ECB in Limbo as Energy Prices Trigger Inflation Scare

Energy markets have pushed the European Central Bank (ECB) back into focus, with traders increasingly leaning towards a higher-for-longer rate outlook as inflation risks begin to resurface.

The recent rebound in oil prices, with crude moving back above the $100 mark, has rattled rate cut expectations. Markets are now less confident cuts will arrive as soon as previously thought.

What’s Moving Eurozone Inflation?

The move has been fairly straightforward in its drivers. Energy prices have turned higher again at a time when the eurozone was beginning to see inflation ease.

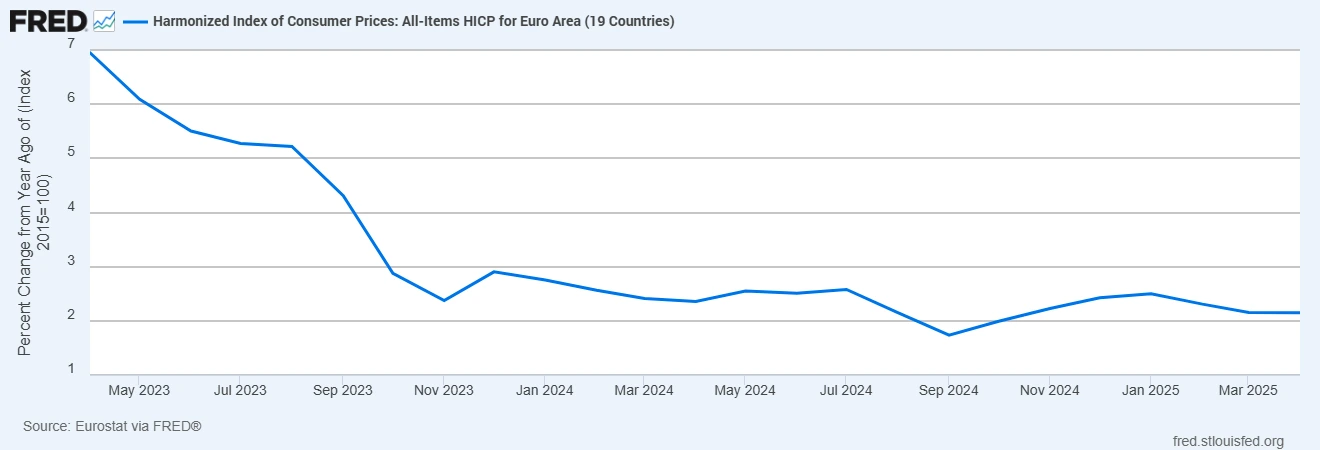

That reversal is already showing up in the data. Headline inflation rose to 2.5% in March from 1.9% the month before, with the energy component swinging sharply from a 3.1% decline to a 4.9% annual increase. It is a clear reminder of how quickly the inflation picture can change when energy markets move.

Eurozone Inflation Stabilises as Energy Pressures Re-Emerge

That shift creates a more complicated backdrop for the ECB. While policymakers cannot directly control energy prices, they remain focused on how these shocks filter through the broader economy.

Higher fuel and input costs tend to feed into transport, manufacturing, and eventually wages. If that process takes hold, inflation becomes harder to bring back towards the 2% target, even if the initial driver sits outside domestic demand.

How Markets Are Responding

This is where the policy narrative begins to shift. Earlier expectations were built around a gradual move towards rate cuts as inflation cooled. Now, that path looks less certain.

Markets are increasingly pricing a policy rate closer to the 2.6% to 2.7% range, with roughly a 70% probability of another rate increase this year. The implication is not necessarily that growth is improving, but that inflation risks are proving more persistent than anticipated.

There is also an element of repositioning at play. It is not entirely clear whether this reflects a genuine change in the macro-outlook or simply a recalibration after earlier optimism around rate cuts.

Expectations may have moved ahead of the data, and the latest move in energy prices has forced a reassessment. Either way, the tone has shifted, and markets are approaching the ECB path with more caution.

Across assets, the response has been consistent with that adjustment. European bond yields have edged higher, particularly at the front end, with German two-year yields holding around the 2.6% level as rate expectations firm.

The euro has remained relatively stable against the dollar, supported by the view that policy may stay tighter for longer. Equity markets, however, have been more tentative, as higher energy costs raise concerns around margins and consumer demand.

Looking Ahead

The focus now turns to whether this energy-driven pressure proves temporary or more sustained.

Upcoming inflation data will be key, alongside any signals from the ECB on how it views second-round effects. At the same time, oil and gas markets remain the central variable.

For now, the message from markets is clear: the path towards easier policy in the eurozone has become less straightforward, and expectations are adjusting accordingly.