Government Debt and Its Impact on the Market

When it comes to macro-indicators these days, all eyes are on Government debt. After the 2008 financial crisis, the Covid-19 pandemic, and a period of elevated fiscal spending, many economies are now carrying much more public debt than they did a decade ago.

Government borrowing can support economic stability and growth, particularly during downturns. But investors also pay close attention to what rising debt means for bond supply, interest rates, currencies, and overall confidence in a country’s policy direction.

What is Government Debt?

Government debt builds up when public spending exceeds tax revenue over time. To finance that gap, governments issue bonds such as U.S. Treasury bills, notes and bonds, or UK gilts. Investors including pension funds, asset managers, and central banks purchase these bonds and receive interest in return.

Debt is often assessed using the debt‑to‑GDP ratio, which compares total public debt with the size of the economy. That said, the question isn’t whether debt is simply “high” or “low”, but whether it actually seems manageable when considering the economic output that supports it.

Government Debt is On the Rise

The International Monetary Fund (IMF) estimates that public debt rose to around 93% of global GDP in 2023 – roughly nine percentage points above pre-pandemic levels.

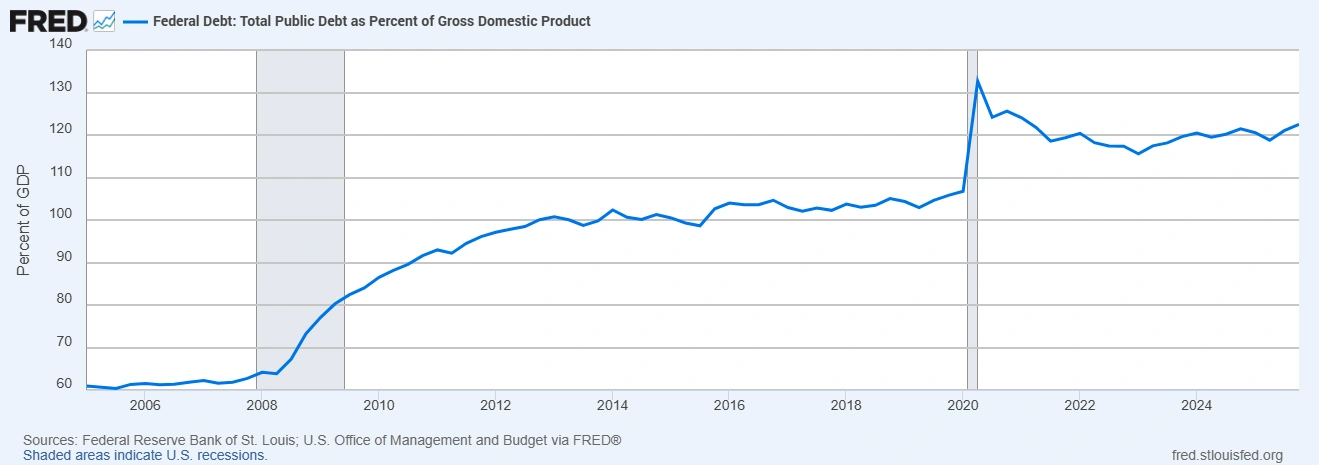

US Federal Debt as a Percentage of GDP

Sources: Federal Reserve Bank of St. Louis; U.S. Office of Management and Budget via FRED®

In the US, TreasuryDirect data shows that total public debt stands at around $39.0 trillion, as of 19 March 2026. Japan’s debt, meanwhile, remains among the highest in the world, with the gross debt‑to‑GDP ratio around 250% in recent years, according to Japan’s Ministry of Finance.

High debt levels alone don’t automatically trigger a crisis, however. Markets tend to pay closer attention when borrowing rises faster than economic growth, or when the policy plan for stabilising debt appears uncertain.

Why Government Debt Levels Push Yields Higher

When governments borrow more, they typically issue more bonds. If investor demand does not rise in step with supply, yields may need to increase to attract buyers.

We’ve seem this dynamic appear more often in recent years. The OECD estimates governments and companies will borrow around $29 trillion from global bond markets in 2026, up roughly 17% from 2024 levels. Central government borrowing across OECD economies alone is projected to reach about $18 trillion in 2026.

Long-term bond yields reflect expectations for future policy rates and the additional compensation investors demand for holding longer maturities (known as the term premium). When issuance is heavy or fiscal risks intensify, this premium can rise, keeping long-dated yields elevated even if central banks aren’t tightening policy.

What’s the Impact of Higher Debt and Yields?

Higher government borrowing can influence several financial markets:

Bond markets

Larger issuance and rising fiscal uncertainty can push yields higher and increase volatility. Because government yields act as a benchmark for the wider economy, rising sovereign yields often translate into higher borrowing costs for households and businesses.

Equity markets

Higher yields raise discount rates, reducing the present value of future earnings. This can weigh on equity valuations, especially when yields move sharply or when growth sensitivity is high.

Currency markets

FX responses can be mixed. Higher yields may attract capital inflows and support a currency in the short term. But if investors question fiscal sustainability, confidence may weaken and the currency may decline.

A clear example came in the UK in September 2022, when fiscal plans implying much higher borrowing coincided with a sharp rise in gilt yields and sterling briefly falling to multi‑decade lows.

When High Debt Matters Less

Context matters. Investors look at whether debt is:

- Issued in the country’s own currency

- Spread across long maturities

- Supported by credible institutions

- Backed by a solid economic outlook

Countries borrowing mainly in domestic currency tend to be less exposed to sudden currency‑mismatch risks. Another critical factor is the relationship between interest rates and economic growth: when borrowing costs rise faster than growth, it’s more difficult to stabilise debt. This is why markets react more sharply when rising debt coincides with a higher‑rate environment.

Bottom Line

Government debt levels matter because they shape bond supply, influence investor confidence and ultimately affect interest rates across the economy. Higher yields can raise borrowing costs, pressure equity valuations, and influence currency movements.

Debt doesn’t need to reach extreme levels to affect markets. Instead, investors focus on the direction of travel – whether debt is rising faster than economic growth and whether policymakers have a credible plan to keep it sustainable over time.