Renewed Oil Inflation Fears Test the AI Rally | Weekly Market Recap: 6-10 July 2026

Markets spent the second week of July balancing renewed inflation concerns against resilient corporate earnings and continued strength in artificial intelligence-related stocks. Rising oil prices and higher bond yields revived questions over how quickly central banks can begin easing policy, encouraging investors to become more selective in their positioning.

While technology continued to underpin broader equity markets, leadership became increasingly concentrated as investors rotated towards sectors supported by higher commodity prices and resilient earnings. The result was a week defined by selective risk-taking rather than broad-based market optimism.

Economic Overview

Markets spent the week balancing renewed energy price pressures against signs that inflation is gradually easing elsewhere. While higher oil prices revived concerns about inflation, central banks continued to signal that interest rates are likely to remain restrictive until there is clearer evidence that price pressures are moving sustainably back towards target. As a result, investors became more selective, favouring companies with resilient earnings while remaining cautious towards sectors more exposed to higher borrowing costs.

The June FOMC minutes reinforced the Federal Reserve’s cautious stance. Several policymakers indicated that further tightening could still be appropriate if inflation proves more persistent than expected, reinforcing expectations that interest rates may remain elevated for longer.

The ECB also maintained a measured tone, with updated projections indicating inflation could remain above target through early 2027. Together with ongoing geopolitical tensions in the Middle East, which continued supporting energy prices, this kept inflation risks firmly on investors’ radar.

In the UK, Bank of England officials also emphasised the need for a restrictive policy stance while inflation remains above target despite signs that domestic growth is slowing.

Economic data painted a mixed but resilient picture. US initial jobless claims fell to 215,000 in the week ending 4 July, suggesting the labour market is cooling gradually rather than weakening sharply. Germany’s industrial production rose 0.9% in May, offering further evidence that manufacturing activity is stabilising.

China presented a contrasting picture. Producer prices rose 4.1% year-on-year in June while consumer inflation eased to 1.0%, highlighting persistent cost pressures alongside subdued domestic demand. The People’s Bank of China maintained an accommodative policy stance as it continued supporting economic growth amid ongoing uncertainty.

Equities, Bonds and Commodities

Markets reflected increasingly selective investor positioning as renewed inflation concerns resurfaced.

In the United States, the S&P 500 rose to 7,575.39 during the week, while the Nasdaq Composite advanced to 26,281.61. The Dow Jones Industrial Average slipped to 52,637.01 as investors rotated away from more cyclical sectors. Technology continued attracting support from AI-related earnings, although gains became increasingly concentrated as valuations came under closer scrutiny.

European equities weakened, with the STOXX Europe 600 falling around 1.8%, the FTSE 100 declining to 10,497.3 and Germany’s DAX coming under pressure as weakness across semiconductor and automotive stocks outweighed stronger industrial production data.

Asian markets delivered mixed performance. Hong Kong’s Hang Seng Index gained 3.5% to 24,175.12 as expectations of continued policy support lifted Chinese technology shares. Japanese equities recovered from early losses after government proposals encouraging greater domestic pension-fund investment improved sentiment.

Bond markets reflected renewed caution around inflation. The US 10-year Treasury yield rose from 4.48% to 4.54%, while the two-year Treasury yield increased from 4.13% to 4.16%. Germany’s 10-year Bund yield moved above 3.0%, while the UK’s 10-year gilt remained close to 4.95%, reinforcing expectations that interest rates will remain restrictive.

Commodity markets were driven by geopolitical developments. Brent crude climbed to $76.01 per barrel as Middle East tensions supported prices, while gold eased to $4,103.23 per ounce as higher real yields reduced demand for non-yielding assets.

Overall, cross-asset performance reflected a market that continues to reward resilient earnings while remaining increasingly sensitive to inflation, interest-rate expectations and geopolitical developments.

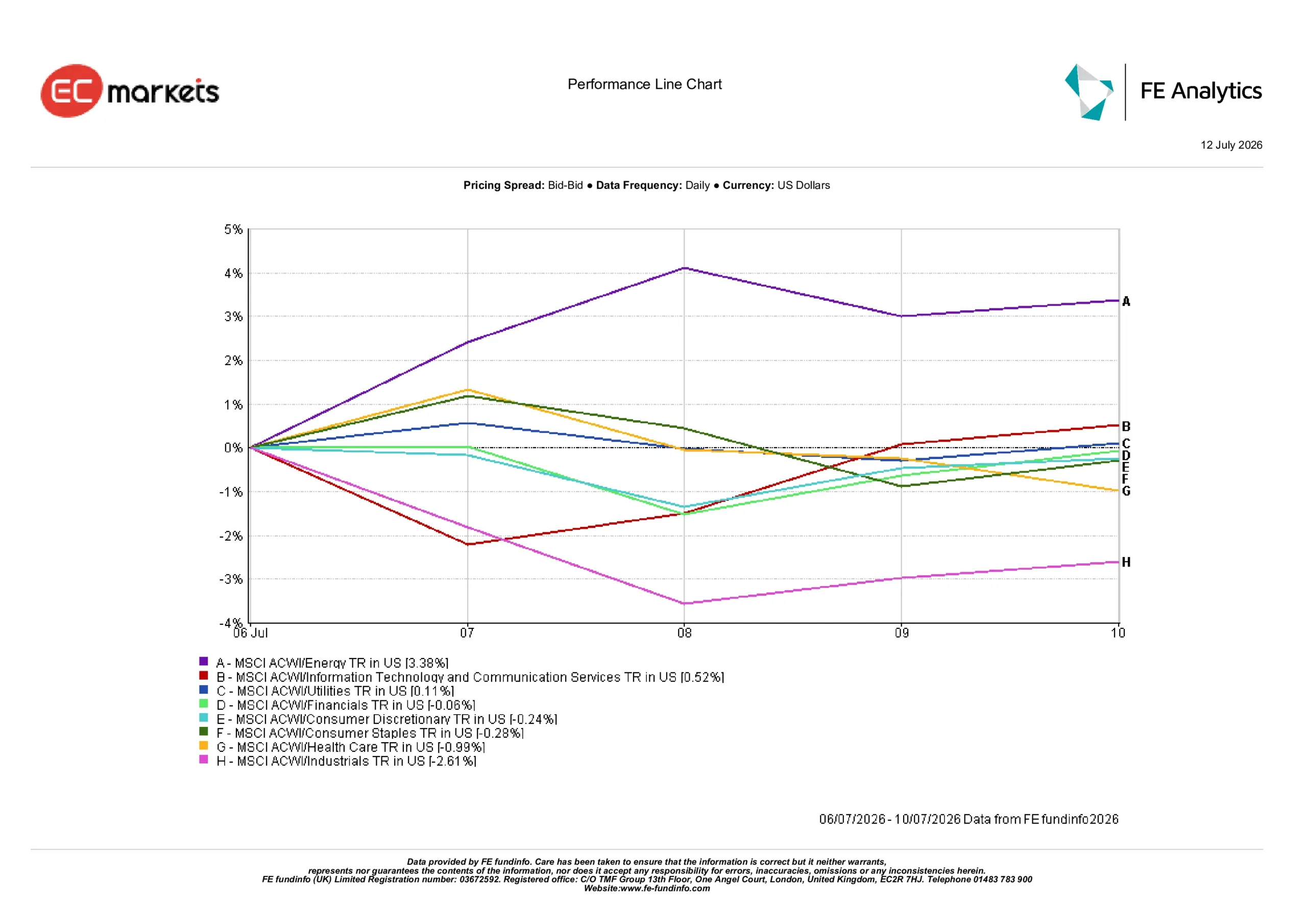

Sector Performance

Sector performance reflected investors’ preference for areas benefiting from higher commodity prices while remaining more cautious towards sectors exposed to rising costs and tighter financial conditions.

Energy led gains with a return of 3.38% as higher oil prices improved the outlook for producers. Information Technology & Communication Services gained 0.52%, supported by continued confidence in long-term AI investment despite growing valuation concerns.

Utilities added 0.11%, reflecting steady demand for defensive earnings, while Financials slipped 0.06% as the benefit of higher interest rates was offset by concerns that tighter financial conditions could weigh on future lending activity.

Consumer Discretionary declined 0.24%, Consumer Staples fell 0.28%, and Healthcare retreated 0.99% as investors reassessed earnings prospects.

Industrials recorded the weakest performance, declining 2.61%, as higher input costs, trade uncertainty and supply-chain concerns weighed on sentiment.

Sector Performance July 6th-10th 2026

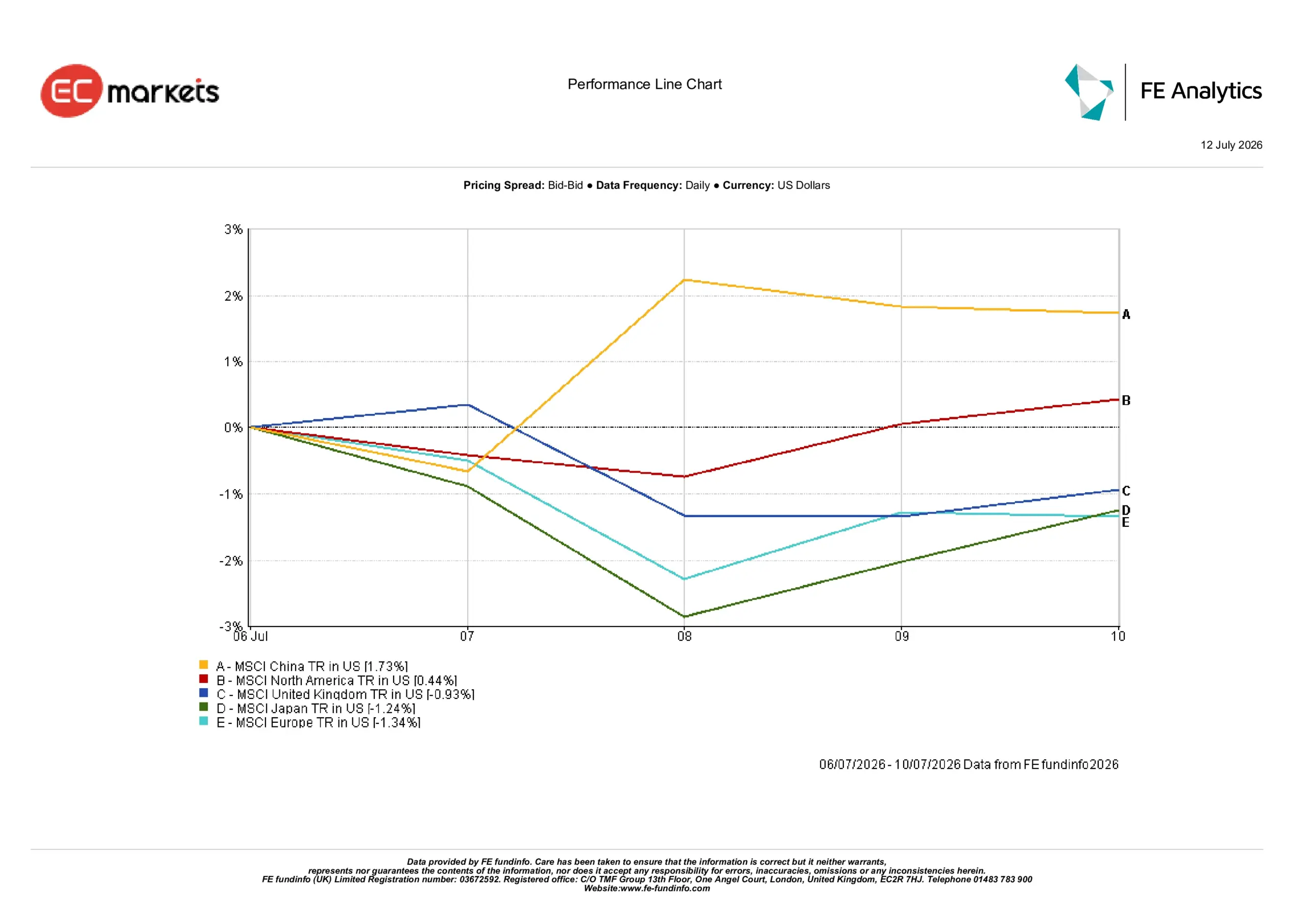

Regional Markets

Regional performance highlighted increasing divergence as investors became more selective about where they wanted cyclical exposure.

China delivered the strongest return at 1.73%, supported by renewed interest in technology shares, continued policy support and a relatively stable currency. North America followed with a gain of 0.44%, underpinned by continued strength in AI-related companies despite higher bond yields.

The United Kingdom declined 0.93% as higher gilt yields and weakness in Health Care outweighed support from defensive sectors. Japan fell 1.24% as early-week weakness in technology shares outweighed the subsequent recovery.

Europe was the weakest-performing region, declining 1.34% amid higher energy prices and continued weakness across semiconductor and automotive companies.

Regional Performance July 6th-10th 2026

Currency Markets

Currency markets remained driven primarily by diverging monetary-policy expectations and sovereign bond yields.

EUR/USD eased from 1.1441 to 1.1414 as concerns surrounding Europe’s energy outlook and slower economic growth continued weighing on the single currency.

GBP/USD strengthened from 1.3352 to 1.3407 as expectations that the Bank of England will maintain restrictive policy continued supporting sterling.

USD/JPY edged higher from 161.36 to 161.70, reflecting the continued gap between US and Japanese interest-rate expectations. Although the yen recovered some ground later in the week following proposals encouraging greater domestic pension-fund investment, the move was insufficient to reverse earlier weakness.

GBP/JPY rose from 215.45 to 216.80, reflecting sterling resilience against the Japanese currency.

Overall, foreign exchange markets continued reinforcing the week’s dominant macro theme: monetary-policy expectations remain the primary driver of currency performance.

Outlook and The Week Ahead

Attention now turns to whether upcoming inflation data reinforce the bond market’s renewed caution. Investors will closely monitor US CPI and PPI releases, together with retail sales, industrial production and consumer sentiment, for further evidence of how restrictive financial conditions are affecting the economy.

Markets will also continue assessing central-bank communication for guidance on how policymakers are balancing persistent inflation against uneven global growth. In Europe and the UK, investors will watch whether recent policy guidance remains appropriate if energy prices continue fluctuating.

China is expected to remain an important source of policy support, with investors monitoring whether further measures can strengthen domestic demand while maintaining confidence in the broader economy.

For now, markets remain increasingly selective. Investors continue favouring companies and regions supported by resilient earnings while remaining cautious towards areas that are more sensitive to higher interest rates, elevated energy prices and slowing global growth.