Ceasefire Rally Unwinds Oil Shock and Weakens Dollar | Weekly Recap: 6-10 April 2026

Global markets rallied last week as easing geopolitical tensions triggered a relief rally across equities, weakened the US dollar, and pushed oil prices sharply lower.

The ceasefire-driven unwind of the energy shock improved risk sentiment, but investors remain alert to renewed volatility as inflation and geopolitical risks continue to shape the macro outlook.

Economic Overview

Markets entered the week trading largely on the geopolitical narrative surrounding the Middle East, with investors focused on whether tensions between the US and Iran would evolve into a prolonged disruption of global energy flows.

Oil prices had surged in the previous week as markets priced a higher probability of supply interruptions through the Strait of Hormuz, raising concerns that a renewed energy shock could reinforce inflation pressures just as central banks were attempting to stabilise financial conditions.

Against that backdrop, risk sentiment remained cautious during the opening sessions of the week. The turning point arrived mid-week, when reports of a two-week ceasefire agreement between the US and Iran triggered a sharp shift in global positioning.

Oil prices moved lower as the immediate disruption risk was repriced, and that adjustment quickly filtered through other asset classes.

Lower energy prices eased near-term inflation expectations and reduced pressure on sovereign bond yields, creating space for global equities to rally and for risk appetite to recover.

Economic data then provided a further test of the macro narrative later in the week. In the US, March CPI showed headline inflation rising 0.9% MoM and 3.3% YoY, largely driven by energy costs. However, core inflation increased only 0.2% on the month and 2.6% annually, allowing markets to interpret the spike as concentrated in energy rather than evidence of a broad inflation resurgence.

In the euro zone, business surveys indicated that higher energy costs continued to weigh on industrial activity, while policymakers at the ECB reiterated their cautious approach to policy normalisation. In the UK, the BoE continued balancing persistent wage pressures against a slowing growth backdrop.

The ceasefire eased immediate geopolitical risk and supported global risk assets, but with energy still a key inflation driver, markets remain highly sensitive to renewed volatility in oil prices.

Markets Overview

Equities

Global equities recorded a strong week as easing geopolitical tensions triggered a broad risk-on rotation across markets. In the United States, the S&P 500 rose around 3.6% over the week, while the Nasdaq gained 4.7% and the Dow Jones Industrial Average advanced roughly 3%. Much of the rally was concentrated around the mid-week ceasefire announcement.

European equities also benefited from the repricing of energy risk. The STOXX Europe 600 surged sharply following the ceasefire headlines, recording its strongest single-day gain in more than four years before consolidating toward the end of the week.

In Asia, markets followed the same global risk-on pattern but with regional variations. Japan’s Nikkei 225 delivered one of the strongest performances among developed markets, supported by strength in technology stocks and renewed optimism around corporate earnings. Chinese equities also advanced, with the Shanghai Composite rising as improving producer-price dynamics and stabilising external conditions supported risk appetite.

Bonds

Bond markets reflected the evolving inflation narrative. US Treasury yields remained relatively contained despite the strong headline CPI reading. The 10-year Treasury yield hovered around 4.3%, while the two-year yield remained near 3.8% as investors weighed the energy-driven inflation spike against softer core inflation. In Europe, Germany’s 10-year Bund yield moved modestly higher to around 3.02%.

Commodities

Commodity markets delivered the clearest signal of the geopolitical repricing. Brent crude fell from roughly $110 per barrel at the start of the week to the mid-$90s by Friday, reflecting the rapid compression of the geopolitical risk premium once ceasefire headlines emerged. Gold remained supported by the weaker US dollar and shifting interest-rate expectations, ending the week up roughly 1.7%.

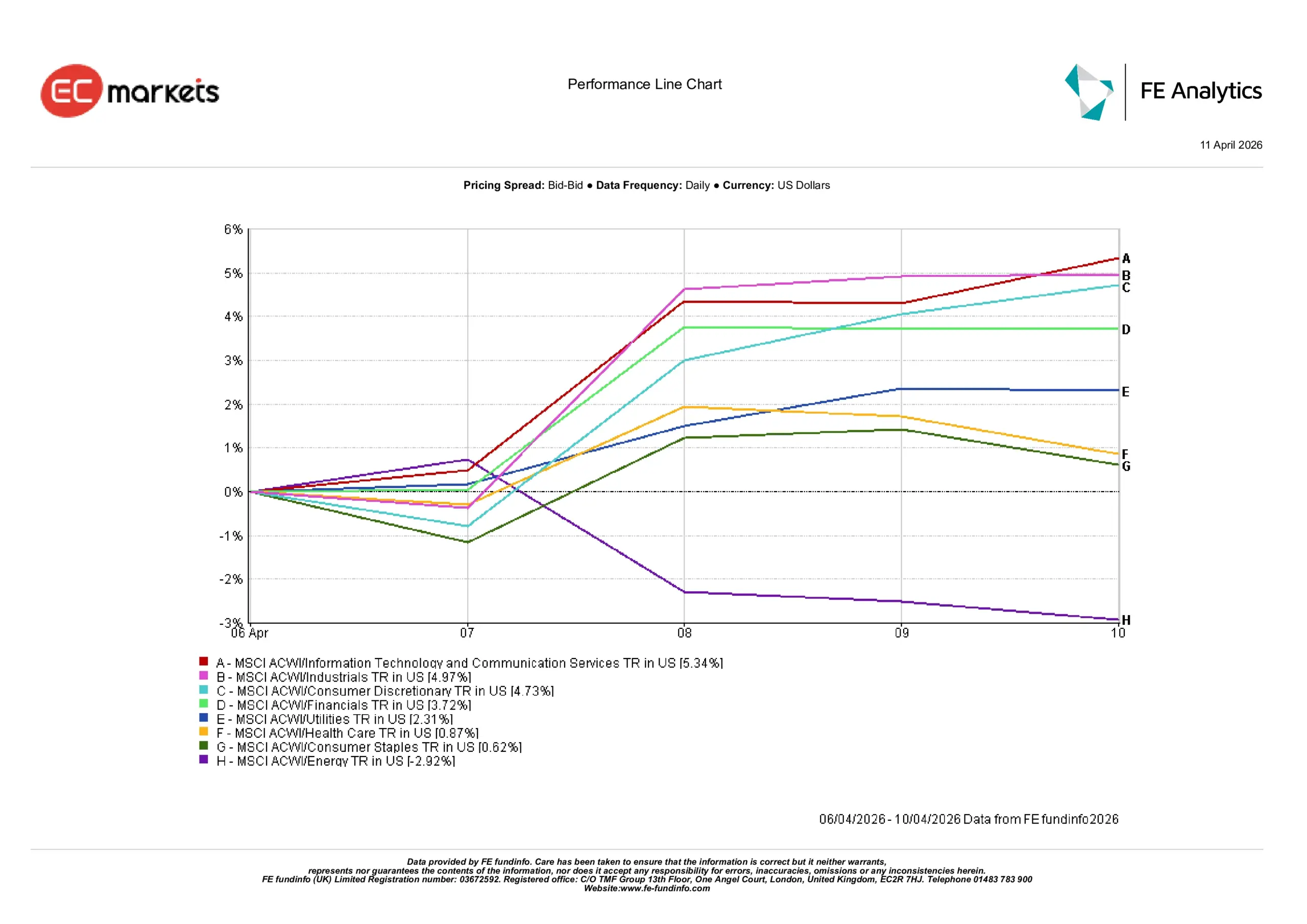

Sector Performance

Sector performance highlighted a clear rotation back toward growth-sensitive and cyclical sectors following the easing of geopolitical tensions and the decline in oil prices.

Information Technology and Communication Services led global sector gains, advancing 5.34% for the week. Industrials followed closely with a gain of 4.97%, while Consumer Discretionary rose 4.73% as investors rebuilt exposure to economically sensitive sectors.

Financials also participated in the rally, advancing 3.72% as the moderation in energy prices helped stabilise expectations around inflation and interest-rate policy.

Defensive sectors lagged the broader market move. Utilities gained 2.31%, while Health Care and Consumer Staples posted more modest increases of 0.87% and 0.62% respectively.

Energy was the clear underperformer during the week, declining 2.92% as crude oil prices fell sharply following the ceasefire announcement.

Overall, the sector rotation suggested investors temporarily shifted from an inflation-hedging posture toward rebuilding exposure to growth and cyclical areas of the equity market.

Sector Performance

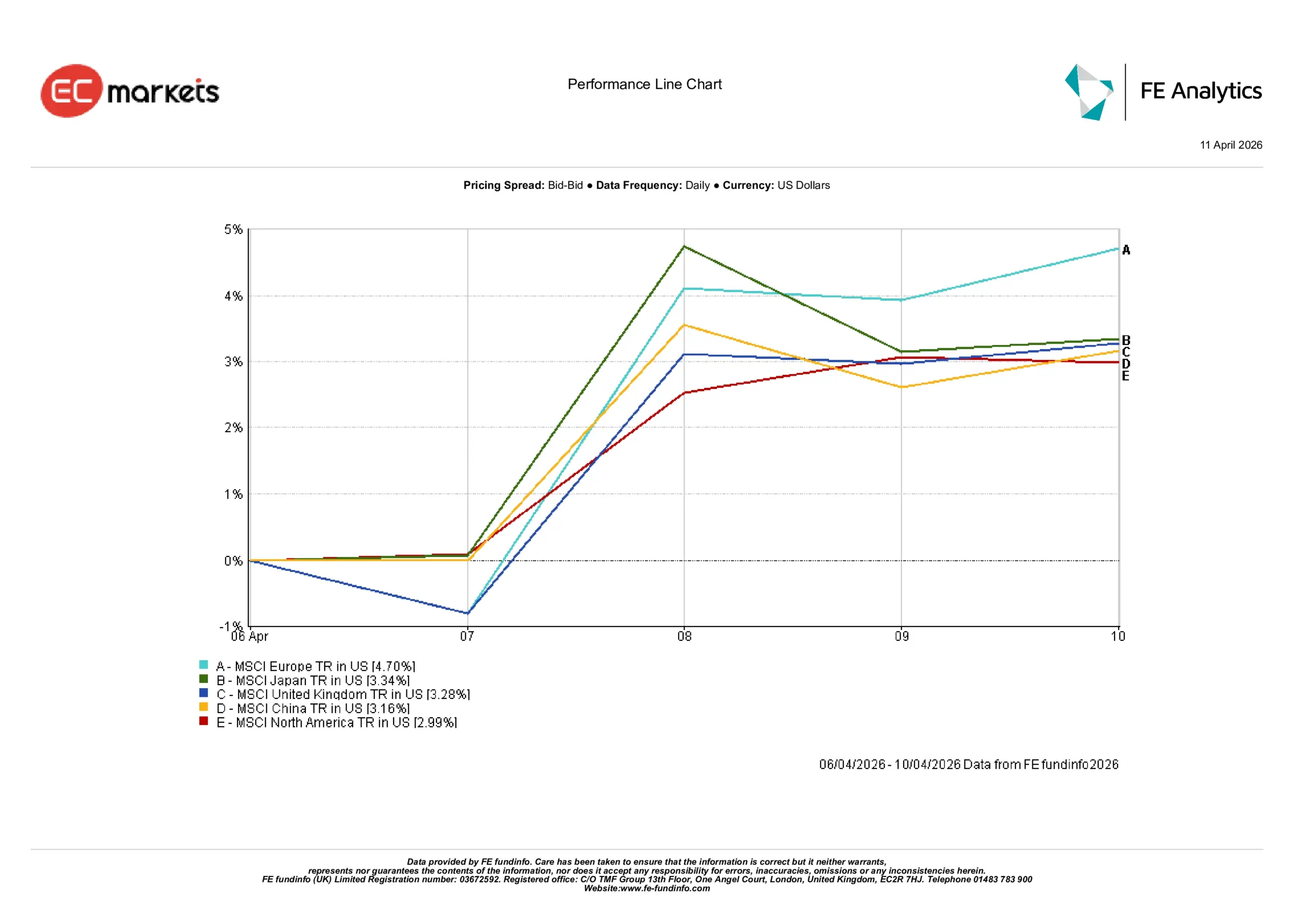

Regional Markets

Regional equity performance reflected the global relief rally, while also highlighting differences in how markets responded to easing energy-price pressures.

Europe emerged as the strongest performer for the week, with MSCI Europe rising 4.70% in US dollar terms. Japan followed with a gain of 3.34%, supported by strong performance in export-oriented sectors and continued optimism around corporate earnings growth.

The United Kingdom also posted solid gains, with MSCI UK advancing 3.28% as global risk sentiment improved. China recorded a weekly gain of 3.16%, with improving producer-price dynamics and stabilising global demand expectations helping support equity markets. Meanwhile, North America rose 2.99% over the week.

The regional pattern suggested markets most exposed to easing energy pressures and improving global sentiment delivered the strongest relative performance.

Regional Performance

Currency Markets

Foreign-exchange markets reflected a clear unwinding of the safe-haven US dollar positioning that had built up during the earlier phase of the energy shock. As geopolitical tensions eased and oil prices moved lower, the dollar weakened broadly against major currencies.

The euro and sterling both strengthened significantly during the week. EUR/USD rose from 1.1542 on 6 April to 1.1720 by 10 April, while GBP/USD advanced from 1.3234 to 1.3462.

The Japanese yen displayed a more nuanced pattern, with USD/JPY edging lower from 159.69 to 159.30 across the week. Sterling’s broader strength was particularly evident in cross-rates, with GBP/JPY rising from 211.33 to 214.44.

Overall, FX markets reinforced the broader macro narrative of the week: easing geopolitical risk and lower oil prices encouraged a rotation away from the US dollar.

Outlook and The Week Ahead

Looking ahead, market sentiment will likely remain closely tied to developments in the Middle East and the durability of the recently announced ceasefire. If the agreement translates into a sustained easing of tensions and stabilisation of energy flows, oil prices may continue to moderate.

However, the ceasefire remains fragile. As a result, investors are likely to maintain flexible positioning rather than assume the latest rally represents a full reset of the macro environment.

On the economic calendar, attention will shift toward upstream inflation indicators. The United States will release March Producer Price Index data on 14 April, followed by import and export price figures on 15 April.

Beyond the United States, markets will also focus on growth updates from major economies, including GDP data from the United Kingdom and China, alongside additional inflation and industrial production indicators across the euro zone and Asia.

For investors, the key question remains whether the recent recovery in risk assets can continue without either a renewed spike in energy prices or a more pronounced deterioration in global growth indicators.