Quality Leads While Geopolitics Sets the Oil Premium | Weekly Recap: 23-27 February 2026

Economic Overview

Markets again asked investors to separate what moves prices from what merely makes headlines. In the US, the policy path stayed “restrictive but stable,” and that was enough to let styles do the heavy lifting: quality growth still drew a bid, but not at the expense of breadth.

Across Europe and the UK, earnings and calm central‑bank communication kept volatility contained and allowed Energy‑ and cash‑flow‑anchored names to participate.

China remained the drag in a week that still struggled to convert policy signals into durable risk appetite, while Japan extended leadership as currency dynamics and corporate delivery continued to reinforce one another.

Geopolitics moved from watchlist to risk‑premium: the Israel–Iran escalation restored a measured oil premium as traders focused on shipping lanes and infrastructure risk—especially around the Strait of Hormuz, without (yet) pricing a confirmed supply shock.

Equities, Bonds & Commodities

Equities advanced selectively rather than in a straight line. The US stayed constructive, Europe and the UK participated with a tilt toward cash‑generative and Energy‑linked exposures, Japan led, and China lagged.

Rates helped more than they hurt: the US 10‑year yield slipped to ~3.97% by Friday, its lowest in four months; Germany’s 10‑year Bund eased to ~2.69%; UK 10‑year Gilts hovered a little above 4.2-4.3% into week‑end.

The shape of the moves mattered more than the magnitude: slightly easier duration supported quality and defensives without derailing cyclicals. Energy held a geopolitical bid, while gold kept its place as a measured hedge rather than a panic trade.

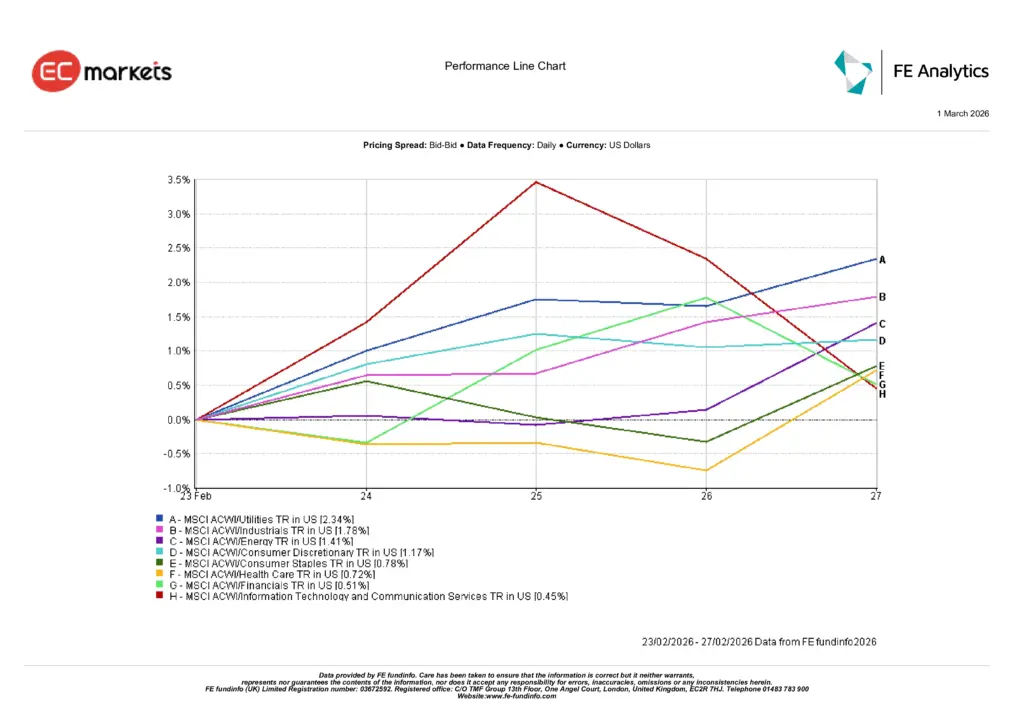

Sector Performance

The week rewarded participation with a quality bias. Utilities (+2.34%) led as investors looked for steady cash flows while keeping risk on the field. Industrials (+1.78%) followed, helped by a firmer activity tone and solid order backlogs, and Energy (+1.41%) benefited from a modest geopolitical premium in oil. Consumer Discretionary (+1.17%), Consumer Staples (+0.78%), Health Care (+0.72%) and Financials (+0.51%) added consistent, if quieter, gains that broadened the advance. Information Technology & Communication Services (+0.45%) finished positive but ceded leadership, which fits a market that is paying for dependable earnings delivery over longer‑dated growth stories.

Taken together, the pattern says the same thing as last week: quality remains the anchor, and cyclical exposure works best where cash‑generation is visible.

Sector Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 27 February 2026.

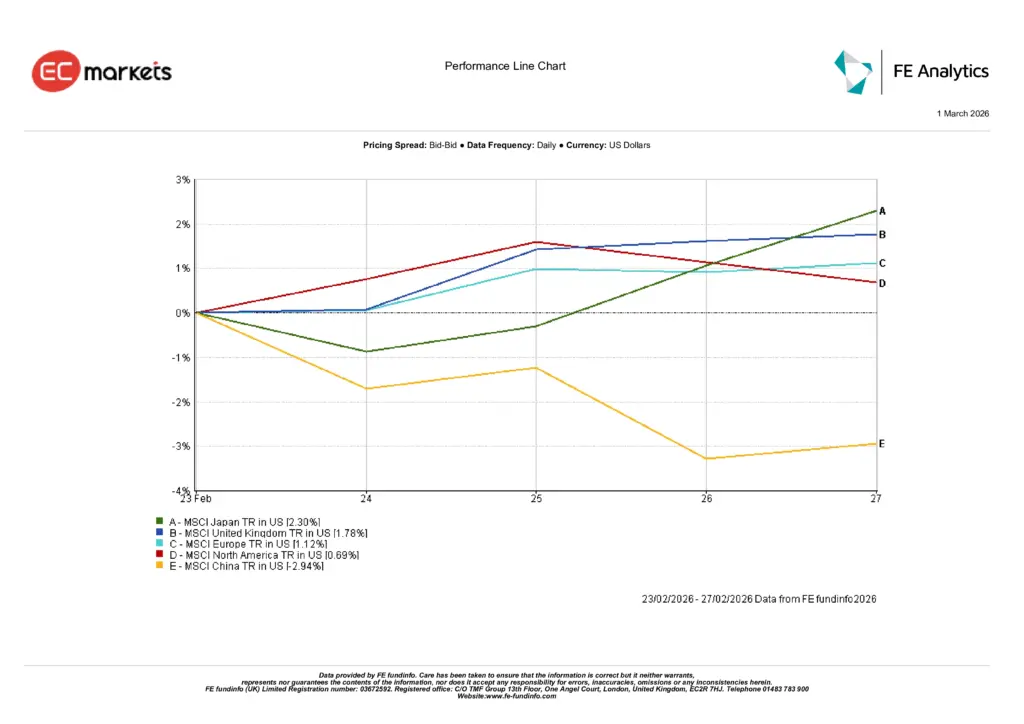

Regional Markets

The week’s regional pattern was straightforward and consistent with the broader rotation. Japan (+2.30%) led as currency support and solid corporate delivery kept buyers engaged. United Kingdom (+1.78%) and Europe ex‑UK (+1.12%) followed, helped by Energy’s bid and steady policy communication that allowed cyclicals to participate. North America (+0.69%) moved higher in line with the quality‑tilted style leadership. China (-2.94%) lagged as confidence in the policy‑to‑growth hand‑off remained tentative.

The takeaway isn’t just the scoreboard; it’s the message it sends: investors are paying up where earnings guidance is credible and policy signals are consistent, and discounting markets where clarity is still developing.

Regional Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 27 February 2026.

Currency Markets

FX moved with rate spreads and the week’s equity leadership rather than on idiosyncratic shocks.

The dollar firmed against the yen as yield differentials stayed in play, leaving USD/JPY higher on the week and reinforcing Japan’s exporter‑friendly backdrop (USD/JPY ~154.6 → ~156.1 across last week). Sterling was broadly flat versus the dollar as UK data and BoE messaging did little to shift expectations (GBP/USD hovered ~1.35), while the euro edged up against the dollar into Friday, consistent with steady euro‑area prints and calmer policy communication (ECB reference ~1.178-1.181 over the period). Crosses told the same story: GBP/JPY moved higher alongside the wider yen weakness, echoing the week’s risk tone and Japan’s leadership in equities.

Outlook & The Week Ahead

The next step depends on whether risk premium stays premium or becomes pipeline. If the Israel-Iran backdrop remains a headline premium without confirmed disruption, Energy can hold leadership alongside quality cyclicals and defensives; a verified hit to shipping or infrastructure would push inflation risk back into the rates debate and re‑energise defensives.

On policy, watch the incoming US and European prints for any surprise that would push the long end back above recent ranges; absent that, the market should continue to reward cash‑flow visibility in growth and operational leverage in cyclicals.

Practically, the message is unchanged: stay patient, stay quality‑focused, upgrade on pullbacks, and size cyclical exposure to the clarity you actually have.