Why Cash Still Matters in a Portfolio

Cash is often overlooked when markets are rising and investment returns are attracting attention. Compared with equities, bonds or other investment assets, cash can appear less exciting because its primary purpose is not growth.

However, cash continues to play an important role in financial planning. Beyond providing access to money when it is needed, cash can offer stability, flexibility and resilience during periods of uncertainty.

Understanding why cash remains valuable can help put its role within a broader financial strategy into perspective.

Why Cash Still Matters

When stock markets are performing strongly, cash can easily seem unexciting.

Many people view money sitting in a bank account as “doing nothing” compared with investments such as equities, bonds or gold. However, despite its lack of growth potential, cash continues to play an important role in personal finance and portfolio management.

Rather than being a tool for generating returns, cash is primarily about flexibility, stability and preparedness. It provides immediate access to funds when they are needed and can help households and investors navigate periods of uncertainty without disrupting longer-term plans.

What Is Cash and Liquidity?

In a financial context, cash means more than the notes and coins in your wallet.

It can also include money held in current accounts, savings accounts, money market funds and other highly liquid assets.

The key characteristic of cash is liquidity. Liquidity refers to how quickly and easily money can be accessed without needing to sell investments or wait for assets to be converted into cash.

Unlike shares, property or long-term investments, cash is generally available immediately when needed. This accessibility is one of the reasons cash remains an important part of many financial plans.

Why Do People Hold Cash?

Cash serves several important purposes.

First, it provides a financial buffer against unexpected expenses. Medical bills, vehicle repairs, home maintenance costs or temporary income disruptions can arise without warning, and having readily available funds can help cover these costs without creating additional financial pressure.

Cash can also support planned short-term spending.

For example, money intended for an upcoming holiday, tuition payment or house deposit may be kept in cash because the funds will be needed within a relatively short timeframe.

Beyond personal finances, cash can provide reassurance during periods of market uncertainty. When investment markets become volatile, cash generally maintains its nominal value, giving investors flexibility while they assess changing conditions.

The Trade-Off Between Liquidity and Growth

While cash offers stability and accessibility, it also comes with limitations.

Over long periods, cash has historically generated lower returns than many investment assets.

One reason is inflation. Across many developed economies, inflation has averaged roughly 3% per year over the long term. This means that if cash returns fail to keep pace with inflation, purchasing power gradually declines over time.

This introduces the concept of opportunity cost.

Money held entirely in cash may miss the long-term growth potential available through other asset classes. Over long periods, holding large amounts of cash can limit overall portfolio growth because cash typically generates lower returns than many investment assets.

At the same time, holding no cash at all can create challenges if unexpected expenses arise or if investments need to be sold during a market downturn.

Finding the balance between stability and growth is one of the key considerations when thinking about cash within a broader financial framework.

How Cash Behaves During Market Downturns

Cash often behaves differently from other assets during periods of market stress.

While equities and other risk assets can experience significant price fluctuations, cash generally remains stable in nominal terms.

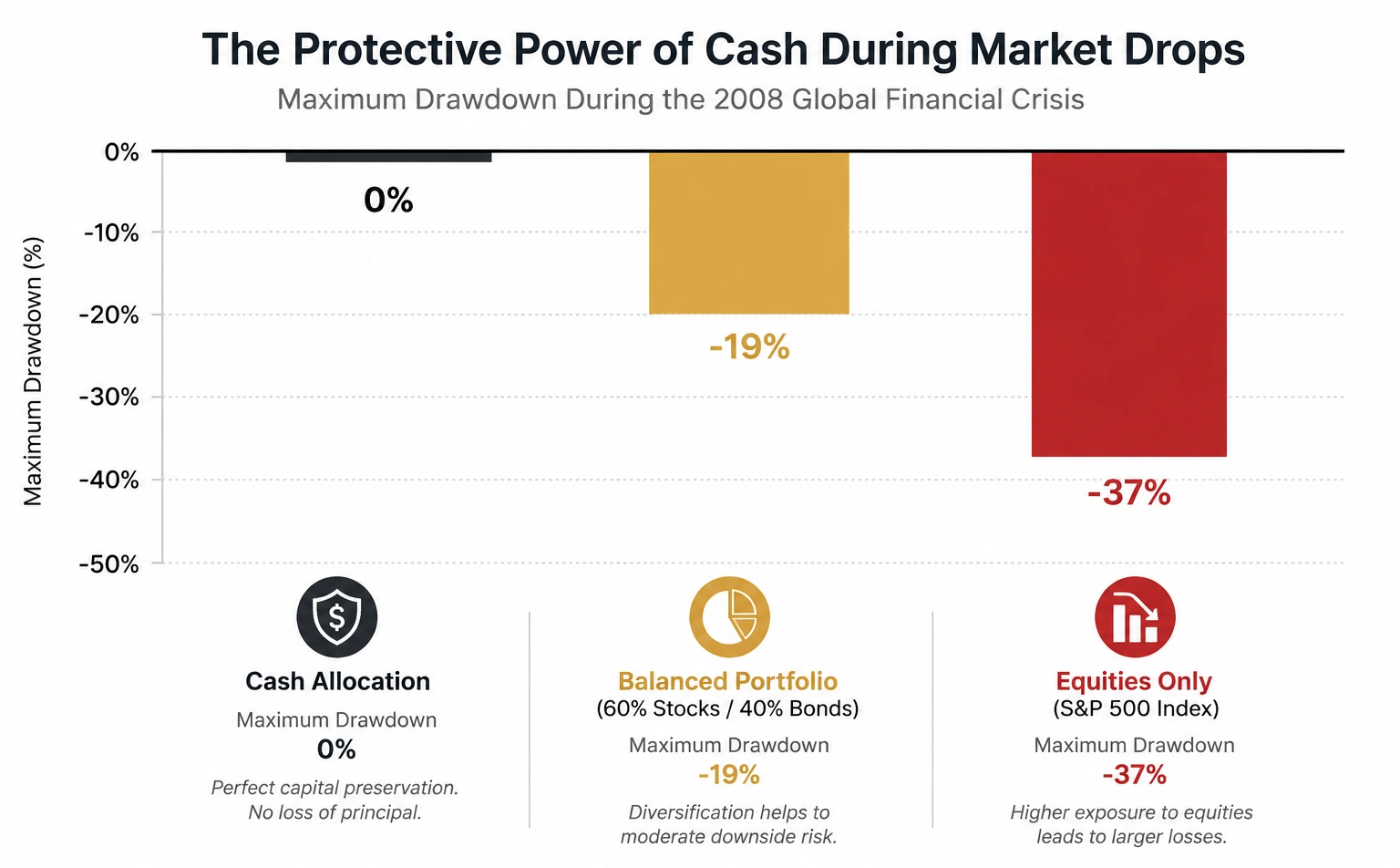

During the 2008 Global Financial Crisis, for example, a traditional portfolio consisting of 60% equities and 40% bonds declined by roughly 19%. Cash holders did not experience this direct capital volatility and retained immediate access to their funds throughout the downturn.

Maximum Portfolio Drops During a Market Downturn (2007-2009)

Illustration of how cash, a balanced portfolio and equities may behave during a significant market downturn. For illustrative purposes only.

This chart compares how much different financial setups dropped during the 2008 Global Financial Crisis. While a full stock portfolio fell sharply and a balanced portfolio experienced more moderate losses, cash maintained its nominal value. It highlights how a dedicated cash reserve can provide stability during periods of market stress.

Why Cash Levels Differ Between Individuals

There is no single cash balance that suits everyone.

The appropriate amount depends on financial goals, income stability, time horizon, upcoming expenses and personal comfort with risk.

Someone with stable income and few short-term financial commitments may have different liquidity needs from someone whose income fluctuates significantly or who expects major expenses in the near future.

Likewise, individuals approaching retirement or those who rely on their portfolio for ongoing income may choose to maintain a larger cash reserve to help manage periods of uncertainty.

For this reason, cash serves different purposes for different people. Its role is shaped as much by personal circumstances as it is by market conditions.

Bottom Line

Cash may not offer the same long-term growth potential as many investment assets, but it continues to serve an important role through liquidity, flexibility and financial resilience.

While inflation can reduce purchasing power over time, cash remains valuable because it provides immediate access to funds, helps manage unexpected expenses and offers stability during periods of market volatility.

Understanding both the benefits and limitations of cash can help people make more informed financial decisions and appreciate how different assets serve different purposes within a broader financial plan.

FAQs

Why is cash important in a portfolio?

Cash provides liquidity, flexibility and stability. It can help cover unexpected expenses and reduce the need to sell investments during market downturns.

What does liquidity mean?

Liquidity refers to how quickly and easily an asset can be converted into cash without significantly affecting its value.

Does cash lose value over time?

Cash generally maintains its nominal value, but inflation can reduce its purchasing power over time if savings returns fail to keep pace with rising prices.

How much cash should someone keep?

There is no universal amount. Appropriate cash levels depend on personal circumstances, income stability, financial goals and upcoming expenses.

Is cash safer than investing?

Cash is generally less volatile than investments, but it typically offers lower long-term growth potential and may be affected by inflation.