Energy Volatility Resurfaces as Growth Positioning Shows Early Strain | Weekly Recap: 20-24 April 2026

Global markets turned more cautious last week as renewed Strait of Hormuz tensions lifted oil prices and challenged the recent rotation into growth assets. US equities remained relatively resilient, while Europe and China lagged amid softer growth signals and renewed energy sensitivity.

Economic Overview

The week was shaped by a renewed shift in the energy narrative, as markets reassessed whether the easing in geopolitical risk seen earlier in April was sustainable. Fresh disruption concerns around the Strait of Hormuz reintroduced supply fears into oil markets, interrupting what had begun to look like a stabilisation phase.

This came against a softer global growth backdrop. In the euro area, flash PMI data remained in contraction territory, with the composite index holding below 50 and services activity weakening further. By contrast, activity in the US and UK proved more resilient, suggesting that the slowdown remains uneven rather than synchronised.

In the United States, the inflation narrative remained sensitive to energy developments. While earlier data had shown some moderation, the risk of renewed pass-through from higher oil prices remains. This has kept the Federal Reserve cautious, with policy expectations broadly stable but highly data dependent.

Across Europe and the UK, the policy backdrop remained constrained. Growth signals continue to soften, while inflation expectations remain sensitive to energy prices. In Asia, China’s growth remained relatively stable, though domestic demand indicators were mixed, while the BoJ continued to signal a gradual and measured approach to policy normalisation.

Overall, the macro environment appeared less like a clean recovery and more like a fragile stabilisation, where growth resilience exists but remains vulnerable to renewed energy-driven volatility.

Markets Overview

Equities

Equity markets reflected this shift, with performance becoming more selective rather than broadly risk-on. In the US, the S&P 500 ended the week modestly higher, supported primarily by continued strength in technology and growth-oriented sectors. The Nasdaq also advanced, extending its leadership, while the Dow Jones Industrial Average lagged, reflecting weaker performance in more cyclical segments.

In contrast, European equities struggled to maintain momentum. The STOXX Europe 600 declined over the week, while Germany’s DAX and the FTSE 100 also moved lower, reflecting a combination of weaker growth expectations and sensitivity to energy developments.

Asian markets were more mixed. Japan showed relative resilience, supported by global positioning and currency dynamics, while Chinese equities remained under pressure as domestic demand concerns limited upside.

Bonds

Bond markets reflected a cautious adjustment in expectations. US Treasury yields moved modestly lower into the end of the week, with the 10-year settling near 4.30% and the 2-year around 3.78%, suggesting that markets were balancing easing inflation pressures against the risk of renewed energy-driven price shocks.

Commodities

Oil remained the central driver of sentiment. Prices moved higher earlier in the week before stabilising, reinforcing the view that geopolitical risk premia remain embedded in the market. Gold stayed supported, benefiting from lower yields and lingering uncertainty.

Overall, cross-asset behaviour suggested investors were balancing improving growth signals against renewed inflation risks linked to energy markets.

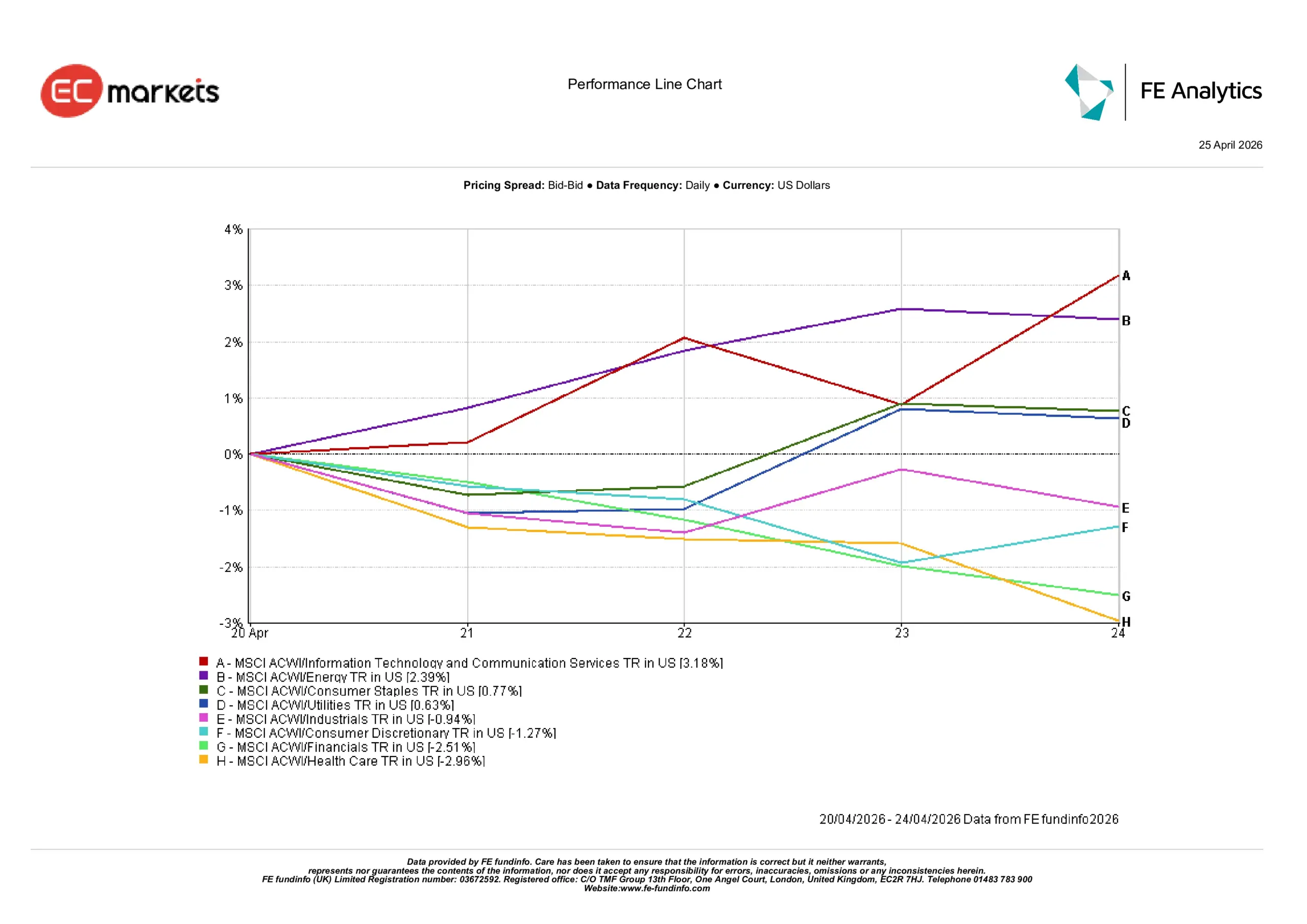

Sector Performance

Sector performance reflected a more cautious and uneven rotation, with leadership narrowing rather than broadening.

Information Technology & Communication Services were the strongest performers, rising 3.18% over the week, supported by lower yields and continued demand for growth exposure. Energy also delivered a positive return of 2.39%, reflecting the rebound in oil prices and renewed supply concerns.

Defensive sectors showed relative resilience but did not lead. Consumer Staples rose 0.77%, while Utilities gained 0.63%, suggesting that investors maintained some defensive exposure without fully rotating back into safety.

More cyclical sectors underperformed. Industrials declined 0.94%, while Consumer Discretionary fell 1.27%, indicating that confidence in a sustained growth rebound remains limited. Financials were among the weakest performers, falling 2.51%, as rate uncertainty and macro sensitivity weighed on the sector. Health Care also lagged, declining 2.96%.

Overall, sector performance suggested investors remained selectively positioned for growth, but without broad conviction behind a full cyclical rotation.

Sector Performance April 20th – 24th 2026

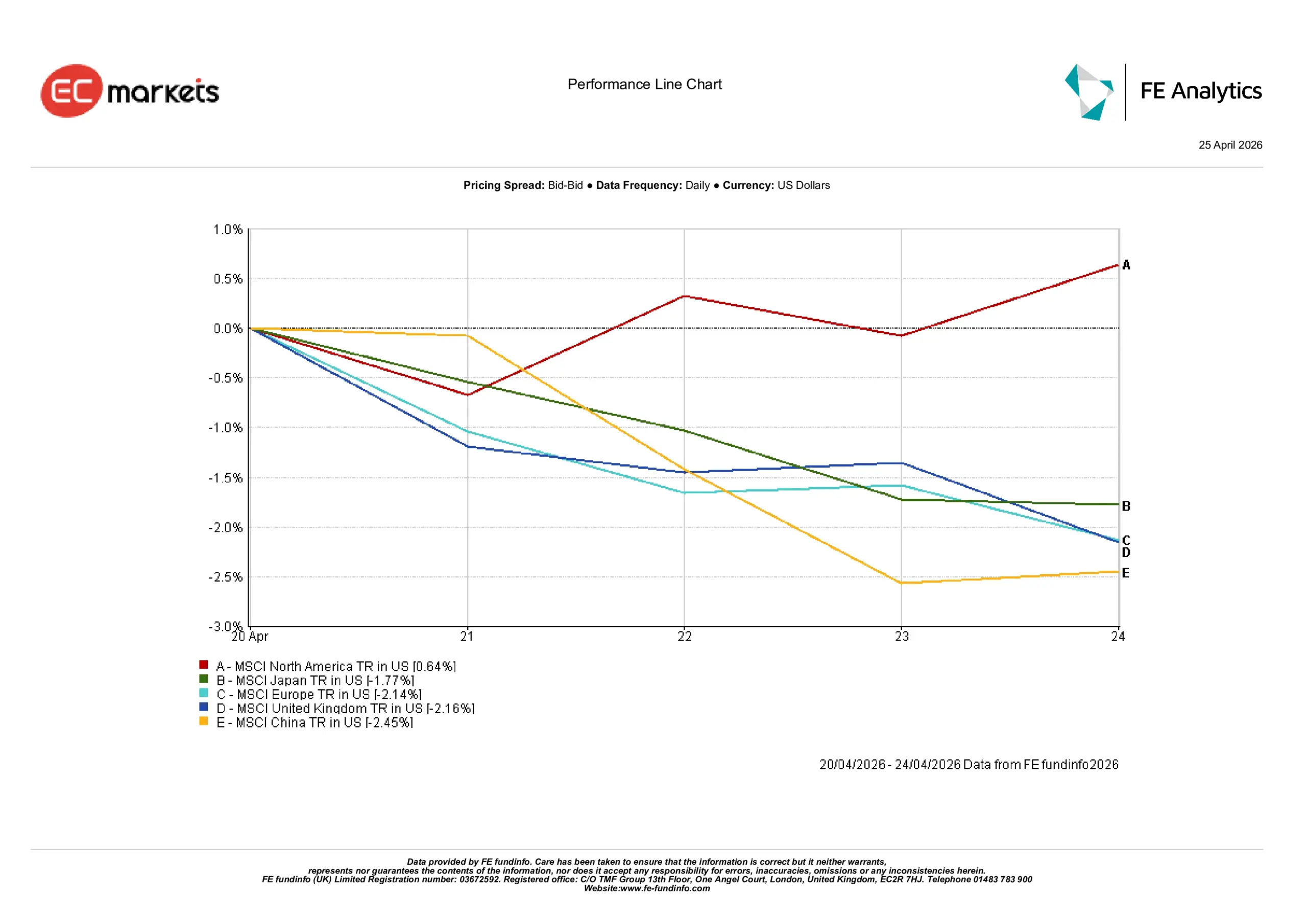

Regional Markets

Regional performance highlighted a clear divergence in global market behaviour.

North America was the only region to post a gain, rising 0.64% over the week, supported by continued strength in technology and relatively resilient earnings expectations.

All other major regions declined. Japan fell 1.77%, reflecting a combination of global sentiment and currency effects. Europe declined 2.14%, while the UK fell 2.16%, both impacted by weaker growth expectations and energy sensitivity.

China was the weakest performer, declining 2.45%, as domestic demand concerns and broader risk sentiment weighed on equity markets despite stable headline growth data.

This divergence suggested that capital remained concentrated in markets with stronger growth visibility, while regions more exposed to external risks continued to lag.

Regional Performance April 20th – 24th 2026

Currency Markets

Foreign-exchange markets reflected a more balanced and less directional environment.

EUR/USD

Declined from 1.1789 at the start of the week to 1.1722 by 24 April, reflecting continued pressure on the euro amid weaker growth signals in the euro area.

GBP/USD

Remained relatively stable, edging from 1.3535 to 1.3533, suggesting that sterling held its ground despite mixed domestic data.

USD/JPY

Rose from 158.82 to 159.38, highlighting continued yen weakness driven by persistent rate differentials and the BoJ’s gradual policy stance.

GBP/JPY

Increased from 214.96 to 215.67, reflecting the combination of a stable pound and weaker yen.

Overall, FX markets reinforced the broader macro narrative of relative US growth resilience and ongoing policy divergence across major economies.

Outlook and The Week Ahead

The key question moving into the coming week is whether markets can maintain this fragile balance between growth resilience and renewed energy-driven uncertainty.

Flash PMI data will provide further insight into the strength of global activity, particularly in Europe where contractionary signals have already emerged. Inflation data from the UK and Japan will also be closely watched for signs that recent energy volatility is feeding into broader price pressures.

At the same time, geopolitical developments remain central. Renewed disruption risks around the Strait of Hormuz suggest that the easing in oil prices seen earlier in April may prove temporary rather than structural. As a result, markets may enter the week with a more cautious tone, particularly if energy prices begin to reprice higher again.

If energy markets stabilise, the recent positioning in growth sectors could hold. However, if volatility returns, the past week’s moves may appear less like a continuation of recovery and more like a pause within a broader period of uncertainty.

The central question is no longer whether conditions are improving, but whether they are stable enough to sustain risk appetite.