Softer Labour Data and Cooling Inflation Support a Broader Market Rotation | Weekly Market Recap: 29 June - 3 July 2026

Markets entered July with investor sentiment improving as signs of easing inflation and a cooling labour market reduced concerns that central banks would need to tighten policy further. The shift supported broader participation across global markets, with leadership extending beyond the technology sector for one of the first times in recent months.

While growth remains uneven across major economies, resilient earnings, moderating price pressures and easing bond yields encouraged investors to take a more balanced approach to risk. The result was a week defined by widening market leadership rather than a continued reliance on large-cap technology stocks.

Economic Overview

Markets entered the week assessing whether incoming economic data would alter the outlook for central-bank policy. Early in the week, stronger US job openings reinforced expectations that interest rates could remain elevated for longer. However, softer labour-market data later in the week, alongside cooling inflation across the euro area, helped improve sentiment and reinforced expectations that policymakers could continue taking a measured approach.

In the US, May JOLTS job openings remained at 7.6 million before June non-farm payrolls increased by just 57,000. The unemployment rate edged down to 4.2%, largely because labour-force participation declined, while average hourly earnings rose 0.3% on the month and 3.5% over the year. Together, the data pointed to a labour market that is cooling without reigniting wage pressures, reducing expectations of further near-term Fed tightening.

Across Europe, Germany’s preliminary inflation rate eased to 2.4% from 2.7%, while euro area headline inflation slowed to 2.8% and core inflation eased to 2.4%. Business activity also showed signs of stabilising, with the euro area’s composite PMI returning to the 50 mark. Although growth remained subdued, moderating inflation strengthened confidence that the ECB could continue taking a measured approach to policy.

Elsewhere, China’s official manufacturing PMI returned to expansion territory at 50.3, signalling continued resilience in export-driven industries despite weak domestic demand. The UK remained softer, with services and composite PMIs below 50, while Japan recorded stronger business activity as both PMIs improved. Overall, the week’s data suggested that global growth remains uneven but resilient enough to support a broader rotation across markets rather than a move towards defensive positioning alone.

Equities, Bonds and Commodities

Equities

Markets finished the week on a stronger footing as softer US labour-market data eased concerns over further Fed tightening and encouraged investors to broaden exposure beyond the technology stocks that have led markets for much of the year.

In the US, the Dow Jones Industrial Average rose 2.0% over the week, while the S&P 500 gained 1.8% and the Nasdaq Composite added 2.1%. Although technology continued to perform well, profit-taking emerged across semiconductor and AI-related companies following their strong gains earlier in the year.

European equities outperformed many of their global peers as easing inflation and attractive valuations encouraged investors back into the region. The STOXX Europe 600 advanced 2.6%, Germany’s DAX reached another record high and the FTSE 100 closed at 10,679.03.

Asian markets also finished higher. Japan’s Nikkei 225 gained 1.5%, supported by stronger services activity, while China’s Hang Seng rose 1.3% and the Shanghai Composite added 0.4%. However, ongoing concerns surrounding weak domestic demand and the property sector continued to limit gains in Chinese equities.

Bonds

Bond markets reflected a modest shift in policy expectations. The US 10-year Treasury yield eased to around 4.45%, while the two-year Treasury yield finished near 4.13% as markets reduced expectations of another near-term Fed rate increase. Germany’s 10-year Bund yield held close to 2.92%, while UK gilt yields remained comparatively elevated as investors continued assessing the UK’s inflation outlook.

Commodities

Commodity markets were comparatively stable. Brent crude ended near $71.94 a barrel as improving shipping conditions through the Strait of Hormuz and tentative US-Iran diplomacy eased supply concerns. Gold recovered to around $4,174 an ounce as lower Treasury yields and a softer US dollar increased demand for defensive assets.

Overall, cross-asset performance suggested investors were becoming more confident in broadening exposure beyond technology while continuing to favour areas supported by resilient earnings and improving macroeconomic conditions.

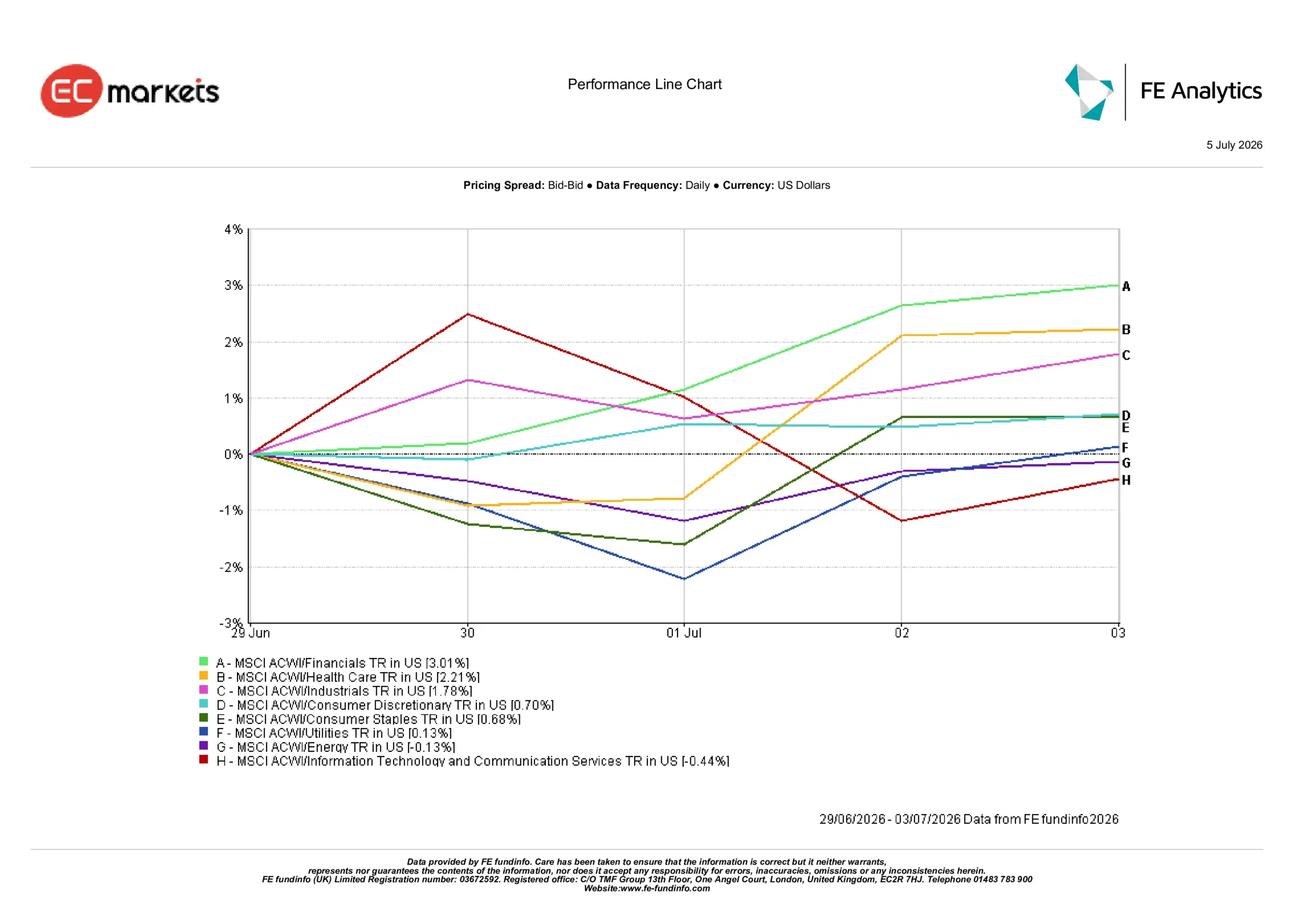

Sector Performance

Sector performance reinforced the week’s broadening market leadership, with investors rotating into financials, healthcare and industrials while reducing exposure to parts of the technology sector that had significantly outperformed earlier in the year.

Financials delivered the strongest return at 3.01%, followed by Healthcare at 2.21% and Industrials at 1.78%. Lower expectations of near-term Fed tightening and improving confidence in Europe’s outlook encouraged investors to broaden exposure beyond technology.

Consumer Discretionary rose 0.70%, Consumer Staples gained 0.68% and Utilities added 0.13%, suggesting investors continued to favour businesses with resilient earnings even as overall sentiment improved.

Energy slipped 0.13% as Brent crude gave back part of its geopolitical premium, while Information Technology & Communication Services declined 0.44% as investors continued rotating away from parts of the AI-driven rally following an extended period of outperformance.

Sector Performance June 29th – July 3rd

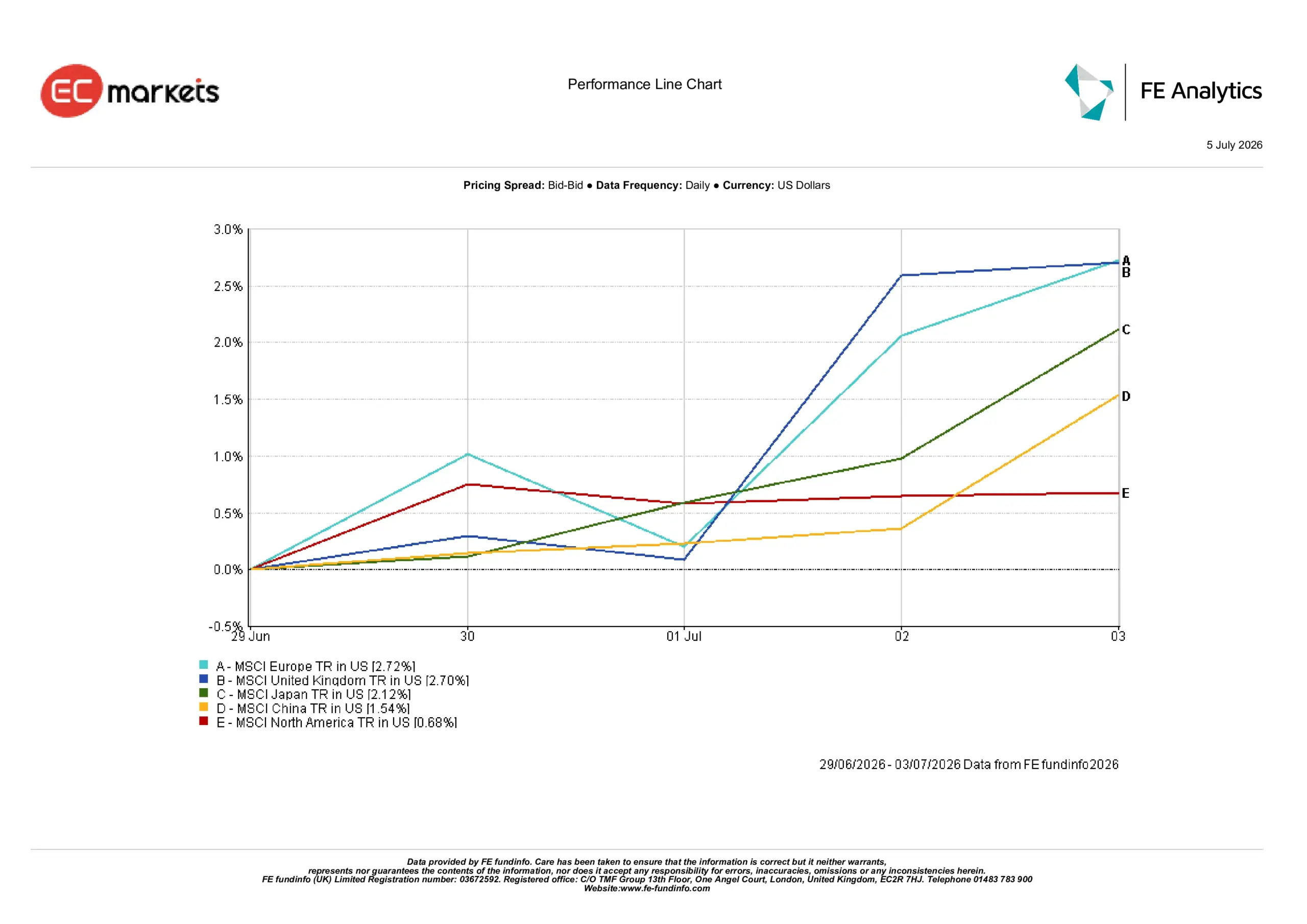

Regional Markets

Regional performance also reflected the broadening market rotation, with Europe and the UK outperforming as easing inflation and attractive valuations drew investors back into the region.

Europe delivered the strongest return at 2.72%, narrowly ahead of the United Kingdom at 2.70%. Japan gained 2.12%, China returned 1.54% and North America lagged with a gain of 0.68%.

Europe’s outperformance reflected moderating inflation, attractive valuations and a more diversified sector mix. The UK benefited from many of the same factors despite softer domestic survey data, while North America’s heavier weighting towards large-cap technology moderated overall gains as investors diversified into other sectors.

Japan was supported by improving services activity and firmer domestic demand, while China’s advance remained relatively restrained as policymakers continued relying on gradual rather than aggressive stimulus measures.

Regional Performance June 29th – July 3rd

Currency Markets

The US dollar lost momentum as the week progressed.

EUR/USD moved from 1.1391 on 29 June to 1.1437 on 3 July, while GBP/USD strengthened from 1.3208 to 1.3352. The moves reflected softer US labour-market data, which reduced expectations of near-term Fed tightening, while sterling also found support as markets continued pricing a relatively restrictive Bank of England compared with several other major central banks.

USD/JPY eased from 161.76 to 161.38 as lower US Treasury yields provided some relief for the yen, although the move remained limited given the wide interest-rate differential between the US and Japan. GBP/JPY rose from 213.56 to 215.48, reflecting sterling’s broader strength against the Japanese currency.

Overall, currency markets reflected a moderation in US dollar strength rather than a broader shift in the interest-rate outlook.

Outlook and The Week Ahead

Attention will now turn to whether the recent rotation across markets can be sustained. Investors will closely examine the Fed minutes for further insight into how policymakers are assessing softer labour-market conditions against inflation that remains above target. Markets will also watch developments across Europe and Asia for further evidence that inflation is easing without a significant slowdown in growth.

Oil prices are also likely to remain in focus after Brent retreated towards pre-conflict levels, as any renewed disruption to Middle East supply could quickly influence inflation expectations and bond yields.

While recent data have reduced the immediate urgency for further policy tightening, investors remain highly sensitive to incoming inflation and labour-market releases. For now, markets appear increasingly willing to broaden participation beyond technology, although the sustainability of that rotation will continue to depend on the balance between inflation, growth and central-bank policy.