Dollar Strength and Yield Pressures Drive Global Risk Repricing | Weekly Recap: 23-27 March 2026

Economic Overview

Markets entered the week navigating a shift in focus away from the immediate energy shock narrative toward the broader implications of persistently tight financial conditions. While geopolitical tensions continued to support elevated oil prices, investor attention increasingly turned to the interaction between inflation expectations, sovereign yields and the pace at which central banks could eventually move toward policy easing.

The macro sequence remained familiar. The cause was a continued repricing of inflation risk through commodities and bond markets. The effect was tighter global financial conditions as higher yields forced investors to reassess equity valuations and risk exposure.

Central bank messaging remained cautious. Policymakers continued to emphasise that while policy tightening may have paused, the threshold for easing remains high. The Fed maintained its data-dependent stance, reinforcing the view that inflation must show clearer signs of moderation before policy support can return. Similar messaging came from the BoE and ECB, where policymakers reiterated that energy costs and wage dynamics remain key upside risks to inflation.

In Asia, the BoJ continued balancing imported inflation pressures with the need to maintain domestic financial stability. The overall policy message across major economies was consistent: inflation risks have not disappeared, and monetary authorities remain reluctant to signal imminent easing.

Equities, Bonds and Commodities

Equities reflected the tightening financial backdrop. Global risk assets struggled as higher sovereign yields and a stronger US dollar weighed on investor sentiment.

US equity markets declined during the week. The S&P 500 and Nasdaq both moved lower as rising yields reduced support for growth-oriented sectors, while the Dow Jones Industrial Average also slipped as investors rotated away from cyclical exposure. The repricing of inflation expectations through bond markets pushed discount rates higher, placing renewed pressure on equity valuations.

European equities experienced broader weakness. The STOXX Europe 600 and Germany’s DAX declined as investors reassessed growth prospects amid tighter financial conditions. The FTSE 100 also fell as energy-driven inflation concerns continued to influence expectations for BoE policy.

Bond markets absorbed the shift through rising yields. The US 10-year Treasury yield remained elevated near the upper end of recent ranges, while the 2-year yield reflected reduced expectations for near-term policy easing. In Europe, German 10-year Bund yields and UK gilt yields also remained firm as investors rebuilt inflation risk premia.

Commodities remained an important transmission channel. Oil prices stayed elevated amid ongoing geopolitical concerns and supply uncertainty. Gold, however, moved lower during the week as rising real yields and a stronger dollar reduced the appeal of non-yielding assets.

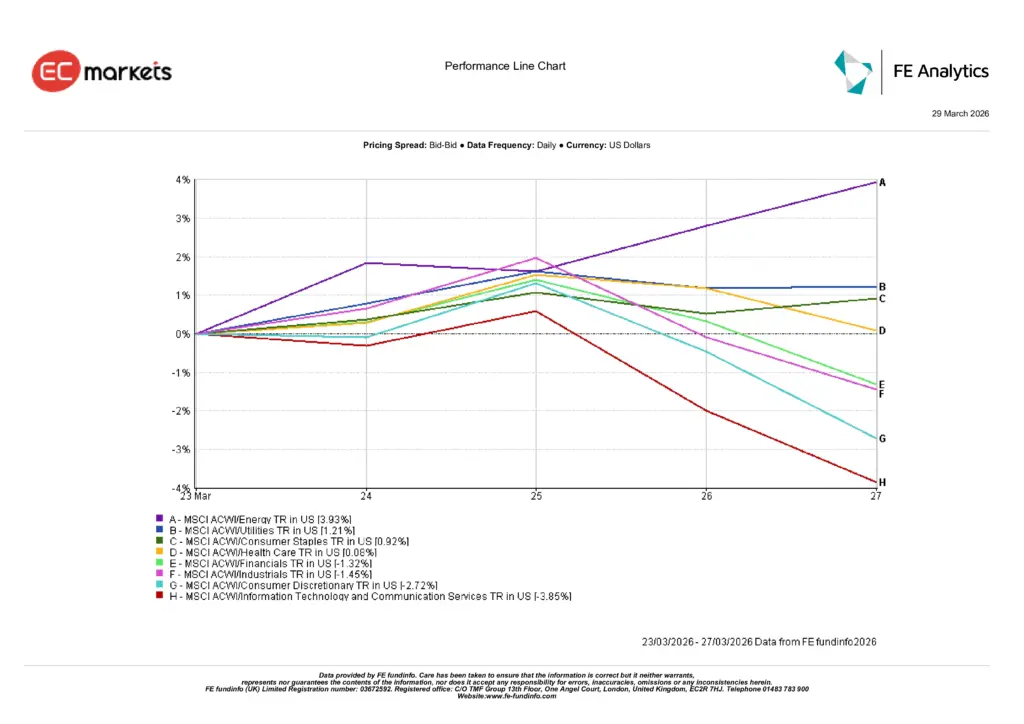

Sector Performance

Sector performance reflected clear investor positioning around the inflation narrative.

Energy was the standout performer, with the MSCI ACWI Energy sector rising roughly 3.9% during the week as higher oil prices strengthened earnings expectations for producers. The cause was continued strength in crude prices. The effect was investor rotation toward sectors with direct commodity exposure.

Utilities also posted solid gains of around 1.2%, benefiting from their defensive characteristics and stable cash-flow profiles. Consumer Staples edged higher by approximately 0.9%, reflecting selective demand for defensive exposure.

Elsewhere, sector performance showed broader weakness. Financials declined roughly 1.3%, while Industrials fell around 1.5% as concerns over global growth and input costs weighed on sentiment.

The weakest performance came from rate-sensitive sectors. Consumer Discretionary dropped about 2.7%, reflecting concerns that higher energy prices could pressure household spending. Information Technology and Communication Services experienced the steepest decline, falling approximately 3.9% as rising yields continued to weigh on long-duration growth valuations.

The overall message remained consistent with previous weeks: in an environment shaped by inflation risk and higher yields, investors have favoured commodity exposure while reducing exposure to growth and cyclical sectors.

Sector Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 27 March 2026.

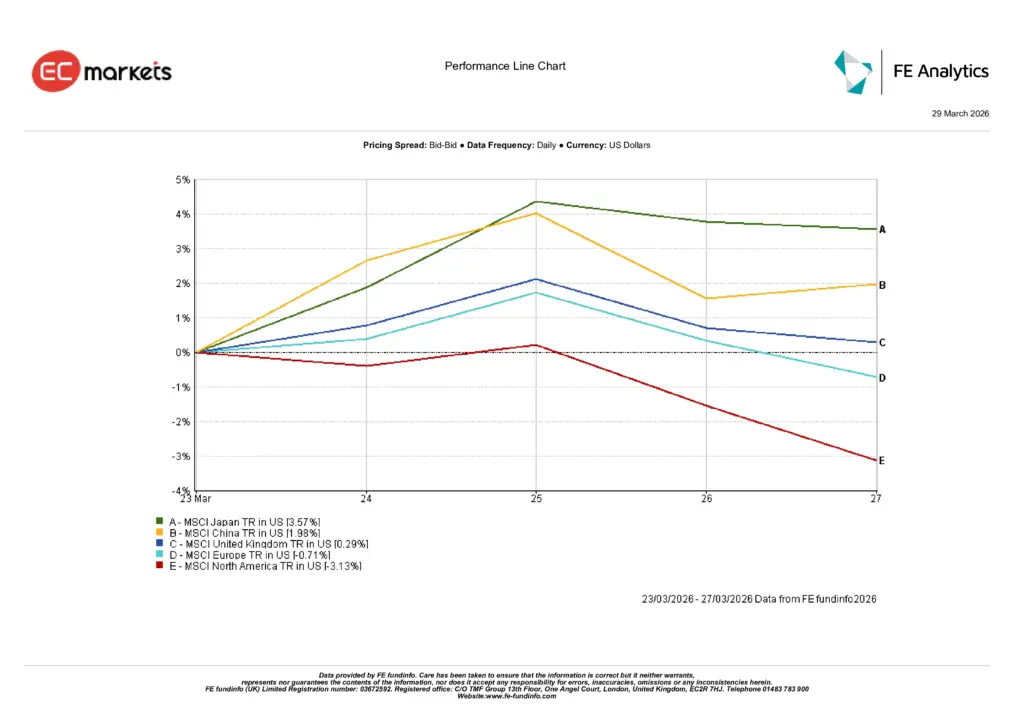

Regional Markets

Regional equity performance showed meaningful divergence across global markets.

North America experienced the sharpest decline, with MSCI North America falling around 3.1% during the week. The move largely reflected weakness across major US indices as rising yields and tighter financial conditions pressured valuations.

Europe also declined, with MSCI Europe falling roughly 0.7%. The region’s sensitivity to imported energy costs and continued uncertainty around growth dynamics weighed on sentiment.

The United Kingdom proved relatively resilient. MSCI UK rose about 0.3%, supported in part by the FTSE’s heavier exposure to energy and defensive sectors.

Asia delivered the strongest performance. MSCI Japan gained approximately 3.6%, benefiting from currency dynamics and renewed investor interest in export-oriented companies. MSCI China rose about 2.0%, supported by expectations of additional policy support and improving domestic sentiment.

The regional pattern suggested that markets less exposed to the immediate impact of rising yields and energy costs experienced comparatively stronger performance.

Regional Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 27 March 2026.

Currency Markets

Currency markets reflected the tightening global financial backdrop and renewed dollar strength.

EUR/USD weakened across the week, falling from around 1.1613 on Monday to roughly 1.1510 by Friday. The move reflected persistent interest-rate differentials favouring the United States as well as cautious sentiment across European markets.

Sterling followed a similar path. GBP/USD declined from approximately 1.3430 to around 1.3260, highlighting the influence of dollar strength and the market’s reassessment of UK monetary policy expectations.

The yen weakened as yield differentials continued to dominate safe-haven flows. USD/JPY rose from roughly 158.4 to around 160.3, reflecting continued divergence between US yields and Japan’s accommodative policy stance.

Cross-rates reinforced the broader pattern. GBP/JPY traded mostly sideways, ending the week near 212.6 after modest volatility, as sterling weakness against the dollar was offset by continued softness in the yen.

Overall, FX markets reflected a consistent macro theme: higher yields and persistent inflation uncertainty continued to favour the US dollar.

Outlook and The Week Ahead

Markets now face a familiar macro dilemma. Inflation risks remain present, but the persistence of higher yields and tighter financial conditions is beginning to influence investor positioning across asset classes.

If oil prices stabilise and inflation expectations moderate, sovereign yields could gradually ease and provide support for equity markets. In that scenario, investors may begin rebuilding risk exposure, particularly in sectors that have recently underperformed.

However, if geopolitical tensions continue to support elevated energy prices, markets may continue to price a higher inflation baseline. The cause would be sustained commodity pressure. The effect would be continued caution from central banks and delayed expectations for policy easing.

For investors, the key variables remain inflation data, wage dynamics and bond market behaviour. These indicators will determine whether the current tightening in financial conditions proves temporary or becomes a more persistent feature of the macro environment.