Labour-Market Resilience and Rising Yields Pressure Risk Assets | Weekly Recap: 1 - 5 June 2026

Markets began June on relatively stable footing as easing geopolitical tensions and softer oil prices continued supporting sentiment across global markets. However, the mood shifted sharply towards the end of the week after stronger-than-expected US labour-market data prompted investors to reassess expectations for Federal Reserve policy. Rising Treasury yields, a stronger US dollar and renewed concerns around higher-for-longer interest rates weighed on risk assets, particularly growth-oriented sectors that had led much of the recent rally.

The result was a broad repricing across asset classes, with equities coming under pressure, bond yields moving higher and investors increasingly focused on the outlook for inflation, monetary policy and financial conditions heading into the second half of the year.

Economic Overview

Markets began the week with a relatively constructive backdrop as easing geopolitical tensions and softer energy prices helped support sentiment. However, stronger-than-expected US economic data ultimately became the dominant market driver.

The biggest catalyst was Friday’s US jobs report, which showed the economy added 172,000 jobs in May, significantly above expectations of 86,000. The unemployment rate remained unchanged at 4.3%, reinforcing the view that the labour market remains resilient despite elevated borrowing costs. The stronger data reduced expectations for near-term Federal Reserve rate cuts and reignited higher-for-longer policy concerns.

Earlier in the week, business activity data also pointed to persistent inflation pressures. The US services sector expanded to 54.5 in May, while the prices-paid component surged to 71.3, its highest level since August 2022. Together, the figures suggested economic activity remains relatively healthy while inflation risks remain elevated.

Outside the United States, economic momentum remained more subdued. Eurozone business activity data continued pointing towards sluggish growth conditions, while political uncertainty and economic concerns weighed on sentiment in the United Kingdom.

In Japan, government bond yields moved higher as inflation indicators remained firm, reinforcing expectations that the Bank of Japan will continue gradually moving away from its ultra-accommodative monetary policy stance.

Overall, markets increasingly shifted away from expectations of imminent policy easing and focused instead on the prospect of higher interest rates remaining in place for longer.

Equities, Bonds and Commodities

Equities

Global equity markets experienced a sharp reversal towards the end of the week as stronger US economic data pushed bond yields higher and weighed on valuations.

In the United States, the S&P 500 fell 2.75% on Friday to finish the week at 7,383.74. Growth-oriented sectors, particularly technology, came under pressure as higher yields weighed on valuations and reduced support for risk assets.

European equities also moved lower. Germany’s DAX and France’s CAC 40 lost ground as investors weighed slowing growth against persistent inflation pressures, while the FTSE 100 weakened as risk sentiment deteriorated.

Bonds

Bond markets underwent a notable repricing following the payrolls report. The US 10-year Treasury yield moved sharply higher, while the policy-sensitive two-year yield climbed back above 4.0% as markets pushed back expectations for Federal Reserve rate cuts.

Sovereign bond yields across Europe and the United Kingdom followed a similar pattern, reflecting the global nature of the adjustment as investors reassessed the outlook for monetary policy.

Commodities

Commodity markets delivered a more mixed performance. Oil prices eased as concerns surrounding Middle East supply disruptions moderated, with Brent crude slipping below the $100 per barrel level.

Gold also weakened, falling towards $4,510 per ounce as rising real yields and renewed US dollar strength reduced demand for non-yielding assets.

Overall, cross-asset performance reflected a market increasingly focused on policy expectations and financial conditions rather than simply growth resilience.

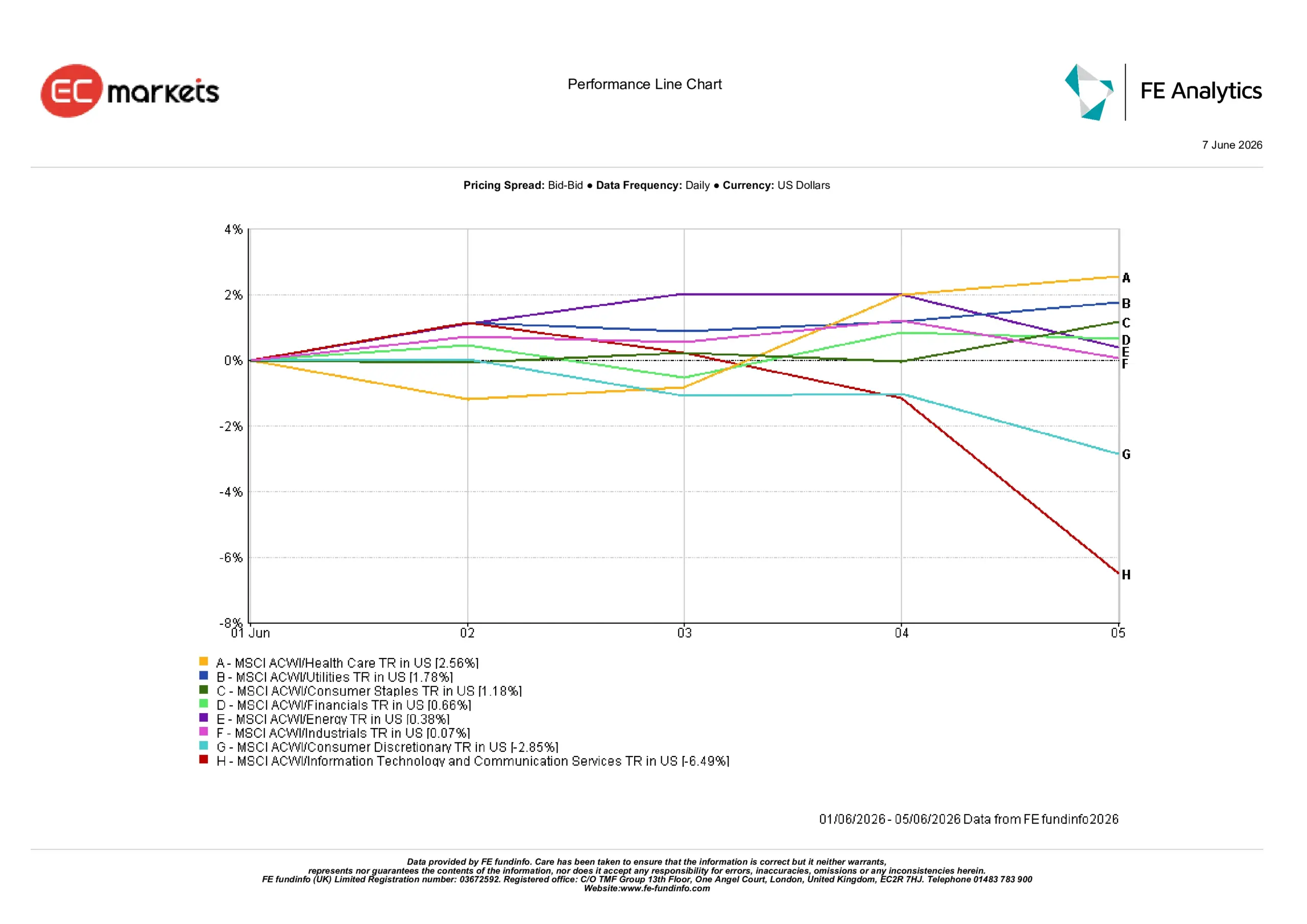

Sector Performance

Sector performance highlighted a clear shift in investor positioning as rising bond yields triggered a rotation away from growth-oriented sectors.

Information Technology and Communication Services was the weakest-performing sector, falling 6.49% as higher yields weighed heavily on technology and growth-stock valuations.

Consumer Discretionary also struggled, declining 2.85% as investors reassessed the outlook for consumer spending in a higher-rate environment.

Defensive sectors significantly outperformed. Health Care and Utilities gained 2.56% and 1.78% respectively as investors sought more stable areas of the market. Consumer Staples rose 1.18%, followed by Financials at 0.66%, while Energy delivered a modest gain of 0.38%.

Industrials remained broadly unchanged, rising just 0.07% during the week.

Overall, sector performance suggested investors were becoming increasingly defensive, favouring stability and earnings resilience over higher-growth opportunities.

Sector Performance June 1st – 5th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 5 June 2026.

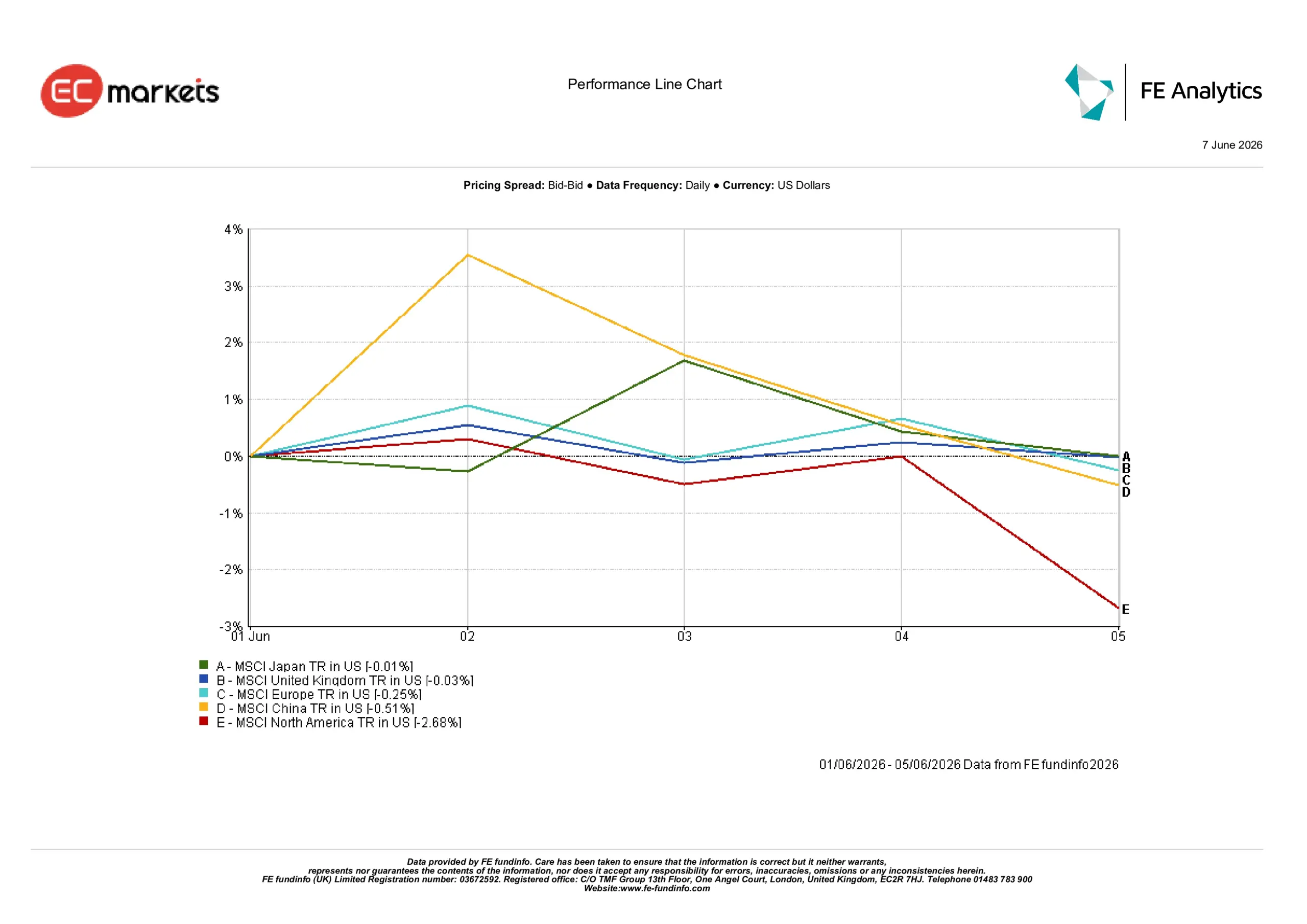

Regional Markets

Regional performance diverged as rising bond yields and differing economic conditions shaped returns.

North America was the weakest-performing major region, falling 2.68% as higher Treasury yields triggered a broad repricing across equity markets.

China declined 0.51% as concerns surrounding the pace of economic recovery continued to weigh on investor sentiment, while Europe fell 0.25% amid weak economic data and persistent growth concerns.

The United Kingdom proved relatively resilient, finishing the week down just 0.03%, while Japan was the strongest-performing major region, ending the week virtually unchanged with a decline of only 0.01%.

Overall, regional performance highlighted how markets with greater exposure to growth and technology sectors experienced the largest adjustments as yields moved higher.

Regional Performance June 1st – 5th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 5 June 2026.

Currency Markets

Currency markets were dominated by renewed US dollar strength following the stronger-than-expected payrolls report and the subsequent repricing of Federal Reserve expectations.

The euro weakened against the dollar as widening interest-rate differentials continued favouring the greenback and supporting demand for US assets.

Sterling also came under pressure against the US dollar as stronger US data reinforced expectations that interest rates may remain elevated for longer.

Meanwhile, the Japanese yen remained under pressure as the substantial yield advantage offered by US assets continued to outweigh expectations of gradual policy normalisation from the Bank of Japan.

Overall, foreign exchange markets reflected the same theme seen across other asset classes, with higher US yields and expectations of prolonged restrictive monetary policy supporting broad US dollar strength.

Outlook and The Week Ahead

Looking ahead, investors are likely to remain focused on inflation data and central-bank communication following the sharp repricing seen across bond markets.

Upcoming price indicators and activity data will provide further insight into whether inflation pressures remain persistent and whether tighter financial conditions are beginning to weigh more meaningfully on economic growth. Markets will also continue monitoring developments in sovereign bond yields, which have become an increasingly important driver of sentiment.

For now, markets appear to be entering a more cautious phase, where policy expectations, inflation trends and financial conditions are likely to play a greater role in shaping performance across asset classes than earnings or growth optimism alone.