Equity Risk Premium: Are Stocks Still Worth the Risk?

By 2026, investors have found themselves in a financial landscape that would have seemed unusual just a few years ago. For the first time in over a decade, cash and government bonds are offering yields close to 5%.

This marks a major shift from the years following the Global Financial Crisis and the pandemic, when interest rates remained extremely low and investors had little choice but to turn to equities for returns.

Today, the question looks very different. If relatively safe assets are offering attractive yields, are stocks still providing enough additional return to justify the extra risk?

Professional investors often answer that question by looking at one important measure: the Equity Risk Premium.

What Is the Equity Risk Premium?

In simple terms, the Equity Risk Premium (ERP) is the extra return investors expect from owning stocks instead of government bonds.

Stocks are inherently uncertain. Company earnings fluctuate, recessions happen and markets occasionally experience sharp corrections. Government bonds, on the other hand, are generally viewed as lower-risk investments. Because equities carry greater uncertainty, investors expect higher long-term returns in exchange for accepting that risk.

ERP represents the gap between what investors can earn from relatively safe assets and what they expect to earn from equities. If government bonds yield 4%, investors may expect stocks to deliver 6% or 7% over time to compensate for the additional uncertainty.

Over long periods, equities have historically outperformed bonds because investors have been rewarded for accepting greater risk. This additional return has been one of the key drivers of long-term wealth creation.

When that gap is wide, equities may appear attractive. When the gap narrows, stocks have to work harder to justify their valuations.

Why Interest Rates Matter

Interest rates play a major role in determining how attractive stocks look relative to bonds.

During much of the decade following the Global Financial Crisis, government bond yields often remained below 3%. The same pattern reappeared during the pandemic, when interest rates fell close to zero. In that environment, investors were willing to pay increasingly high prices for equities because there were few attractive alternatives.

That changed in 2022 and 2023. To combat inflation, the Federal Reserve raised interest rates aggressively, pushing the Federal Funds Rate to 5.25%-5.50%. By 2024-2026, the US 10-Year Treasury yield traded largely between 4% and 5%.

Higher bond yields effectively raise the bar for equities. When investors can earn close to 5% from government bonds, they naturally become more selective about the risks they are willing to take in the stock market.

From TINA to TARA: Why Alternatives Matter Again

For years, markets operated under the idea of TINA, or “There Is No Alternative”. With bond yields close to zero, investors had little choice but to allocate capital to equities, helping support valuations.

By 2026, investors are increasingly entering what some analysts describe as the TARA era: “There Are Reasonable Alternatives”.

For many years, investors accepted higher stock market risk because bonds offered little income. Today, with government bonds yielding around 5%, investors once again have meaningful alternatives, making the competition between stocks and bonds far more balanced.

One way investors compare the two asset classes is through earnings yield, which is simply the inverse of the price-to-earnings ratio. It provides a rough estimate of how much profit investors receive relative to the price they pay for stocks.

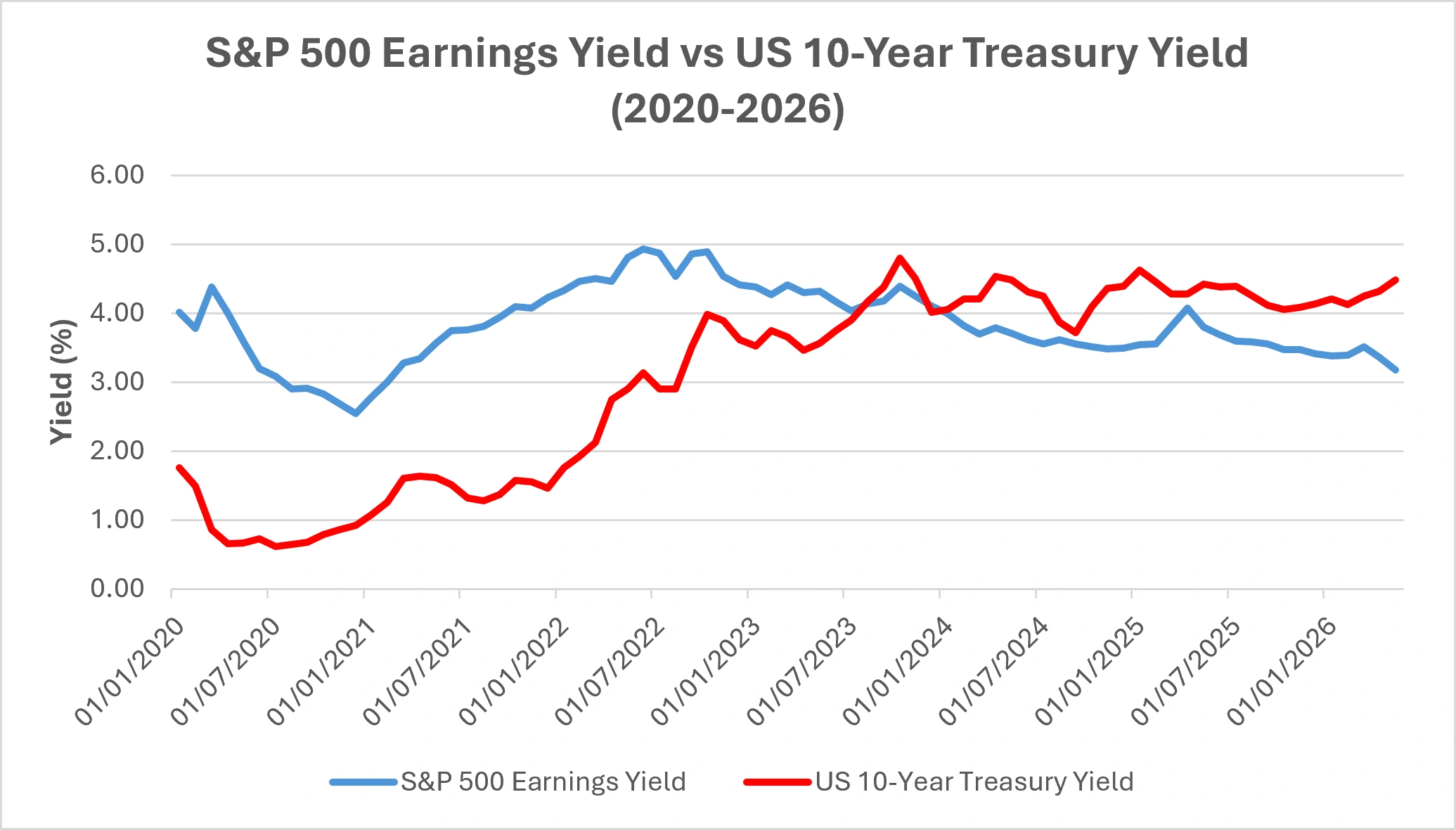

In early 2026, the S&P 500 earnings yield stood at roughly 3.9%, implying a valuation close to 25 times earnings. At the same time, the US 10-Year Treasury yield was around 4.3%.

This meant that bonds were offering yields comparable to, or even higher than, the earnings yield available from equities. It was a reversal not seen since the early 2000s and represented a significant change in the investment landscape.

S&P 500 Earnings Yield vs US 10-Year Treasury Yield

Source: Board of Governors of the Federal Reserve System (US) via FRED® and Multpl.com. Past performance is not a reliable indicator of future performance. Data as of May 2026.

Rising bond yields have steadily reduced the return advantage enjoyed by equities since 2022. S&P 500 earnings yield was calculated as the inverse of the S&P 500 P/E ratio (100 ÷ P/E ratio), using monthly P/E ratio data from Multpl.com. By 2024-2026, Treasury yields had risen above the earnings yield of the S&P 500, highlighting why investors have become increasingly selective when assessing risk and valuation.

As the Equity Risk Premium narrows, investors often become less tolerant of disappointing earnings or slower growth. Companies that fail to meet expectations may face sharper valuation adjustments as capital has more attractive alternatives.

Why the Relationship Is Not Always Straightforward

None of this means equities are doomed to underperform.

Stocks offer something bonds cannot: growth. Corporate profits can expand, dividends can increase and businesses can innovate. Bonds, by contrast, provide largely fixed returns.

History shows that equities have delivered superior long-term returns precisely because investors are compensated for accepting greater uncertainty. Strong economic growth, rising productivity and improving earnings can allow stocks to outperform even when interest rates remain elevated.

There is also no single “correct” ERP. The amount of extra return investors demand changes over time depending on economic growth, inflation expectations and market sentiment.

During periods of uncertainty, investors often demand a larger premium. During periods of optimism, they may be willing to accept a smaller one.

This is why the relationship between bond yields and stock valuations is not always straightforward. Valuation matters, but so do earnings, innovation and investor expectations.

What It Means for Investors

A lower ERP does not necessarily mean investors should abandon stocks or move entirely into cash.

However, it does suggest that the easy gains of the low-rate era may be harder to achieve.

When the return advantage of equities narrows, investors often place greater emphasis on quality. Companies with strong balance sheets, consistent earnings growth and reliable dividends tend to become more attractive in a higher-rate environment.

Higher interest rates also affect sectors differently. High-growth companies, whose valuations rely heavily on future earnings, are generally more sensitive to rising bond yields. By contrast, businesses with stable cash flows and dependable dividends may become relatively more attractive when investors prioritise income and financial strength.

Markets are constantly weighing the trade-off between safety and growth. Understanding ERP helps investors think beyond price movements and focus on whether they are being adequately compensated for taking risk.

Bottom Line

The Equity Risk Premium helps investors assess whether the potential return from equities is sufficient to justify the additional risk relative to safer assets.

In the higher-rate environment of 2026, that premium has narrowed as government bonds once again offer meaningful yields. While this does not make equities unattractive, it does mean valuations, earnings growth and business quality matter more than they did during the low-rate era.

For investors, understanding ERP provides a useful framework for evaluating the ongoing trade-off between safety and growth.