Energy Costs Push Inflation Higher as Bond Markets Brace for Fed | Weekly Recap: 8 - 12 June 2026

Markets spent the second week of June navigating a more challenging environment as rising energy prices, persistent inflation pressures and elevated bond yields complicated the outlook for monetary policy. While economic growth remained broadly resilient, investors became increasingly focused on whether inflation could remain higher for longer, particularly as geopolitical tensions in the Middle East continued supporting energy prices. As a result, bond markets, currencies and sector performance were largely driven by shifting interest-rate expectations rather than growth optimism alone.

Economic Overview

Markets spent the second week of June confronting renewed inflation concerns as rising energy prices and persistent pricing pressures challenged expectations that the disinflation process would continue smoothly. Investors entered the week hoping for a relatively stable macro backdrop, but incoming data reinforced the view that inflation risks remain present and that central banks may need to maintain restrictive policy settings for longer.

The main focus came from the US, where May consumer price data highlighted renewed upward pressure on headline inflation. Energy costs rose sharply during the month, contributing to a higher inflation reading and reinforcing concerns that previous progress on price stability could prove uneven. The data followed the previous week’s stronger-than-expected payrolls report and further reduced expectations of near-term Fed easing. Markets increasingly shifted towards a higher-for-longer policy outlook, supporting bond yields and encouraging a more selective approach to risk assets.

Outside the US, economic momentum remained relatively subdued. Activity indicators across Europe pointed to only modest growth, while ECB officials continued to stress the need for caution despite the gradual easing cycle already underway. In the UK, weak growth conditions and political uncertainty continued to weigh on sentiment. Meanwhile, Japan faced ongoing inflation pressures and rising domestic yields, reinforcing expectations that the BoJ will continue gradually normalising policy settings.

Geopolitical tensions in the Middle East also remained an important consideration for markets. Concerns surrounding regional stability and shipping routes kept energy markets sensitive to potential supply disruptions and contributed to the broader inflation narrative.

Equities, Bonds and Commodities

Equities

Market performance remained mixed as investors balanced inflation concerns against still-resilient economic conditions. US equities lost momentum as rising yields weighed on valuation-sensitive growth sectors, particularly technology and other long-duration assets. European markets also traded cautiously. Germany’s DAX and France’s CAC 40 faced headwinds from slower growth expectations, while the FTSE 100 proved relatively resilient thanks to its heavier exposure to defensive and commodity-related companies.

Bonds

Bond markets remained central to overall sentiment. Treasury yields stayed elevated as investors adjusted expectations for the Fed’s policy path. The US 10-year Treasury yield remained above 4.5%, while the policy-sensitive two-year yield also held firm as markets priced fewer rate cuts. European sovereign yields moved broadly higher alongside US rates, reflecting similar concerns around inflation and financial conditions.

Commodities

Commodity markets continued to be influenced by geopolitical developments and inflation expectations. Brent crude remained above the $100 per barrel level as supply concerns supported prices. Gold prices weakened during the week, with higher real yields and a relatively firm US dollar reducing demand for non-yielding assets.

Overall, cross-asset performance suggested that investors were becoming increasingly selective rather than abandoning risk altogether, with inflation and policy expectations once again driving asset-allocation decisions.

Sector Performance

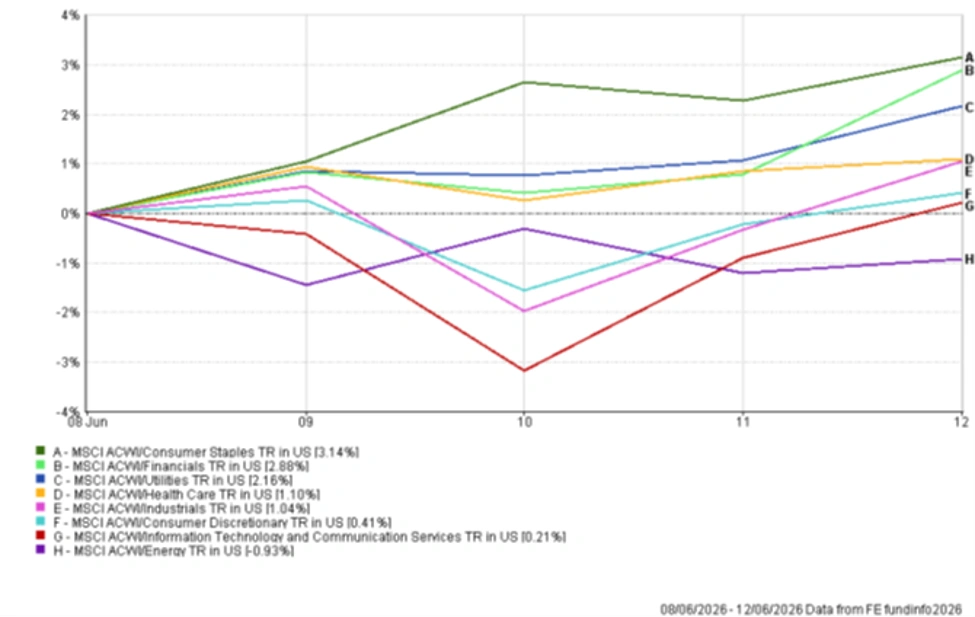

Sector rotation reflected a move towards more defensive and inflation-resilient areas of the market. Consumer Staples delivered the strongest performance, rising 3.14%, as investors favoured stable earnings and resilient cash flows. Financials also performed well, advancing 2.88% amid expectations that higher interest rates could continue supporting profitability.

Utilities gained 2.16%, while Healthcare rose 1.10%, highlighting demand for traditionally defensive sectors. Industrials added 1.04%, supported by relatively stable growth expectations and continued investment spending.

Consumer Discretionary advanced a more modest 0.41%, suggesting that investors remained cautious around the outlook for household spending. Information Technology and Communication Services rose just 0.21%, significantly underperforming the broader market despite remaining positive. Energy was the only sector to finish in negative territory, declining 0.93% as oil-price volatility and profit-taking weighed on performance.

Overall, sector leadership suggested that investors were favouring quality and defensive characteristics while remaining more selective towards growth-oriented areas.

Sector Performance June 8th – 12th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 12 June 2026.

Regional Markets

Regional performance diverged as currency movements, sector composition and exposure to growth-sensitive areas shaped returns.

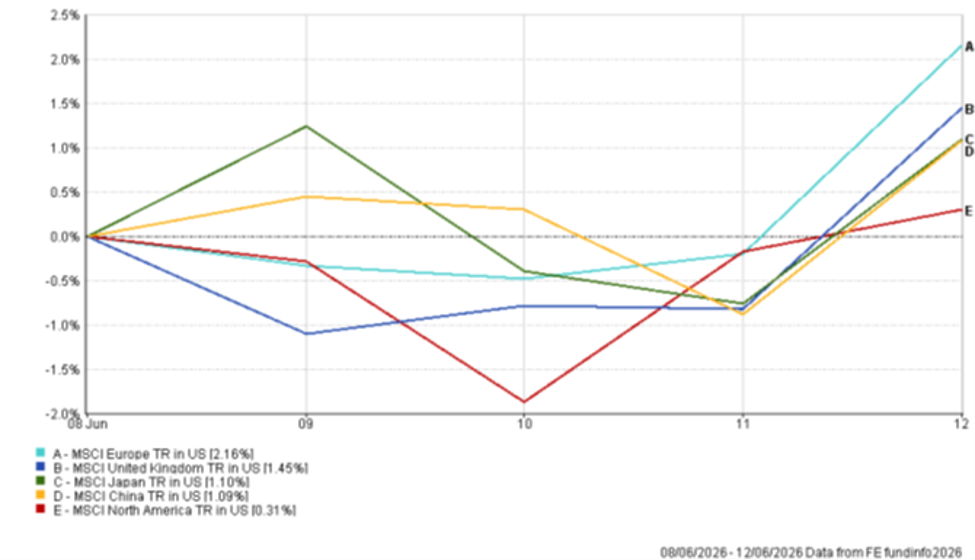

Europe delivered the strongest performance, with the MSCI Europe Index advancing 2.16% in US dollar terms. Improving sentiment towards value-oriented sectors and reduced exposure to large technology companies helped support returns. The UK followed closely, rising 1.45%, as defensive sectors and commodity-related companies helped support returns.

Japan gained 1.10%, supported by improving corporate fundamentals and continued expectations for gradual policy normalisation from the BoJ. China also posted a positive return of 1.09%, despite lingering concerns surrounding the property sector and domestic demand.

North America lagged other regions, with the MSCI North America Index rising only 0.31%. The region’s heavier exposure to mega-cap technology and interest-rate-sensitive growth sectors meant that higher inflation and elevated Treasury yields limited broader upside.

Overall, regional performance highlighted a shift towards markets with stronger value characteristics and lower sensitivity to rising yields.

Regional Performance June 8th – 12th 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 12 June 2026.

Currency Markets

Currency markets reflected changing interest-rate expectations and the continued influence of bond yields on capital flows. The US dollar remained broadly supported as markets reassessed the likelihood of near-term Fed easing.

EUR/USD edged higher during the week, rising from 1.1534 on 8 June to 1.1569 by 12 June. Despite soft economic momentum across the euro area, the single currency found support as investors adjusted expectations around ECB policy and broader dollar positioning.

Sterling also strengthened modestly against the US dollar. GBP/USD rose from 1.3340 to 1.3407 over the week, supported by relatively stable domestic data and a degree of resilience in UK assets.

Against the yen, the dollar remained firm. USD/JPY increased from 160.18 on 8 June to 160.23 by 12 June, although the pair traded as high as 160.57 during the week. Expectations that the BoJ could continue gradually tightening policy helped limit further weakness in the Japanese currency.

GBP/JPY also moved higher, rising from 213.68 to 214.83 over the same period. The move reflected sterling strength and the continued importance of yield differentials in shaping currency markets.

Overall, FX markets reflected the same themes seen across other asset classes, with bond yields and interest-rate expectations remaining the primary drivers of relative currency performance.

Outlook and The Week Ahead

Attention will now turn towards central-bank communication and incoming economic data as investors assess whether inflation pressures are becoming more persistent. Markets will closely monitor the Fed’s policy guidance, along with retail sales, labour-market indicators and further inflation releases across major economies.

Energy markets and geopolitical developments will remain important, particularly given their influence on inflation expectations and commodity prices. Bond yields are also likely to remain a key driver of sentiment, with any further increase potentially placing additional pressure on valuation-sensitive sectors.

For now, investors appear increasingly focused on inflation persistence, policy expectations and financial conditions, with these factors likely to play a greater role in shaping market performance than growth optimism alone.