Ceasefire Holds as Markets Reprice Energy Risk and Rotate Back into Growth | Weekly Recap: 13-17 April 2026

Global markets rallied last week as lower oil prices and an open Strait of Hormuz helped unwind crisis pricing and improve risk sentiment. Equities led gains, yields eased, and investors rotated back into growth sectors, although renewed geopolitical tensions continue to threaten the recovery.

Economic Overview

Markets spent last week assessing whether the sharp energy-driven volatility seen earlier in April had peaked, and whether conditions were in place for a broader normalisation in risk assets.

At the centre of that shift was the Strait of Hormuz remaining open throughout the week. While the immediate supply shock faded, conviction around a sustained recovery remained tentative.

That caution was reinforced by a softer global growth backdrop. The IMF revised its 2026 global growth forecast down to 3.1%, warning that prolonged disruption in energy supply could push the global economy closer to a 2.5% downside scenario.

In the US, March producer prices rose 0.5% m/m, below expectations of 1.1%, while import prices increased 0.8% against forecasts of 2.0%. This suggested a more limited pass-through from higher oil prices, although policymakers continued to warn of delayed effects on broader inflation.

Across Europe and the UK, the policy backdrop remained complex, with slowing growth and persistent inflation concerns. In Asia, China’s 5.0% y/y GDP growth provided some support, though weak consumption and property trends highlighted uneven demand, while the BoJ maintained a gradual policy stance.

Overall, the macro environment shifted toward cautious stabilisation, but remained fragile and highly sensitive to renewed energy disruption.

Markets Overview

Equities

Global equities moved from cautious recovery to a more decisive risk-on tone as the week progressed.

US

In the US, the S&P 500 rose 4.53%, while the Nasdaq gained nearly 7% and the Dow Jones Industrial Average advanced 3.2%. Falling oil prices eased concerns around inflation and financial conditions, allowing investors to rotate back into longer-duration assets.

Europe

European equities also performed strongly. The STOXX Europe 600 extended its gains, supported by the direct benefit of lower energy costs on the region’s inflation outlook. Germany’s DAX outperformed as investors rebuilt exposure to industrial and export-oriented sectors, while the FTSE 100 posted more modest gains due to its heavier weighting toward energy producers.

Asia

In Asia, performance was more mixed but broadly constructive. Japan’s Nikkei 225 reached record highs before consolidating, supported by global risk appetite and a stable policy outlook from the BoJ. Chinese equities advanced on stronger growth data, though gains were more measured as concerns around domestic demand persisted.

Bonds

Bond markets reflected a partial unwinding of inflation risk. US Treasury yields declined into the end of the week, with the 10-year falling to 4.246% and the 2-year to 3.7%, as softer inflation data and lower oil prices reduced the urgency for further tightening. In Europe, yields also eased as expectations for additional policy tightening were pushed further out.

Commodities

Commodity markets delivered the clearest signal of shifting sentiment. Brent crude fell 9% to $90.38, while WTI dropped over 11% to $83.85, reflecting a rapid unwind of geopolitical risk premia. Gold remained supported, suggesting underlying uncertainty has not fully dissipated.

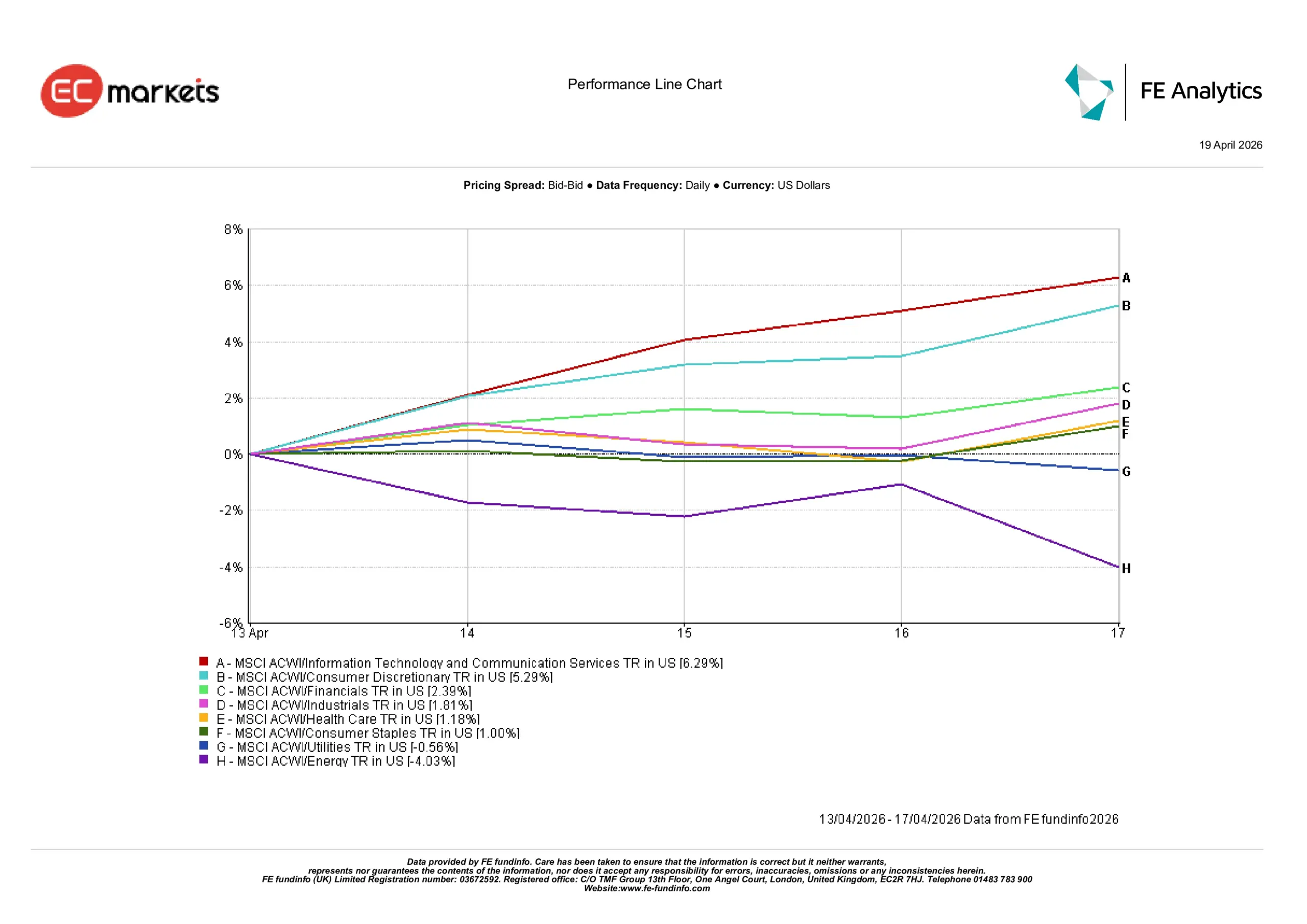

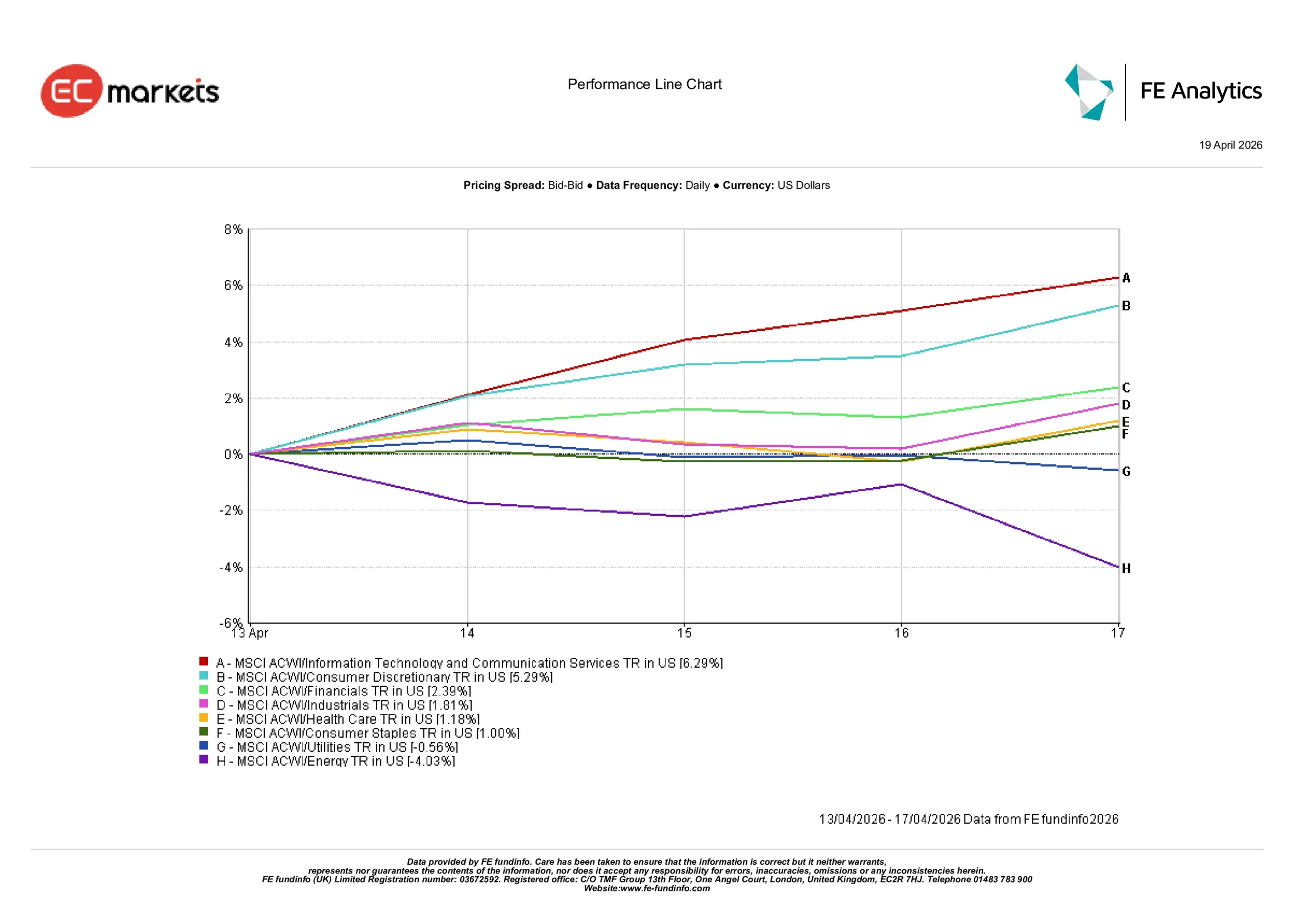

Sector Performance

Sector performance followed a clear pro-cyclical rotation, led by growth-sensitive sectors as falling yields improved conditions for longer-duration assets.

Information Technology & Communication Services led gains, advancing 6.29% for the week. Consumer Discretionary followed with a gain of 5.29%, while Financials rose 2.39% as investors moved back into economically sensitive sectors. Industrials also advanced, gaining 1.81%, reflecting a stabilisation in growth expectations as energy prices declined.

Defensive sectors lagged the broader market move. Healthcare and Consumer Staples posted modest gains of 1.18% and 1.00% respectively, while Utilities declined 0.56%, indicating a gradual rotation away from defensive positioning.

Energy was the clear underperformer, falling 4.03% as crude oil prices dropped sharply. The decline underscored how much of the sector’s recent strength had been driven by geopolitical risk rather than underlying demand.

Overall, the pattern suggests investors were selectively rebuilding exposure to growth and cyclical sectors, while reducing positions in both defensives and energy-linked trades.

Sector Performance

Regional Markets

Regional performance reflected differing sensitivities to energy prices and global growth expectations.

North America led gains, with MSCI North America rising 3.49% in US dollar terms, supported by strong performance in technology and earnings resilience.

China followed with a gain of 3.38%, as stronger GDP data helped stabilise sentiment despite ongoing concerns around domestic demand. Europe advanced 2.93%, benefiting from the decline in oil prices and its impact on inflation expectations.

Japan rose 2.44%, supported by global risk appetite and a stable policy outlook, while the UK lagged slightly, gaining 1.45%, as the FTSE’s exposure to energy limited the upside from falling oil prices.

The regional divergence highlighted that markets with greater sensitivity to energy costs and growth recovery benefited most from the shift in sentiment.

Regional Performance

Currency Markets

Foreign-exchange markets reflected a modest unwind of safe-haven US dollar positioning. As geopolitical tensions eased and oil prices declined, the dollar softened, although moves were more measured than in the previous week.

EUR/USD rose from 1.1759 to a high near 1.1849 before settling at 1.1764, while GBP/USD increased from 1.3506 to 1.3601 before ending the week at 1.3517. Both pairs reflected improved risk sentiment but also some late-week consolidation.

The yen strengthened modestly, with USD/JPY declining from 159.45 to 158.64, although gains remained limited by persistent rate differentials. GBP/JPY edged lower from 215.36 to 214.42, reflecting relative strength in the yen.

Overall, FX markets reinforced the broader narrative of easing risk while still reflecting underlying policy divergence.

Outlook and The Week Ahead

The coming week will test whether the market’s shift back toward risk can hold in the face of renewed geopolitical uncertainty. While lower oil prices supported last week’s rotation into growth and cyclical assets, weekend developments have already begun to challenge that narrative.

Reports of a re-closure of the Strait of Hormuz following renewed tensions between Iran and the US suggest the easing in energy prices may prove temporary rather than structural. As a result, the relief rally seen at the end of last week may face immediate pressure at the start of trading, with the potential for a more cautious tone to return across global markets.

Alongside geopolitical developments, investors will also focus on key economic data. Flash PMIs will provide an updated read on global activity and pricing pressures, while inflation releases from Japan and the UK will offer further insight into the persistence of cost pressures. US earnings will also remain central, particularly in assessing whether corporate margins can absorb recent volatility in input costs.

If energy markets stabilise despite the latest developments, risk sentiment may hold and allow the rotation into growth sectors to continue. However, if oil prices reprice higher once again, the past week’s moves may look less like the start of a new trend and more like a temporary unwind of positioning.

The key question for investors is no longer whether energy pressures have eased, but whether they can remain contained long enough to prevent another tightening in financial conditions.