Though Out of the Spotlight, Real Interest Rates Still Matter

Real interest rates rarely grab the headlines as much as nominal rates do. Investors often only hear about the level of central bank policy rates or the yield on government bonds such as the 10-year US Treasury.

However, in financial markets, it’s often the real interest rate that matters more.

Real interest rates adjust nominal rates for inflation, showing the return investors actually receive after accounting for rising prices. In simple terms, they measure how much purchasing power an investment truly delivers. For example, if a government bond yields 4% while inflation is running at 3%, the real return is only about 1%. Even though the nominal yield appears relatively high, the investor’s true gain after inflation is much smaller.

Understanding this distinction is important because many financial assets respond more directly to changes in real interest rates than to nominal ones.

Nominal vs. Real Interest Rates

A nominal interest rate is the stated return on an investment. This could be the yield on a government bond or the policy rate set by a central bank. Nominal rates do not account for inflation.

A real interest rate, on the other hand, adjusts for inflation and therefore reflects the real increase in purchasing power. The relationship is relatively simple. Real interest rates are approximately equal to nominal rates minus inflation.

For instance, if a bond offers a nominal yield of 5% while inflation is 2%, the real return is roughly 3%. But if inflation rises to 4%, the real return falls to around 1%, even though the nominal rate has not changed.

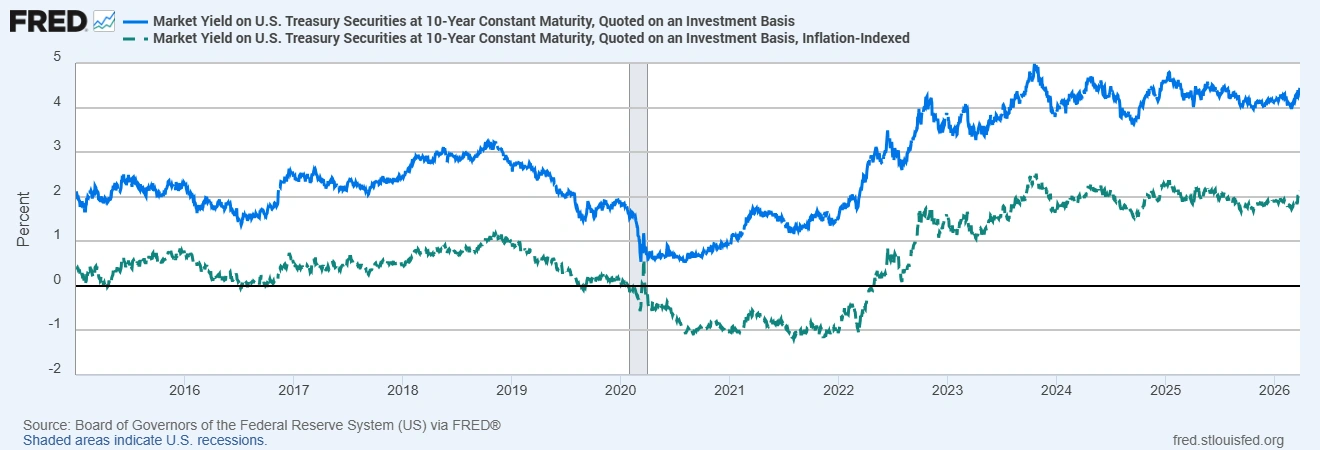

Nominal vs. Real 10‑Year US Treasury Yields

In early 2026, the nominal 10-year US Treasury yield has been around 4.3%-4.4%, while the 10-year Treasury Inflation-Protected Securities (TIPS) yield, which reflects the real yield, has been closer to about 2.0%. Despite the relatively high headline yield, the inflation-adjusted return available to investors has been far smaller.

Why Real Interest Rates Drive Markets

Real interest rates play a central role in determining how attractive different assets appear to investors.

When real yields rise, safe assets such as government bonds become more appealing because they offer a higher inflation-adjusted return. This can draw investment away from equities, commodities and other risk assets.

In contrast, when real yields are low or even negative, investors often search for alternatives that can preserve purchasing power.

Central banks and policymakers also pay close attention to real interest rates when assessing the stance of monetary policy. Even if a central bank keeps its nominal policy rate unchanged, falling inflation expectations can push real rates higher. This effectively tightens financial conditions and can slow economic activity.

Impact on Equities, Bonds, Gold, and Currencies

Changes in real interest rates can influence multiple financial markets.

In equity markets, higher real yields increase the discount rate used to value future corporate earnings. When discount rates rise, the present value of those earnings declines, which can put pressure on stock valuations.

In the bond market, real rates determine the inflation-adjusted return on fixed income investments. Rising real yields typically mean falling bond prices, which can also push borrowing costs higher across the economy.

Gold is particularly sensitive to real interest rates. Because gold does not generate income, its attractiveness depends partly on the opportunity cost of holding it. When real yields rise, investors can earn higher returns from bonds, which tends to reduce demand for gold. Conversely, when real yields fall or turn negative, gold often becomes more appealing as a store of value.

Currency markets can also react to changes in real yields. A country offering relatively higher real returns may attract international capital flows, which can support its currency. If real yields fall relative to other economies, the currency may weaken as investors look elsewhere for better inflation-adjusted returns.

Inflation Expectations and Real Yields

Real interest rates are closely linked to inflation expectations. If investors expect inflation to decline, nominal bond yields may fall less than expected, causing real yields to rise.

This dynamic has been visible in recent years. Between 2021 and 2023, inflation surged in many economies, pushing real yields deep into negative territory because bond yields lagged the rise in prices. As inflation gradually cooled in the following years, real yields began to recover.

Because of this relationship, investors often monitor indicators such as 10-year TIPS yields and breakeven inflation rates to gauge how markets are pricing inflation and future monetary policy.

Bottom Line

Nominal interest rates often attract the most attention, but real interest rates provide a clearer measure of the true return investors receive after inflation.

Movements in real yields can influence bond prices, equity valuations, currency flows and commodity demand. When real rates rise, financial conditions tend to tighten. When they fall, investors often shift toward assets that offer protection against inflation.

For this reason, many market participants closely watch indicators such as the 10-year TIPS yield when assessing the broader economic and investment environment.