Record Highs Meet Rising Pressure | Weekly Recap: 18 - 22 May 2026

Markets pushed further into record territory last week before momentum finally began to show signs of strain as rising bond yields, renewed inflation concerns and geopolitical uncertainty triggered a sharp late-week reversal across risk assets.

The S&P 500, Nasdaq and Dow Jones Industrial Average all climbed to fresh all-time highs during the week, supported by resilient corporate earnings, continued enthusiasm surrounding artificial intelligence investment and generally stronger-than-expected US economic data.

However, beneath the surface, market leadership continued broadening beyond mega-cap technology as investors rotated toward inflation-linked and cyclical sectors. Rising Treasury yields, volatile oil prices and renewed Middle East tensions also created a more cautious macro backdrop by the end of the week.

Economic Overview

Economic data throughout the week continued reinforcing the view that the US economy remains relatively resilient despite restrictive monetary policy.

US flash manufacturing PMI surged to 55.3, its strongest reading since May 2022, while pending home sales rose 1.4% month-on-month.

At the same time, Federal Reserve minutes maintained a cautious tone, with several policymakers remaining open to additional policy firming should inflation pressures persist.

Outside the United States, economic momentum appeared softer. UK private-sector activity unexpectedly slipped into contraction territory for the first time in over a year, while Germany’s PMI data remained below expansion levels.

China’s economic recovery also continued losing momentum. Industrial production slowed to 4.1% year-on-year, retail sales rose just 0.2%, and property-market weakness extended into a 34th consecutive month of falling home prices.

Japan remained one of the few relative bright spots globally. First-quarter GDP expanded at an annualised 2.1%, beating expectations, although softer inflation data complicated expectations surrounding future Bank of Japan tightening.Core inflation slowed to 1.4% in April from 1.8% previously, remaining below the BOJ’s 2% target for a third consecutive month.

Equities, Bonds and Commodities

Equities

US equities remained firmly supported for most of the week before Friday’s selloff interrupted momentum.

The S&P 500 rose 0.9% for the week, extending its winning streak to eight consecutive weeks, its longest run since 2023. The Dow Jones gained 2.1%, briefly crossed the 50,000 level for the first time and recorded its ninth record close of 2026. The Nasdaq also advanced 0.45% despite late-week weakness across semiconductor stocks.

AI-related optimism and resilient earnings continued supporting equities throughout the week, with approximately 84% of S&P 500 companies reporting Q1 results beating analyst expectations. However, Friday saw renewed profit-taking across the technology sector as investors reassessed valuations following the recent AI-driven rally.

European equities delivered a more mixed performance. The Euro Stoxx 50 and DAX traded cautiously into the weekend as investors monitored rising oil prices and growing stagflation concerns across the region.

Bonds

Bond markets remained central to market sentiment throughout the week as investors reassessed Federal Reserve expectations amid persistent inflation pressures and stronger-than-expected US economic data.

The US 10-year Treasury yield climbed toward 4.59%, its highest level in almost a year, while the 30-year yield moved above 5.1%. The 2-year Treasury yield also rose to 4.13%, reinforcing higher-for-longer rate expectations following hawkish Fed commentary and resilient economic data.

The move higher in yields increased pressure across rate-sensitive sectors and reinforced the view that central banks may need to maintain restrictive policy settings for longer than previously anticipated.

Commodities

Commodity markets remained heavily influenced by geopolitical headlines throughout the week.

Oil prices experienced sharp volatility as traders reacted to developments surrounding US-Iran negotiations and the Strait of Hormuz. Brent crude traded above $103 per barrel during the week, while WTI crude remained near the $98 level before easing into the weekend. Despite the late pullback, oil still recorded strong gains earlier in the week amid renewed supply concerns.

Gold prices moved lower, falling roughly 0.3% on the week to around $4,510 as rising real yields reduced demand for defensive assets.

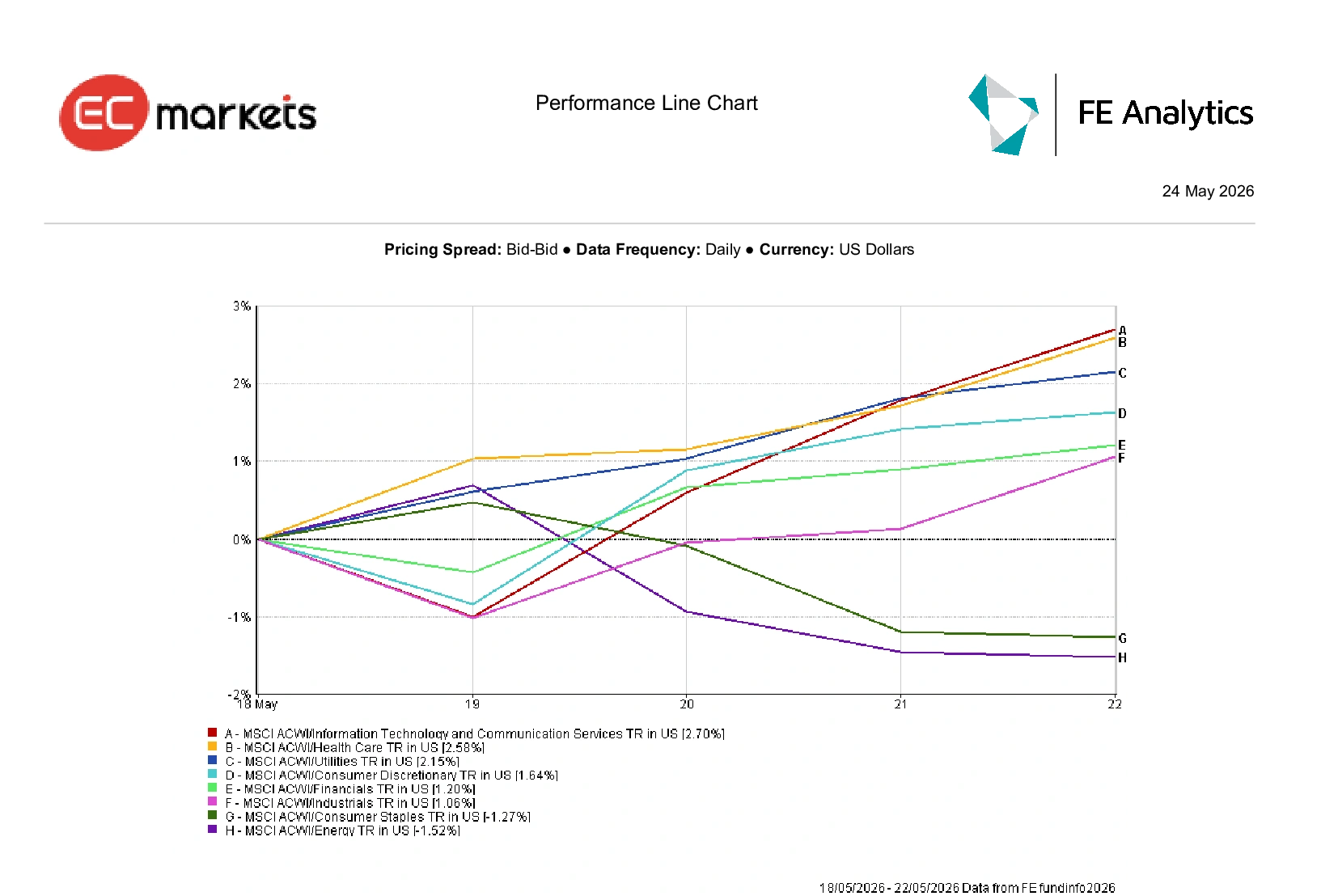

Sector Performance

Sector performance reflected a continued broadening of market leadership beyond concentrated mega-cap technology exposure.

Information Technology and Communication Services was the strongest-performing sector globally, rising 2.70% during the week as AI-related momentum and earnings resilience continued supporting sentiment.

Healthcare and Utilities also outperformed, gaining 2.58% and 2.15% respectively as investors rotated toward more defensive sectors amid rising market volatility.

Consumer Discretionary gained 1.64%, while Financials and Industrials rose 1.20% and 1.06% respectively.

Meanwhile, Consumer Staples declined 1.27%, while Energy fell 1.52% despite elevated oil-price volatility during the week.

Overall, sector rotation showed investors balancing AI-led growth exposure with more defensive positioning.

Sector Performance May 18th – 22nd 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 22 May 2026.

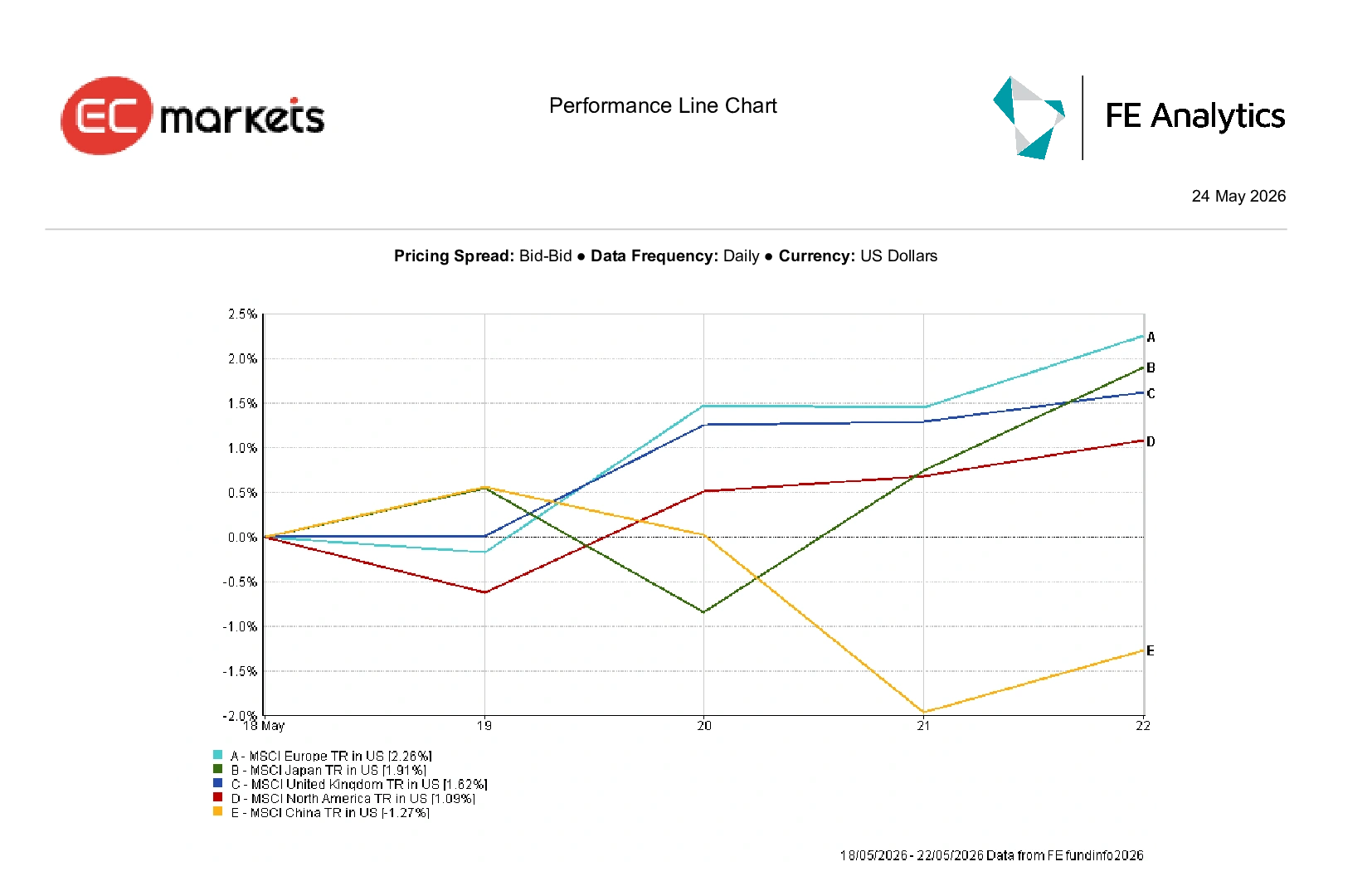

Regional Markets

Regional performance remained relatively resilient overall, although divergence between developed and emerging markets continued widening.

MSCI Europe was the strongest-performing major region, rising 2.26% during the week as financials and industrials helped support broader indices despite slowing economic momentum.

Japan gained 1.91% in USD terms following stronger-than-expected GDP data, while the UK rose 1.62%.

North America advanced 1.09% overall as continued AI leadership offset pressure from rising Treasury yields and Friday’s equity pullback.

China remained the weakest major region, declining 1.27% as slowing domestic demand and continued property-market weakness weighed on investor sentiment.

Regional Performance May 18th – 22nd 2026

Currency Markets

FX markets remained largely driven by rising Treasury yields, shifting central-bank expectations and geopolitical volatility throughout the week.

The US dollar index (DXY) edged 0.05% lower to 99.22, although higher Treasury yields continued supporting the higher-for-longer Federal Reserve narrative.

The Euro came under pressure during the week as disappointing economic data and weaker eurozone PMI readings reinforced concerns around slowing regional growth. EUR/USD opened the week near 1.1654 before closing lower around 1.1608, while rising energy-market risks and stagflation concerns further weighed on sentiment toward the single currency.

Sterling emerged as one of the stronger-performing major currencies during the week. GBP/USD rose from around 1.3300 to close near 1.3434 on Friday, gaining approximately 0.81%, as investors increasingly priced fewer Bank of England rate cuts relative to the Eurozone despite softer UK PMI data.

Meanwhile, USD/JPY posted a second consecutive weekly gain, rising toward 159.04 as softer Japanese inflation data pressured the yen and reduced expectations of near-term Bank of Japan tightening.

Bitcoin was broadly flat, rising 0.06% to trade near $77,460 as digital assets consolidated recent gains.

Overall, currency markets continued favouring yield advantage and relative economic resilience as investors navigated rising geopolitical and inflation uncertainty.

Outlook and The Week Ahead

Markets now move into another important macro week, with inflation data, central-bank expectations and geopolitical developments likely to remain the dominant drivers of sentiment.

Investors will closely monitor US Core PCE inflation data, Eurozone CPI releases and comments from Bank of Japan Governor Kazuo Ueda for further signals around the global interest-rate outlook. Upcoming earnings from Salesforce, Dell, Costco and Snowflake may also provide additional insight into enterprise spending trends and continued AI-related investment demand.

Meanwhile, developments surrounding US-Iran negotiations and oil markets are likely to remain central to broader risk sentiment following last week’s sharp commodity volatility.

While equities remain supported by resilient earnings and continued AI-driven optimism, rising bond yields, persistent inflation pressures and geopolitical uncertainty are creating a more fragile macro backdrop. For now, markets continue favouring economic resilience and momentum, although last week’s late selloff highlighted how quickly sentiment can shift when inflation, rates and oil-price risks move back into focus.