Q1 2026: Global Market Update & Outlook

Markets shifted notably in Q1 2026 as investors grappled with rising energy prices, sector rotation, and growing uncertainty around the pace of global monetary easing.

The optimism that characterised the final months of 2025 began to fade as commodity markets surged and equity leadership rotated. Energy stocks emerged as the clear outperformer across global markets, while technology and consumer sectors lost momentum. At the same time, bond markets experienced renewed volatility as investors reassessed inflation risks and the timing of interest rate cuts.

In this article, we examine the macroeconomic backdrop across the US, Europe, and Asia/emerging markets, summarise Q1 cross-asset performance, and outline positioning for the months ahead.

Q1 2026: Macroeconomic Landscape

United States

The US economy entered 2026 with moderate momentum, but increasing uncertainty around the path of monetary policy. Consumer spending and a resilient labour market continued to support activity, although higher borrowing costs weighed on housing and corporate investment.

Inflation pressures persisted into Q1, particularly as energy prices rose sharply, complicating the Federal Reserve’s policy outlook. Policymakers maintained a cautious tone, emphasising a data-dependent approach as they balanced the risks of easing too early against slowing growth.

Europe

Economic conditions across the euro area remained subdued. Industrial production continued to face pressure from weak external demand and elevated energy costs, while services activity provided only limited support.

The European Central Bank maintained a cautious stance, balancing slower growth with inflation that remained above target in several economies. Fiscal consolidation across parts of the region further contributed to a restrained economic backdrop.

Asia & Emerging Markets

Across Asia and emerging markets, performance remained uneven. Japan benefited from stable domestic demand and continued corporate reform momentum, supporting moderate growth.

In contrast, China’s recovery remained fragile, with structural challenges in the property sector and cautious consumer sentiment weighing on activity. More broadly, emerging markets remained sensitive to global capital flows and commodity price movements.

Overall, the macro backdrop in Q1 reflected a global economy that remained positive but fragile, leaving markets increasingly sensitive to commodity shocks, policy signals, and inflation developments.

Equity Market Recap: Risk On, But Selectively

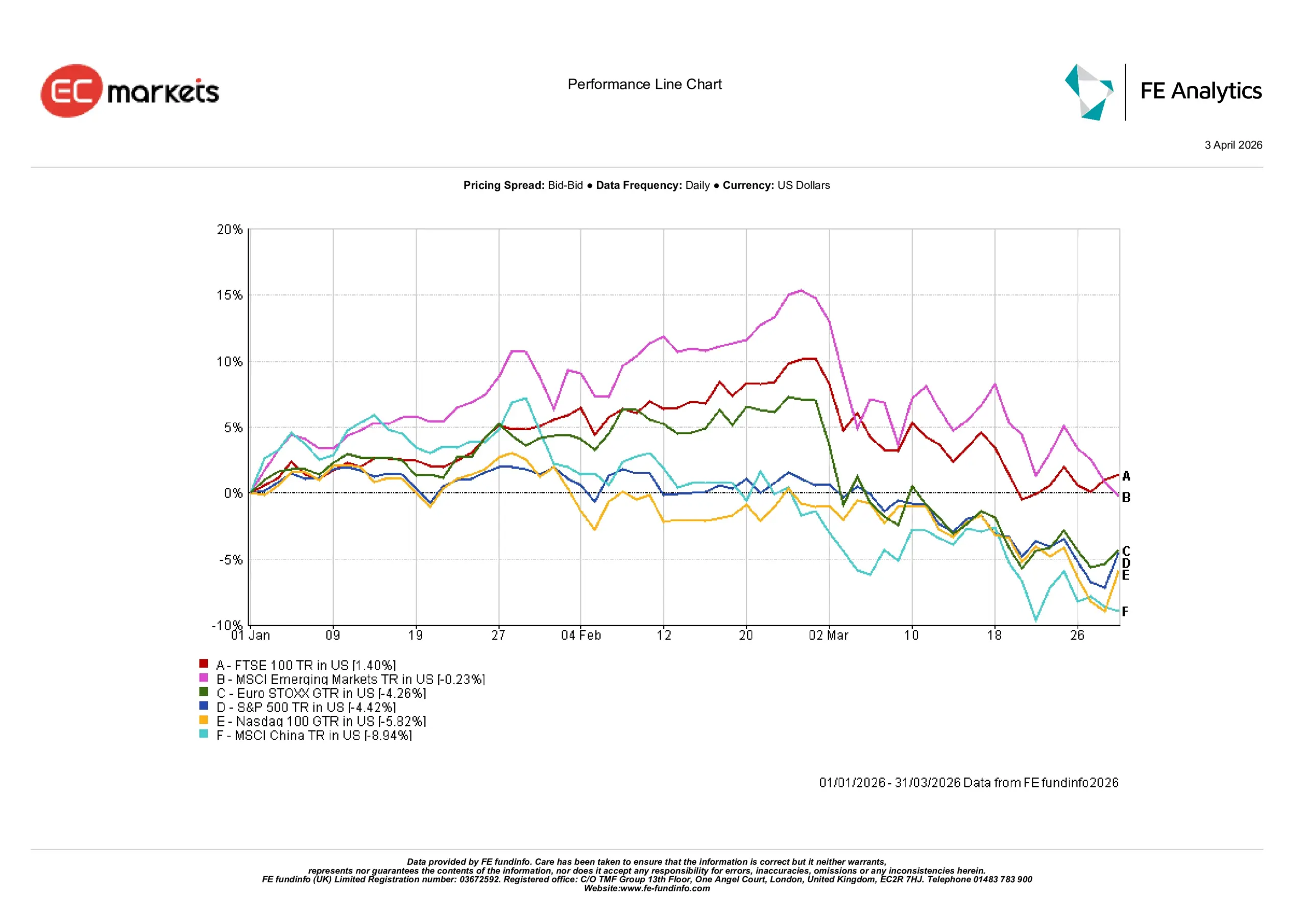

United States

US equities declined in Q1, with the S&P 500 falling 4.42% and the Nasdaq-100 down 5.82%. The move marked a reversal from the broad strength seen in late 2025.

Higher energy prices, persistent inflation concerns, and fading enthusiasm for high-valuation growth stocks weighed on sentiment. Technology, which had led the previous rally, lost momentum as investors rotated away from rate-sensitive sectors.

Europe

European equities also weakened, though performance diverged across markets. The Euro STOXX index fell 4.26% (USD terms), reflecting slower growth expectations and rising input costs.

The FTSE 100, however, gained 1.40%, supported by its heavier exposure to energy and commodity-linked companies, highlighting how sector composition drove returns during the quarter.

Asia & Emerging Markets

Performance across Asia and emerging markets was mixed. The MSCI Emerging Markets index declined marginally by 0.23%, but underlying dispersion was significant.

Chinese equities underperformed, with MSCI China falling 8.94%, as concerns around domestic demand and structural recovery persisted.The key takeaway: selectivity returned, and investors became less willing to reward weaker growth stories without stronger policy support.

Q1 2026 Index Performance

Sector Rotation and Key Market Themes

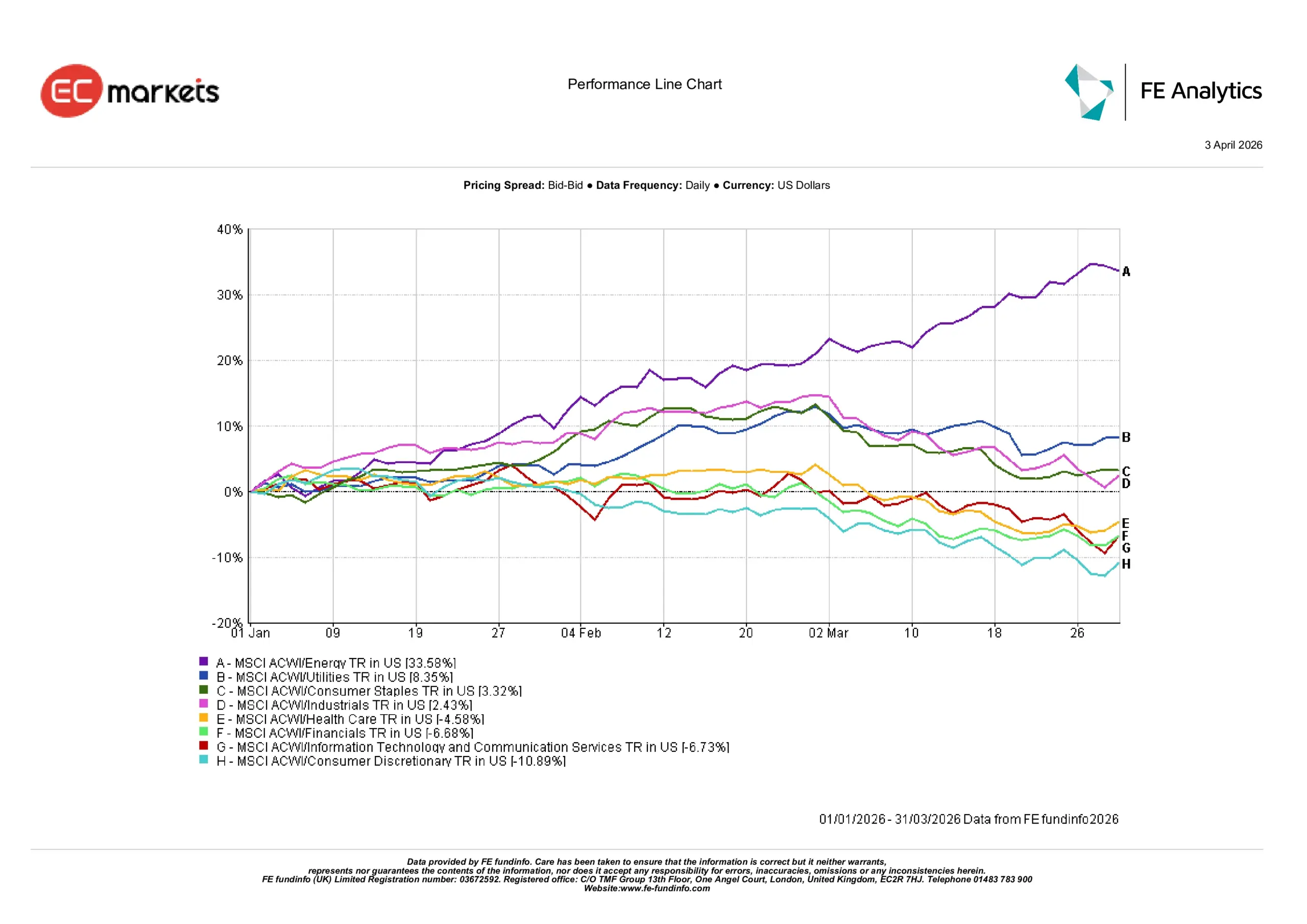

Energy Dominates

Sector leadership shifted decisively in Q1, with energy emerging as the standout performer. The sector surged 33.6% as oil prices rallied sharply amid supply concerns and geopolitical tensions.

Defensives Hold Up

Defensive sectors gained traction as volatility increased. Utilities rose 8.4%, while consumer staples gained 3.3%, supported by stable demand and pricing power. Industrials also posted moderate gains of 2.4%.

Growth and Cyclicals Under Pressure

Growth-oriented sectors struggled. Information technology and communication services fell 6.7%, while financials declined 6.7% amid bond market volatility. Healthcare slipped 4.6%, and consumer discretionary was the weakest performer, falling 10.9%.

Q1 2026 Sector Performance

Source: FE Analytics. All indices are total return in US dollars. Past performance is not a reliable indicator of future performance. Data as of 31 March 2026.

Fixed Income: Regaining Relevance

Bond markets regained relevance during Q1 after several quarters of limited diversification benefits.

US Treasuries experienced volatility as expectations for rapid rate cuts faded. European sovereign bonds followed a similar pattern, balancing weaker growth with persistent inflation.

Despite fluctuations, elevated yields began attracting investors seeking income and defensive positioning, re-establishing fixed income as a stabilising component in diversified portfolios.

Fixed Income Government Bond Returns

Source: Bloomberg, LSEG Datastream, J.P. Morgan Asset Management. All indices are Bloomberg benchmark government indices. Total returns are shown in local currency, except for global, which is in US dollars. Past performance is not a reliable indicator of future performance. Data as of 31 March 2026.

Commodities and Currencies: Energy Leads

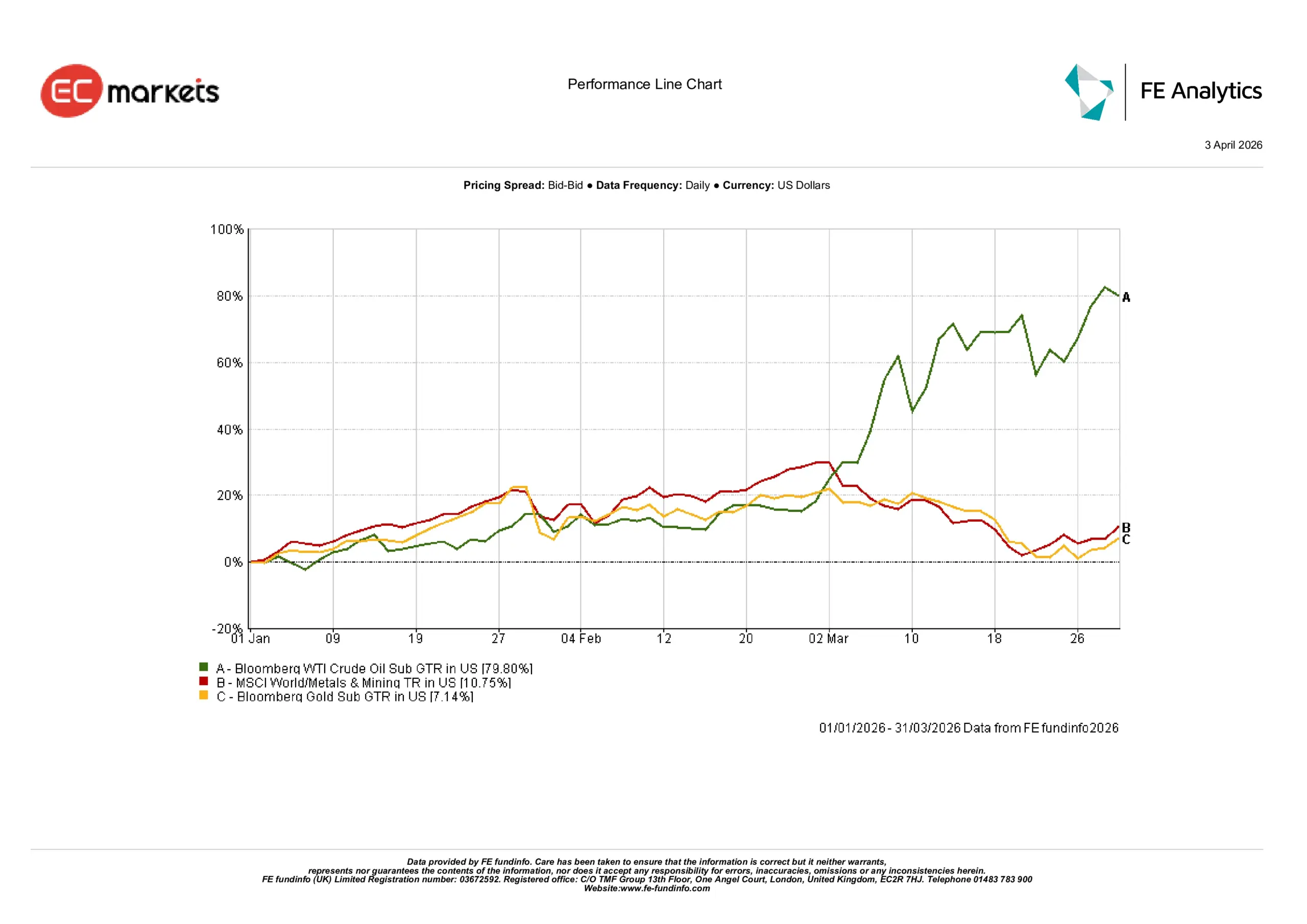

Oil Drives the Rally

Energy markets dominated Q1, with crude oil rising nearly 80%. Supply constraints, geopolitical tensions, and tightening inventories drove the surge, making oil the standout asset class of the quarter.

Gold Benefits from Uncertainty

Gold gained approximately 7%, supported by safe-haven demand and central bank buying. Industrial metals also advanced, with the MSCI World Metals & Mining Index rising around 10.7%.

Q1 2026 Commodity Performance

Source: FE Analytics. All indices are total return in US dollars. Past performance is not a reliable indicator of future performance. Data as of 31 March 2026.

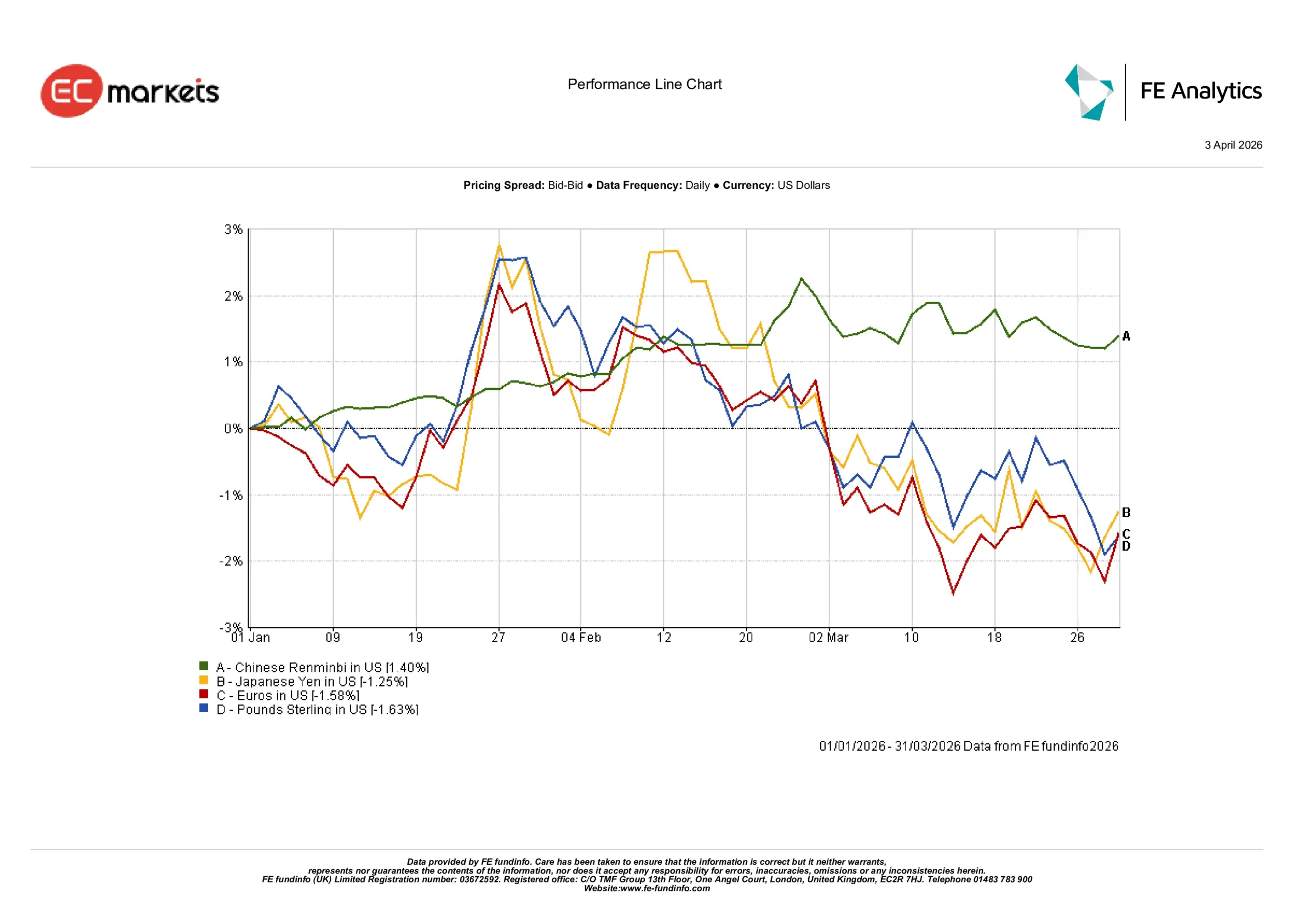

FX: Modest but Divergent

Currency moves were relatively contained but showed divergence. The Chinese renminbi strengthened 1.4%, while developed market currencies weakened slightly against the US dollar:

- Euro: -1.6%

- Sterling: -1.6%

- Yen: -1.3%

Interest rate differentials and carry trade dynamics continued to support a broadly stronger US dollar.

Q1 2026 Currency Dynamics

Q1 2026: Outlook and Positioning

Looking ahead, markets are likely to remain highly sensitive to inflation trends, commodity prices, and central bank policy.

The sharp rise in energy prices has introduced renewed uncertainty around the timing of monetary easing, particularly in the US and Europe. While global growth remains positive, signs of moderation suggest policymakers will maintain a cautious, data-driven approach.

For investors, the environment increasingly demands selectivity.

- Commodity-linked sectors may continue to outperform if inflation persists

- Companies with strong pricing power remain well-positioned

- Defensive sectors may benefit if volatility increases

- Fixed income is regaining importance due to attractive yields

Maintaining diversified exposure across asset classes will be critical as macro conditions evolve.

Conclusion

Q1 2026 marked a clear shift in market dynamics.

Rising energy prices, sector rotation, and evolving policy expectations reshaped investor sentiment. Equity markets declined modestly across regions, while leadership rotated toward energy and defensive sectors.

Commodities, particularly oil, were the primary driver of returns, while currency movements remained relatively contained.

The broader takeaway is clear: markets have transitioned from broad-based momentum to a more selective environment. As inflation, commodities, and policy continue to drive direction, disciplined positioning and diversification will remain key themes for the remainder of 2026.

FAQs: Q1 2026 Market Trends

1. Why did energy stocks outperform in Q1 2026?

Energy stocks led global markets due to a sharp rise in oil prices, driven by supply constraints, geopolitical tensions, and tightening global inventories. This directly boosted revenues and margins for energy producers.

2. Why did technology stocks decline in Q1 2026?

Technology stocks came under pressure as investors rotated away from high-valuation, rate-sensitive sectors. Persistent inflation and higher interest rate expectations reduced the appeal of future earnings-driven growth stocks.

3. What caused volatility in bond markets during Q1 2026?

Bond market volatility was driven by changing expectations around inflation and the timing of central bank rate cuts. Rising energy prices reinforced inflation concerns, delaying expectations for monetary easing.

4. Why is oil considered a key driver of markets in 2026?

Oil has become a central market driver because of its impact on inflation, corporate costs, and consumer spending. Sharp price increases influence central bank policy decisions and sector performance across equities.

5. Are defensive sectors expected to continue outperforming?

Defensive sectors such as utilities and consumer staples may continue to perform well if market volatility persists. Their stable earnings and pricing power make them attractive during uncertain macroeconomic conditions.

6. How should investors position in the current market environment?

The current environment favours selective positioning. Investors are focusing on commodity-linked sectors, companies with strong pricing power, defensive assets, and diversified exposure across asset classes.