Headline Inflation Is Down. The Hard Part Starts Now

Headline inflation has cooled, but the last mile rarely runs in a straight line. US CPI slowed to 2.4% y/y in January 2026, down from 2.7% in December 2025; core CPI eased to 2.5% from 2.6%. These gains remain above target because the parts now doing the heavy lifting move slowly.

The next phase is less about goods and more about services, wages, and supply frictions, which means prices tend to drift lower in steps rather than drop quickly.

Services Inflation

Services behave differently from goods because they are driven by people, premises, and contracts. “Services less energy services” is running near 3% y/y, and shelter sits a little above that.

They are stubborn because rents and imputed shelter reset when leases roll, health care and insurance follow multiyear contracts, and transport and education are labour intensive and often capacity constrained.

As a result, service prices adjust gradually, which slows the last leg of disinflation even after goods prices normalise. Because services make up a larger share of the CPI basket than goods, this slow adjustment has an outsized impact on the overall inflation path.

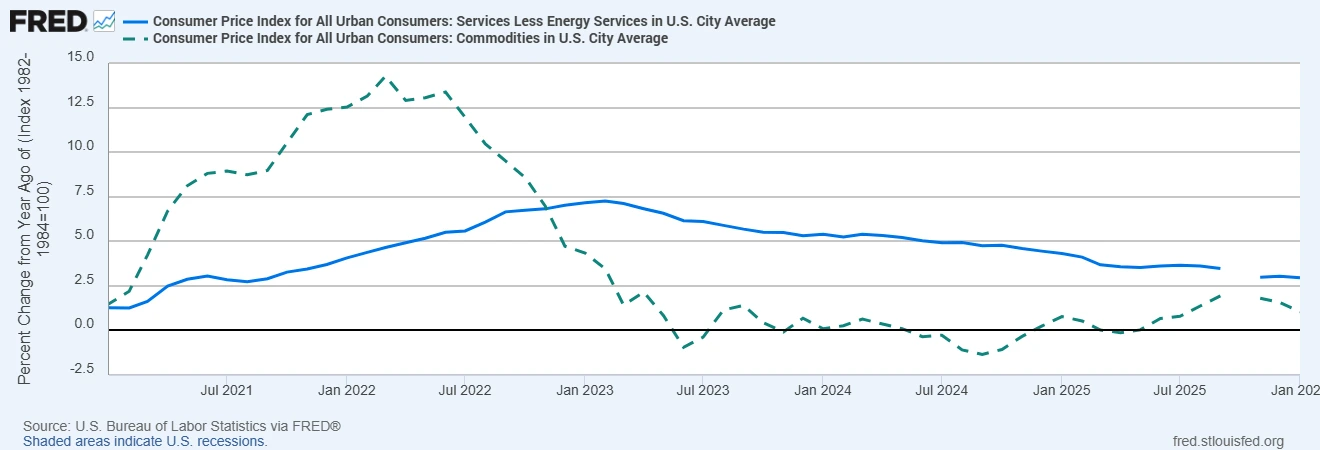

This dynamic is clear in the data, where services inflation remains significantly firmer than goods inflation.

Core Services Inflation Has Stayed Firm as Goods Inflation Has Fallen

Wage Growth

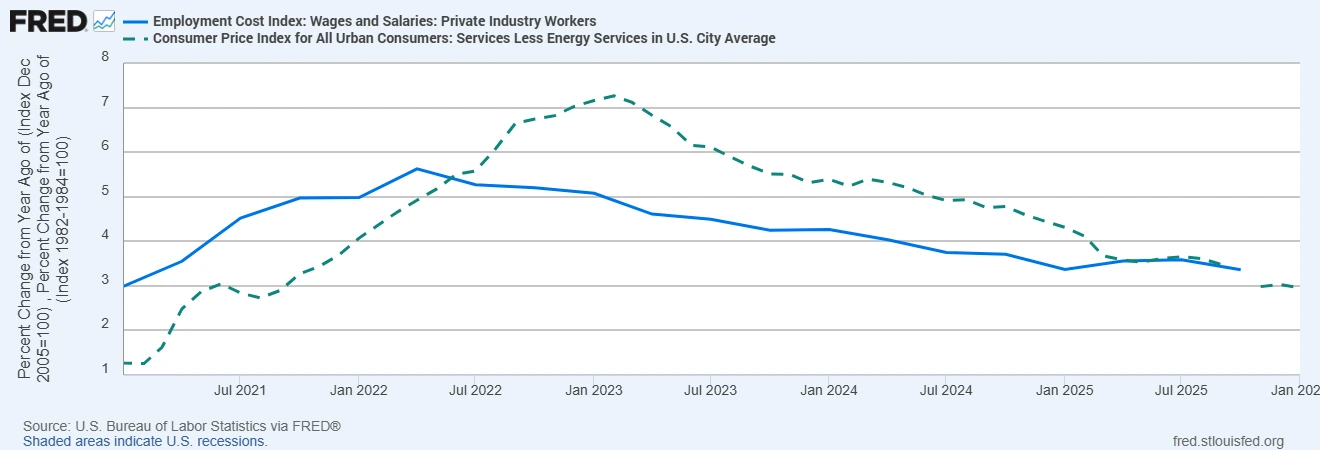

Wages sit at the centre of services prices because labour is the main input cost. The Employment Cost Index shows wages and salaries a little above 3% y/y and pay for job stayers remains firmer.

Wage growth typically lags labour‑market cooling because firms hoard labour after difficult hiring cycles, minimum wage changes lift the floor, and skills gaps keep pressure on specific roles. Therefore, wage disinflation takes time, which keeps core services inflation elevated even as headline CPI softens.

This is why wage dynamics often determine how quickly or slowly central banks can cut rates.

Wage Growth Is Keeping Core Services Inflation Elevated

Supply Side Constraints

Supply chains are healthier than during the pandemic, but structural frictions remain.

Energy costs are sensitive to geopolitics and under investment, which keeps a floor under transport and production costs.

Shipping lanes can be disrupted by regional conflict or climate events, and reshoring or diversification adds transitional costs.

These pressures do not guarantee higher inflation, but they limit how far and how fast prices can fall in energy‑linked and logistics‑linked categories, which helps explain why underlying gauges remain above target.

What Markets Are Missing

Markets often assume that once headline CPI rolls over, inflation will glide to target. Policymakers are more cautious because services and wages adjust slowly.

With core services still firm and wage growth easing only gradually, inflation may settle near 2.5% to 3.0% for a period rather than return quickly to 2.0%. Consumer inflation expectations remain somewhat elevated, which influences price setting and pay negotiations, and therefore slows the return to target.

This mix argues for a measured pace of rate cuts and a higher bar for declaring victory. Because services and wages move slowly, markets may underestimate how long it takes for inflation to return fully to target.

Implications for FX and Global Assets

In FX, currencies supported by positive real rates can remain resilient because slower disinflation implies slower or later rate cuts. That favours selective carry trades, but it also increases sensitivity to wage and services data that can shift paths quickly.

In equities, sticky services inflation widens sector dispersion because companies with pricing power and lower wage intensity can absorb costs more easily, while labour‑intensive or rate‑sensitive businesses face more pressure if cuts are delayed.

In fixed income, the risk is to duration because slower cuts push up term premiums and discount rates, which weighs on long‑duration assets.

Conclusion

The next inflation cycle is shaped by services, wages, and supply frictions because these drivers move slowly and anchor the pace of disinflation. To track the path, focus on core services and shelter trends near 3% y/y, wage metrics a bit above 3% y/y, and underlying measures such as core PCE close to 3% y/y.

The direction is down, but the journey is uneven. Positioning that respects these stickier parts of inflation, and the possibility that policy stays restrictive for longer, is better aligned with the evidence than a straight-line disinflation story.

The message is simple: disinflation continues, but at a pace driven by the slow-moving components of the economy.