Sticky Inflation Meets Falling Oil as Markets Rotate into Defensive Sectors | Weekly Recap: 22-26 June 2026

Markets ended the final full week of June balancing two competing forces. Stronger-than-expected US economic data reinforced expectations that interest rates could remain higher for longer, while a sharp decline in oil prices eased inflation concerns and encouraged investors to rotate into more defensive areas of the market. Although economic growth remained resilient, falling bond yields and weaker energy prices helped improve sentiment later in the week. However, investors continued reducing exposure to high-valuation technology stocks in favour of sectors offering more stable earnings and lower sensitivity to economic uncertainty.

Economic Overview

Markets ended the final full week of June balancing two opposing forces. Stronger-than-expected US economic data reinforced expectations that interest rates could remain higher for longer, while a sharp fall in oil prices later in the week eased inflation concerns and improved market sentiment.

In the US, the May Personal Consumption Expenditures (PCE) report, the Fed’s preferred inflation measure, showed headline inflation rising 0.4% MoM and 4.1% YoY, while core PCE increased 0.3% on the month and 3.4% annually. First-quarter GDP growth was revised higher to an annualised 2.1%, highlighting continued economic resilience despite higher borrowing costs. Elsewhere, durable goods orders fell 4.5% and the goods trade deficit widened to $105.8 billion. S&P Global’s flash June PMI also pointed to ongoing expansion, with manufacturing rising to 55.7 and the composite index reaching 52.2. Together, the data reinforced expectations that the Fed is likely to remain cautious on interest-rate cuts.

Across Europe, growth remained subdued. The euro area’s flash composite PMI improved to 49.5 but remained below the 50 threshold separating expansion from contraction, while Germany’s reading weakened to 48.0, its lowest level in 18 months. In the UK, the composite PMI slipped to 49.4, signalling softer business activity.

China continued to face weak domestic demand and pressure in the property sector, prompting the PBoC to leave its one-year and five-year loan prime rates unchanged at 3.00% and 3.50%. Japan presented a brighter picture, with manufacturing activity improving and Tokyo core CPI accelerating to 1.6%, supporting expectations that the BoJ will continue gradually normalising policy.

Equities, Bonds and Commodities

Global equity markets delivered mixed returns as investors reduced exposure to high-valuation technology stocks and rotated towards more defensive sectors.

In the US, the S&P 500 declined 2.05% and the Nasdaq Composite fell 4.7% as investors took profits in large-cap technology and AI-related companies. The Dow Jones Industrial Average gained 0.6%, supported by stronger performance from industrial, healthcare and financial stocks.

European markets proved more resilient. The STOXX Europe 600 finished broadly unchanged, the DAX declined around 1.3%, while the FTSE 100 gained approximately 1.4%, supported by banks and internationally diversified companies. In Asia, Japan’s Nikkei 225 fell roughly 2.7%, while Hong Kong’s Hang Seng dropped 5.2% and the Shanghai Composite lost 1.6%, reflecting continued concerns over China’s economic outlook.

Government bond yields eased despite persistent inflation. The US 10-year Treasury yield declined from 4.51% to 4.37%, while the two-year yield fell from 4.23% to 4.09%. Lower oil prices helped reduce inflation concerns, allowing yields to move lower despite expectations that interest rates may remain elevated.

Commodity markets were dominated by falling energy prices. Brent crude declined from $80.05 to $72.60 after shipping through the Strait of Hormuz resumed and supply concerns eased. Spot gold ended the week at $4,089.26, recovering from an intra-week low of $3,982.83 as lower bond yields encouraged renewed safe-haven demand.

Overall, cross-asset performance reflected a more selective investment environment, with investors favouring defensive sectors while reducing exposure to crowded growth trades.

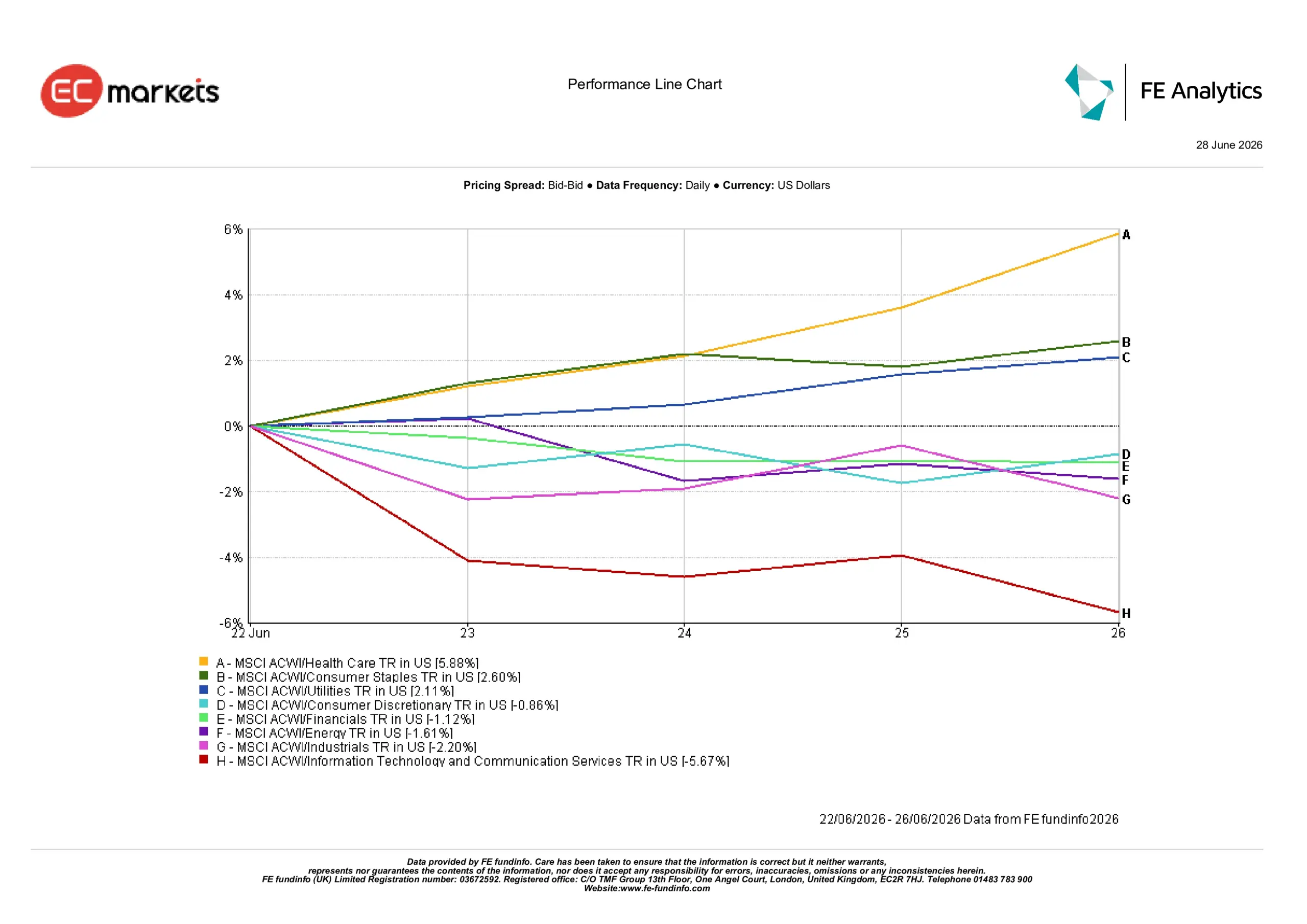

Sector Performance

Sector performance highlighted a clear shift towards defensive positioning as investors sought businesses with resilient earnings and lower sensitivity to economic uncertainty.

Healthcare led all sectors with a gain of 5.88%, followed by Consumer Staples (+2.60%) and Utilities (+2.11%).

Consumer Discretionary declined 0.86%, while Financials fell 1.12% as lower bond yields reduced support for banking shares. Energy lost 1.61% following the sharp decline in oil prices, and Industrials fell 2.20% amid concerns that slower global growth could weigh on future demand.

Information Technology & Communication Services was the week’s weakest performer, falling 5.67% as investors locked in profits following the sector’s strong gains earlier in the year and reassessed valuations across large-cap technology companies.

Sector Performance June 22nd – 26th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 26 June 2026.

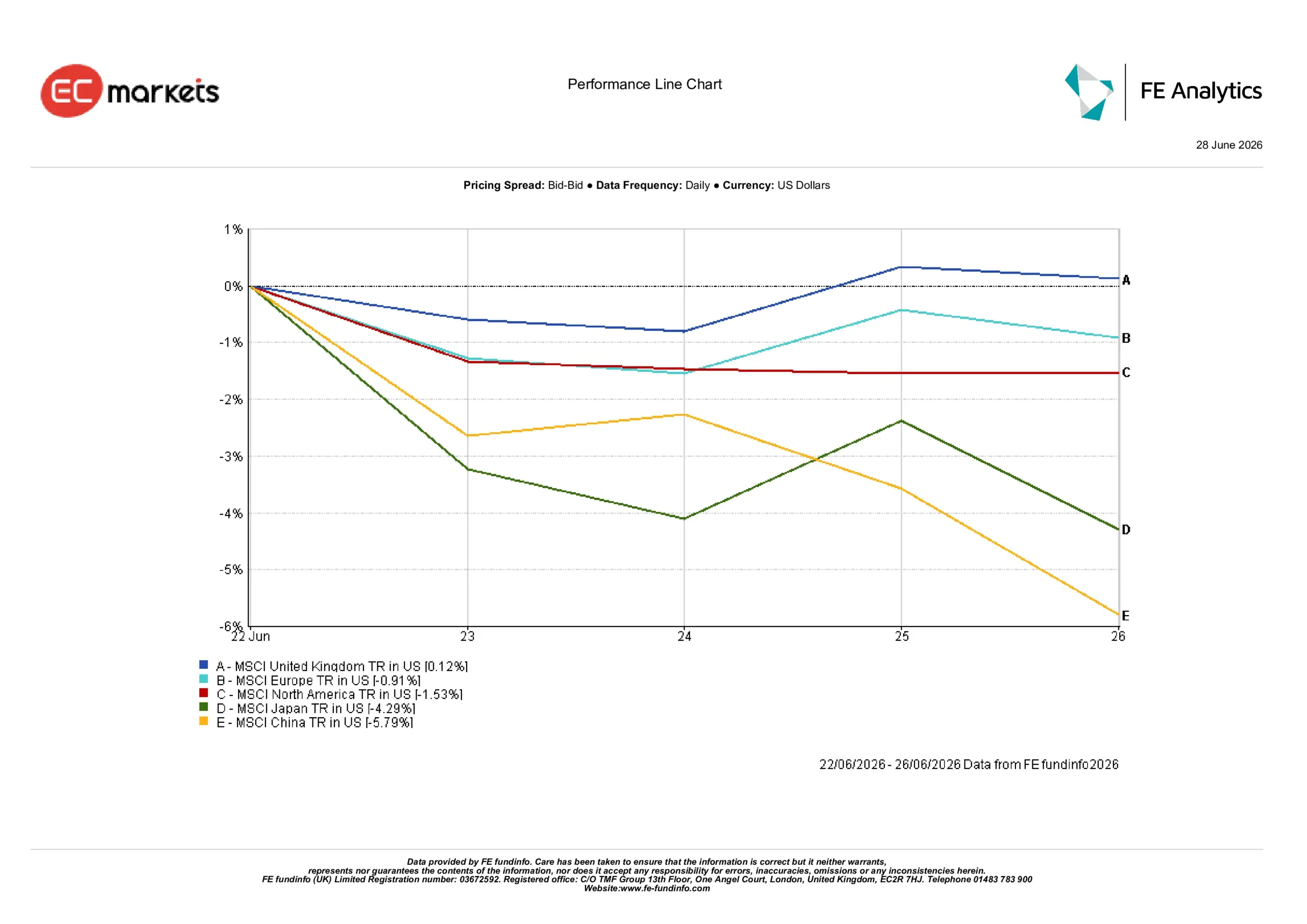

Regional Markets

Regional performance reflected differing economic conditions and investor sentiment.

The United Kingdom was the strongest performer, with the MSCI United Kingdom Index gaining 0.12% in US dollar terms. Its defensive market composition and internationally focused companies helped support returns despite domestic political uncertainty.

Europe declined 0.91%, weighed down by weak business activity and slowing industrial momentum, particularly in Germany. North America fell 1.53% as technology stocks came under pressure following the week’s profit taking.

Japan and China were the weakest-performing regions, declining 4.29% and 5.79% respectively. In Japan, technology weakness outweighed improving economic data, while China continued to struggle with weak domestic demand, property-sector challenges and limited policy support.

Overall, investors continued favouring markets with more resilient earnings and defensive characteristics.

Regional Performance June 22nd – 26th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 26 June 2026.

Currency Markets

Currency markets reflected changing expectations around interest rates and economic growth.

EUR/USD fell from 1.1467 to 1.1384 as weaker euro area economic data reduced expectations of further ECB tightening.

GBP/USD edged slightly higher from 1.3197 to 1.3203, recovering after early weakness as investors looked beyond political developments in the UK.

USD/JPY rose from 161.26 to 161.76 as the wide interest-rate differential between the US and Japan continued supporting the dollar.

GBP/JPY edged higher from 213.47 to 213.56, reflecting sterling’s relative stability against a weaker yen.

Overall, currency markets reflected a broadly resilient US dollar, although easing bond yields limited further upside by the end of the week.

Outlook and The Week Ahead

Looking ahead, investors will continue assessing whether easing energy prices can help slow inflation without significantly weakening economic growth. Labour-market data, inflation releases and central-bank communication will remain key drivers of market sentiment.

The past week highlighted an increasingly selective investment environment. Investors are placing greater emphasis on resilient earnings, reasonable valuations and defensive sectors while remaining cautious towards areas more exposed to slowing growth and elevated interest rates. Whether this rotation continues will depend on the balance between incoming economic data, inflation trends and central-bank expectations in the weeks ahead.