Why Bonds Now Drive Equity Markets

For many years, investors tended to treat bonds as the backdrop and equities as the headline. That is harder to argue today. In the US, the 10-year Treasury yield stood at 0.52% on 4 August 2020, rose to 4.26% on 17 April 2026, and briefly moved above 5% in October 2023. The benchmark cost of money has shifted significantly, and investors now watch government yields almost as closely as they watch stock indices.

The Shift in Market Leadership

Traditionally, equities were discussed mainly through earnings growth, economic expansion, and risk appetite, while bond markets were seen as a clearer reflection of inflation and central bank policy. In that lower-inflation environment, the relationship between stocks and bonds was often stabilising rather than disruptive.

In simple terms, when equities struggled, bonds often provided support, helping balance overall portfolios. That relationship held for much of the period between 2000 and 2019, when inflation remained relatively contained.

The post-pandemic inflation shock changed that balance. As inflation accelerated, central banks tightened policy and raised interest rates at a pace not seen for years. By March 2026, the Fed’s target range stood between 3.5% and 3.75%, while its balance sheet had fallen to around $6.7 trillion from close to $9 trillion at its 2022 peak.

That shift matters because it has brought the cost of capital back into focus. When interest rates were close to zero, changes in yields had a limited impact on equity valuations. Today, those same moves carry much more weight.

How Bond Yields Influence Equity Valuations

Bond yields now sit at the centre of how equities are valued. Equity prices reflect expected future earnings and the rate used to discount those earnings back to today’s value.

When yields rise, that discount rate increases, which reduces the present value of future cash flows. This tends to weigh more heavily on growth stocks, where a larger share of expected returns lies further in the future.

Even if company earnings remain strong, higher yields can still put pressure on equity prices by changing how those earnings are valued.

Risk Appetite, Capital Flows, and Market Behaviour

Higher yields also influence investor behaviour. When government bonds offer returns closer to 4% or 5%, they become a more meaningful alternative to equities than they were in a near-zero rate environment.

As yields rise, some investors may reduce exposure to risk assets and move toward bonds. When yields fall, the opposite can happen, with capital flowing back into equities in search of higher returns.

Recent trading has underlined this relationship. Stronger-than-expected US economic data has often pushed yields higher, which in turn has weighed on equity markets as expectations for rate cuts are pushed back. Conversely, easing inflation pressures have tended to support bonds and provide relief for equities.

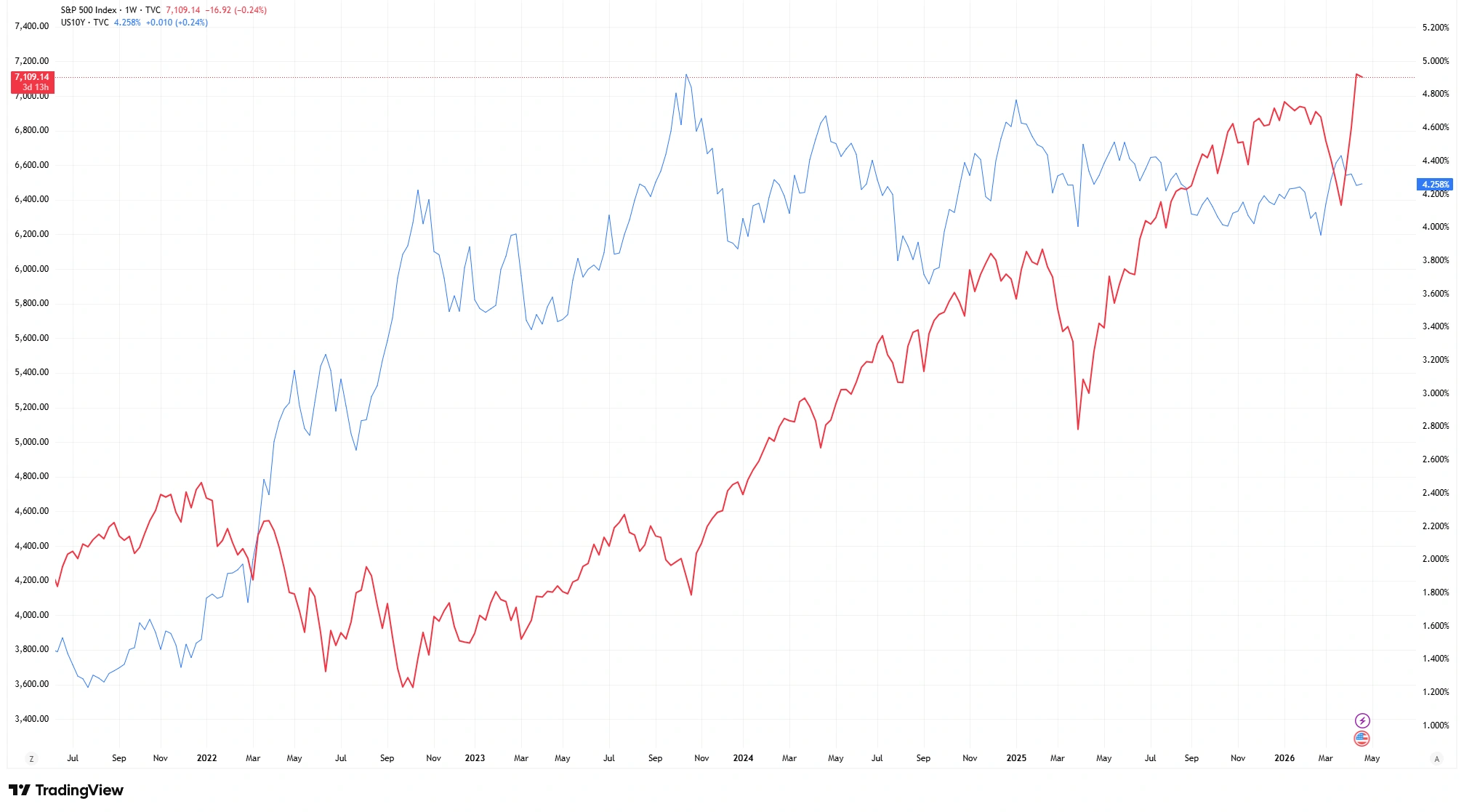

S&P 500 vs US 10-Year Treasury Yield

Rising Treasury yields have increasingly coincided with periods of equity market pressure, highlighting the growing influence of bond markets on equity performance.

The relationship is not perfect every day, but the pattern is becoming harder to ignore.

Why It Matters in Today’s Market

Markets today are more sensitive to interest rates than they were during the previous low-rate decade. This means bond markets are no longer just reflecting economic conditions, they are actively shaping them.

At the same time, this relationship is not one-directional. Strong earnings growth can still support equities even when yields are rising. That balance remains important.

Rising yields can also increase volatility. If bond markets move sharply or unexpectedly, equity markets can react quickly as investors reassess valuations and risk.

Bottom Line

Bond markets have become more central to equity performance because they influence discount rates, investor behaviour, borrowing costs and capital allocation at the same time.

In a world of higher inflation uncertainty, rising interest rates and reduced central bank support, the bond market no longer sits in the background. It increasingly helps set the direction for broader financial markets.

For investors, understanding movements in bond yields is now an essential part of interpreting where equity markets may move next.

Frequently Asked Questions

Why do bond yields affect stock prices?

Bond yields influence the discount rate used to value future corporate earnings. When yields rise, future cash flows are worth less in today’s terms, which can pressure stock valuations.

Why do growth stocks react more to rising yields?

Growth companies often rely on earnings expected further in the future. Higher yields reduce the present value of those future earnings more sharply.

What is the US 10-year Treasury yield?

The US 10-year Treasury yield is the return investors receive for holding US government debt for ten years. It is widely viewed as a benchmark for borrowing costs and market expectations.

Can stocks rise while bond yields are increasing?

Yes. Strong earnings growth, improving economic data or positive sentiment can support equities even when yields are rising.

Why are bond markets more important now?

After years of near-zero rates, higher inflation and tighter central bank policy have made interest rates more influential across valuations, borrowing costs and capital flows.