Quality Over Hype: Why ROIC Matters More Than Revenue Growth

Table of Contents

- Why Revenue Growth Doesn't Tell the Full Story

- What Is ROIC?

- ROIC vs Revenue Growth

- Why ROIC Matters More Than Revenue Growth

- Economic Moats and Competitive Advantages

- Why Higher Interest Rates Have Changed the Conversation

- If Growth Is Strong, Why Does Capital Efficiency Matter?

- Why the Relationship Is Not Always Straightforward

- Bottom Line

When investors evaluate companies, revenue growth often grabs the headlines. Fast-growing businesses can attract significant attention, particularly when they operate in exciting industries or emerging markets. However, experienced investors know that growth alone does not always create value. What often matters more is how efficiently a company turns investment into profits. One metric that helps answer that question is Return on Invested Capital (ROIC), a measure widely used to assess business quality, capital efficiency and long-term value creation.

Why Revenue Growth Doesn’t Tell the Full Story

Investors often focus on revenue growth when evaluating companies. Rising sales can signal strong demand and expanding market share, but growth alone does not guarantee value creation.

Some companies generate impressive revenues but require enormous amounts of capital to sustain that growth. Others are able to turn relatively modest investments into substantial profits. This difference matters because shareholder returns depend not only on how fast a company grows, but also on how efficiently it uses capital.

That is why many professional investors pay close attention to Return on Invested Capital, or ROIC. In simple terms, ROIC measures how effectively a company turns capital into profits and helps distinguish exciting growth stories from genuinely high-quality businesses.

What Is ROIC?

ROIC measures how efficiently a company uses the money invested in the business to generate profits. That invested capital includes both shareholders’ equity and debt used to finance operations.

Rather than focusing only on how much a company earns, ROIC asks a different question: how much profit is generated for every dollar invested in the business?

A high ROIC suggests management is allocating capital effectively and creating value for shareholders. A low ROIC may indicate that growth is expensive or inefficient. In general, companies that consistently earn returns above their cost of capital are creating value, while those that fail to do so may destroy value over time.

In simple terms, ROIC helps investors understand whether management is creating value or merely consuming capital.

ROIC vs Revenue Growth

Both metrics are important, but they measure very different things.

Revenue Growth

- Measures how quickly a company’s sales are increasing.

- Can indicate rising demand or market share gains.

- Does not necessarily show whether growth is profitable.

ROIC

- Measures how efficiently a company converts invested capital into profits.

- Helps assess management quality and capital allocation.

- Provides insight into whether growth is actually creating shareholder value.

This distinction explains why many professional investors look beyond headline revenue figures when assessing business quality.

Why ROIC Matters More Than Revenue Growth

Revenue can grow rapidly without necessarily creating shareholder value. Companies may expand aggressively or spend heavily while generating disappointing returns.

By contrast, businesses with high ROIC are often able to generate strong profits without requiring large amounts of additional capital. These companies frequently benefit from pricing power, efficient operations and strong management execution.

High ROIC becomes particularly powerful when companies can continue reinvesting profits at similarly attractive rates. Businesses with durable competitive advantages and large growth opportunities are often able to compound shareholder value over many years.

This is one reason why quality growth is often more valuable than growth for its own sake.

Economic Moats and Competitive Advantages

High ROIC rarely happens by accident.

Companies with strong competitive advantages, often referred to as economic moats, tend to generate consistently high returns because competitors struggle to replicate their business models.

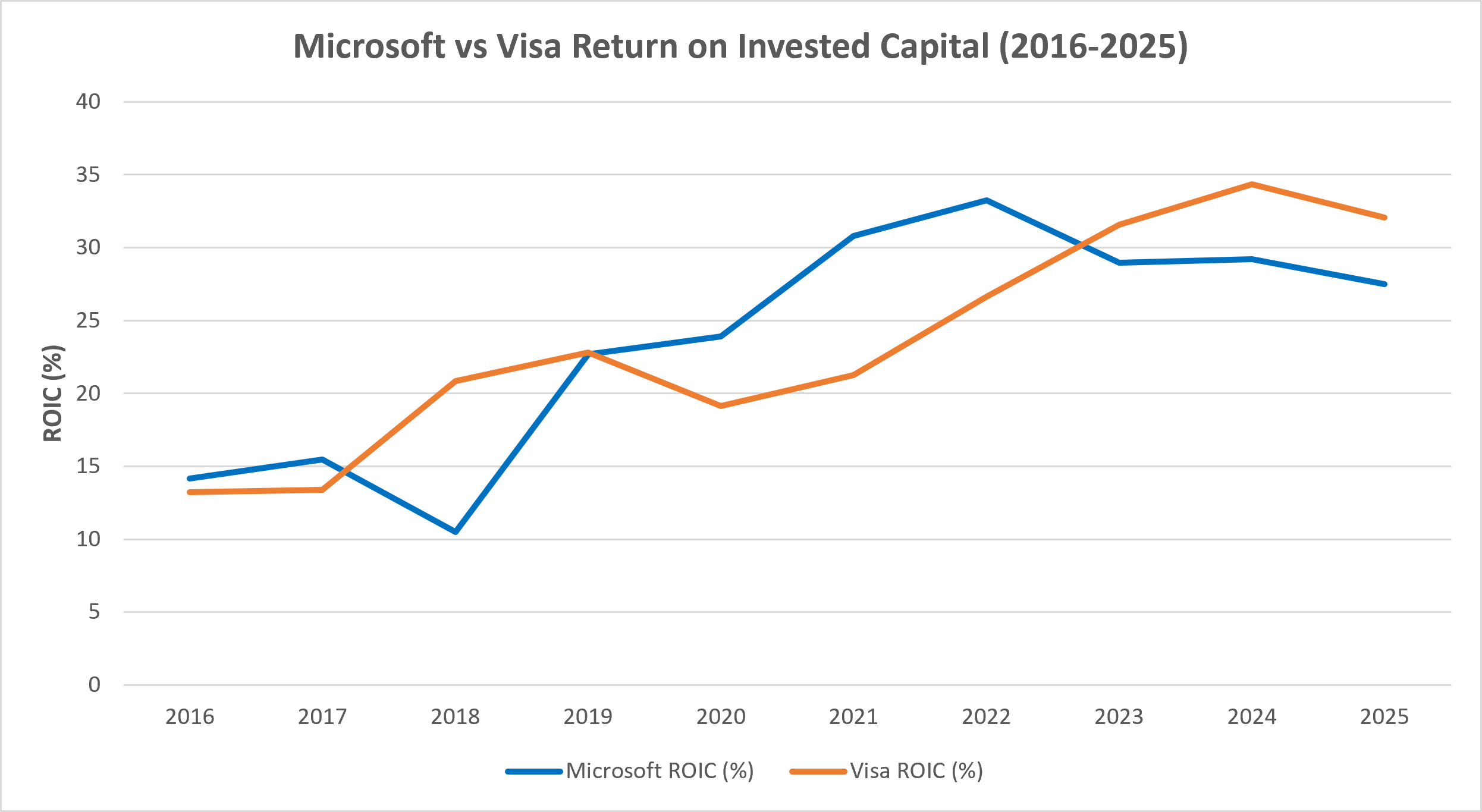

Microsoft’s software ecosystem and cloud platform have historically supported returns on invested capital well above 20%. Visa’s asset-light payments network has frequently generated returns above 30%, making it one of the most capital-efficient businesses in the world. Apple has also maintained attractive returns thanks to its powerful brand and integrated ecosystem.

According to Morningstar, Visa’s ROIC has steadily increased over the past decade, breaking above 30% in recent years, while Microsoft has consistently generated returns exceeding 20%. These figures stand comfortably above their estimated cost of capital, helping explain why investors often regard them as high-quality businesses.

By contrast, capital-intensive industries such as airlines, energy and manufacturing typically generate lower and more cyclical returns because they require significant investment in equipment and infrastructure and are often more exposed to economic cycles.

Why Higher Interest Rates Have Changed the Conversation

During the years following the Global Financial Crisis and the pandemic, low interest rates made capital cheap and markets often rewarded growth at almost any cost.

That changed after central banks raised interest rates in 2022 and 2023. As borrowing costs increased, investors shifted their attention towards profitability, balance sheet strength and capital efficiency.

In a higher-for-longer environment, companies that can generate attractive returns without relying heavily on external financing have become increasingly attractive.

Ultimately, ROIC is most meaningful when viewed relative to the cost of financing the business. Companies that consistently earn returns above their cost of capital are generally creating value for shareholders.

If Growth Is Strong, Why Does Capital Efficiency Matter?

Growth requires investment, and not all investment creates value.

Companies that need to spend enormous sums simply to maintain growth may deliver weaker long-term returns than businesses that generate substantial profits from relatively modest investments.

This helps explain why many of the world’s highest-quality companies have delivered strong shareholder returns over long periods. Businesses that consistently earn returns well above their cost of capital can reinvest profits and compound value over time.

Quality growth often proves more valuable than rapid growth. Investors are ultimately rewarded not just for growth, but for profitable growth.

Why the Relationship Is Not Always Straightforward

Low or negative ROIC is not automatically a warning sign.

Young and rapidly growing businesses may intentionally generate lower returns while investing heavily in future expansion. If those investments create durable competitive advantages and stronger earnings potential, weaker near-term returns may be justified.

ROIC can also vary across industries and economic cycles. Capital-intensive sectors often experience stronger returns when demand is high and weaker returns during economic slowdowns.

For this reason, ROIC is most useful when compared with industry peers and evaluated over long periods rather than in isolation.

Microsoft vs Visa Return on Invested Capital (2016-2025)

Source & Methodology: The historical trend metrics displayed in this chart are sourced directly from the Financials (Profitability & Efficiency) data segments on Morningstar. Return on Invested Capital (ROIC) is an adjusted, non-GAAP efficiency metric. It is utilized here under Morningstar’s standardized calculation modelling to guarantee an accurate, apples-to-apples performance comparison over the 2016-2025 timeline. Past performance is not a reliable indicator of future performance.

Microsoft and Visa have consistently generated returns on invested capital well above their estimated cost of capital. These durable competitive advantages and efficient business models have supported long-term shareholder value creation.

Bottom Line

ROIC measures how efficiently companies turn capital into profits, which is why many professional investors view it as one of the most important indicators of business quality.

Revenue growth remains important, but growth alone does not guarantee value creation. Companies that consistently generate high returns on capital often possess durable competitive advantages and strong management teams that can create wealth without relying excessively on external financing.

In the end, quality and growth work best when they go hand in hand. For long-term investors, understanding ROIC can provide a deeper perspective on what truly drives sustainable business success.

Disclaimer: This material is provided for educational and informational purposes only and does not constitute investment advice or a recommendation. Investments can fall as well as rise in value, and past performance is not a reliable indicator of future results.