated levels of gold purchases.

This additional source of demand has become an increasingly important factor influencing long term gold prices.

Why Do Investors Hold Gold?

A common question among newer investors is: if gold produces no income, why hold it at all?

Investors typically buy gold not for cash generation but for diversification, portfolio resilience and as a potential store of value during periods of financial uncertainty. Rather than replacing equities or bonds, gold often serves as a complementary asset within a diversified portfolio.

Bottom Line

Gold cannot be valued using traditional equity valuation techniques because it generates no earnings, dividends or cash flow.

Instead, professional investors assess gold through a broader macroeconomic framework that includes opportunity cost, real interest rates, inflation expectations, US dollar movements, central bank demand and overall investor sentiment.

No single factor determines gold prices. Instead, it is the interaction of these economic forces that shapes demand over time. Understanding these drivers helps explain why gold behaves differently from equities and continues to play an important role in diversified portfolios.