When a Cheap Stock Isn't Really Cheap: Understanding Value Traps

Looking Beyond Low Valuations

Many investors are naturally drawn to companies with low price-to-earnings (P/E) ratios. The logic appears straightforward: if a stock trades at a lower valuation than its peers, it must represent a bargain. After all, one of the core principles of value investing is buying quality businesses at attractive prices. However, not every cheap stock is genuinely undervalued. Some companies trade at low valuations because their businesses are deteriorating, their industries are undergoing structural change, or investors expect weaker earnings in the future. In these cases, what appears to be an attractive opportunity can become a costly mistake.

Professional investors refer to these situations as value traps. A value trap is a stock that appears inexpensive based on traditional valuation metrics but continues to disappoint investors because the underlying business keeps weakening.

What Is a Value Trap?

A value trap is a company whose low valuation reflects genuine business challenges rather than temporary market pessimism.

Investors are often attracted by low P/E ratios, low price-to-book ratios or unusually high dividend yields without fully understanding why the market has assigned those valuations. This highlights an important principle of fundamental analysis: valuation should never be assessed in isolation. It should always be considered alongside business quality, competitive positioning, financial strength and long-term earnings potential.

Buying a stock simply because it looks cheap ignores the underlying business.

Why Stocks Become Cheap

There are many reasons why a company’s valuation may decline. Falling earnings expectations, technological disruption, rising debt and weakening competitive advantages can all justify lower valuation multiples.

Markets are also forward looking. While many investors focus on the trailing P/E ratio, institutional investors often pay closer attention to the forward P/E, which reflects expected earnings over the next twelve months. A stock may therefore appear inexpensive based on historical profits while already pricing in weaker future earnings.

The key challenge for investors is determining whether these problems are temporary or permanent. Short-term setbacks such as economic slowdowns or supply chain disruptions may create genuine opportunities if the underlying business remains fundamentally strong. Structural problems, such as disruptive technologies or permanently declining demand, can justify lower valuations for many years.

Lessons from Intel, Nokia and Kodak

Several well-known companies demonstrate why low valuations do not always represent attractive investment opportunities.

Intel traded at relatively modest valuation multiples while annual revenue declined from approximately US$79 billion in fiscal 2021 to around US$54 billion in fiscal 2024v. Manufacturing delays and stronger competition from AMD and Nvidia raised concerns about its future competitiveness, causing investors to assign lower valuation multiples despite the company remaining profitable.

Nokia followed a similar pattern. Once controlling more than 40% of the global mobile phone market, Nokia failed to adapt to the smartphone revolution that followed Apple’s iPhone launch in 2007. As its competitive position deteriorated, the company experienced years of declining market share, weaker earnings and persistent share price underperformance.

Kodak represents perhaps the classic value trap. Despite inventing the first digital camera in 1975, the company failed to adapt its business model as digital photography replaced film. Its reluctance to disrupt its highly profitable film business ultimately led to bankruptcy protection in 2012, demonstrating that low valuations cannot compensate for a structurally obsolete business model.

These examples demonstrate that low valuation multiples often reflect genuine concerns about a company’s future rather than hidden value waiting to be discovered.

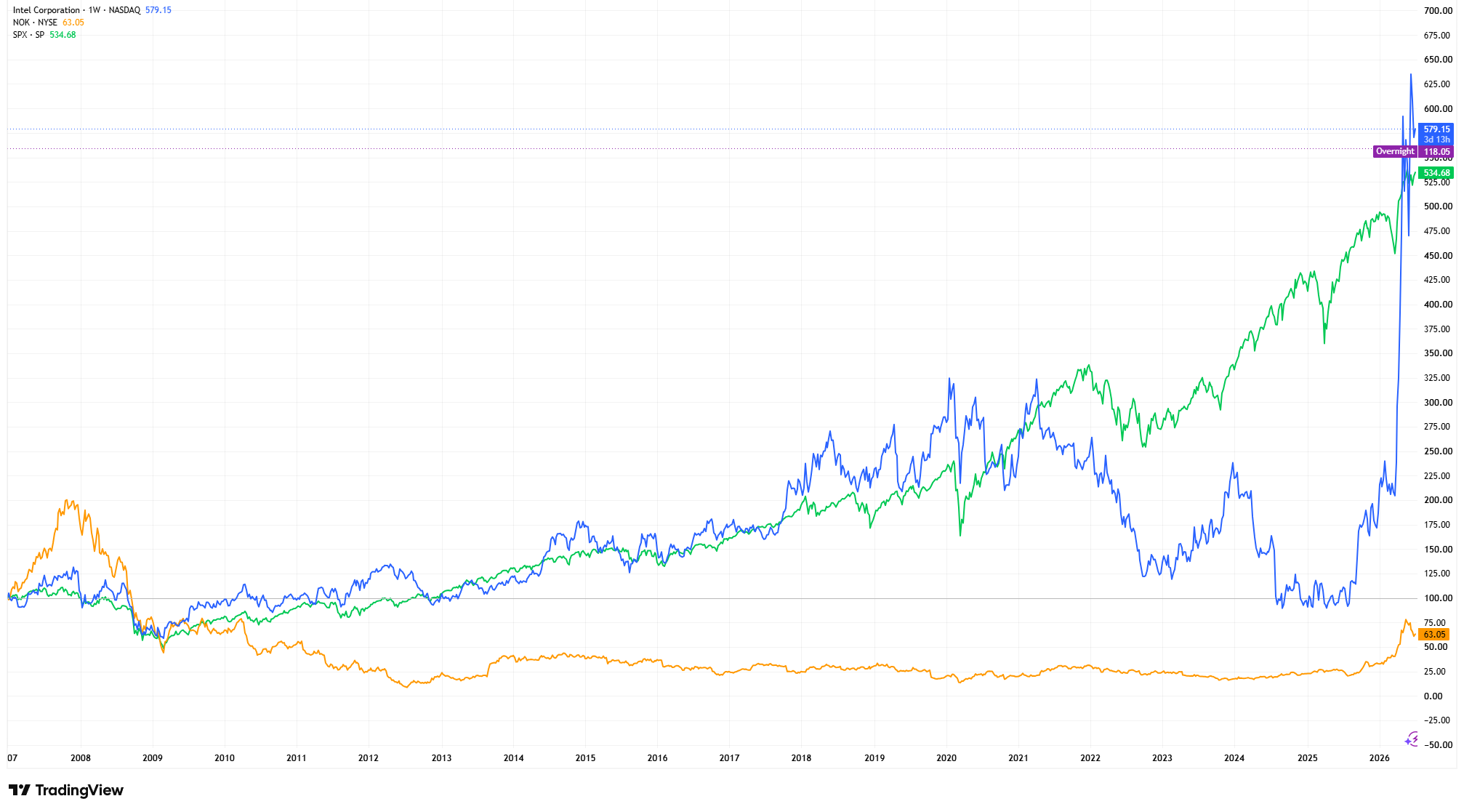

Intel, Nokia and the S&P 500: Indexed Share Price Performance (2007 = 100)

Source & Methodology: TradingView. Each price series has been indexed to 100 at the selected starting date in 2007 using the formula (Current Price ÷ Starting Price) × 100. Indexing standardises each series to a common starting point, allowing long-term shareholder performance to be compared on a like-for-like basis regardless of differences in absolute share prices. Past performance is not a reliable indicator of future performance. Data as of 1 July 2026.

By indexing each series to a common starting point, the chart illustrates how businesses facing structural competitive challenges can significantly underperform the broader market over extended periods, despite often appearing inexpensive based on traditional valuation measures. The objective is not to compare absolute share prices, but to demonstrate why understanding why a stock is cheap is just as important as recognising that it is.

How Professional Investors Avoid Value Traps

Professional investors rarely rely on valuation ratios alone. Instead, they evaluate revenue growth, earnings quality, free cash flow, Return on Invested Capital (ROIC), balance sheet strength, competitive advantages and management’s capital allocation decisions.

A company with a low P/E ratio but deteriorating cash flow, declining returns on capital and increasing debt may represent a far riskier investment than a higher-valued business with durable competitive advantages and stronger long-term earnings prospects. For this reason, valuation is often viewed as the final stage of analysis rather than the starting point.

If a Stock Looks Cheap, Shouldn’t I Buy It?

This is a common question among newer investors.

Not necessarily.

Successful investing is not about buying the cheapest companies. It is about identifying businesses whose future prospects are better than the market currently expects. Many value traps remain inexpensive for years because the underlying business continues to weaken, making patience and thorough research essential.

Bottom Line

Valuation remains one of the most important aspects of investing, but it should never be analysed in isolation.

Low P/E ratios, high dividend yields and discounted share prices do not automatically make a company an attractive investment. Investors should evaluate business quality, competitive advantages, cash generation, balance sheet strength and long-term earnings power alongside valuation.

Avoiding value traps can be just as important as identifying undervalued opportunities. For fundamental investors, the most important question is not whether a stock appears cheap, but why it appears cheap. Understanding that distinction can help investors separate businesses experiencing temporary setbacks from those facing permanent structural decline and make better long-term investment decisions.