Fed Holds Steady Amid Oil Shocks | Weekly Recap: 16-20 March 2026

Markets remained under pressure as central banks held rates and oil-driven inflation tightened conditions across equities, bonds, and currencies.

Economic Overview

As markets opened this week, policymakers faced a choice. Would they treat oil-driven inflation as a temporary shock to the system, or as a reason to delay easing rates altogether?

Escalating tensions between the United States and Iran continue to disrupt markets – particularly energy channels – due to concern over the risk to shipping routes around the Strait of Hormuz.

Because the Strait carries a large share of global oil and LNG supply, even modest disruption can push energy prices higher and rebuild inflation expectations.

The bigger picture here was a familiar one. Oil supply shocks triggered expectations of rising inflation and tightened financial conditions. In response, markets reassessed just how quickly central banks could move toward easing rates.

Against this backdrop, the week’s heavy central bank calendar became less about the immediate level of policy rates and more about signaling. Investors focused on whether policymakers would reassure markets or reinforce the need for policy restraint while inflation risks remain elevated.

- The Fed held the federal funds target range at 3.50%-3.75%, maintaining a data-dependent stance. Markets interpreted the decision as a hawkish hold, signalling that policymakers were not prepared to ease prematurely while energy prices remain volatile.

- The BoE followed a similar path, leaving Bank Rate unchanged at 3.75% while highlighting the risk that sustained energy price strength could feed into second-round inflation effects through wages and corporate pricing behaviour.

- The ECB and BoJ also left policy unchanged, reinforcing the same message: oil prices remain the key transmission channel shaping inflation expectations, policy credibility, and global risk appetite.

Equities, Bonds, and Commodities

Equities delivered a clear verdict on the week’s macro mix. Although central banks did not tighten policy further, the combination of higher oil prices and rising sovereign yields tightened financial conditions enough to keep risk assets under pressure.

US equity markets declined across the board. From Monday to Friday:

- The S&P 500 fell ~1.9%, the Nasdaq Composite ~2.2%, and the Dow ~2.2%, as rising real yields and the removal of near-term cut expectations weighed on duration-sensitive multiples. The repricing of inflation risk through higher oil prices and bond yields translated directly into pressure on equity valuations.

- In Europe, the STOXX Europe 600 fell ~3.8%, marking a third straight weekly decline, while the FTSE 100 lost ~1.4% as the BoE’s hawkish hold and energy-driven inflation concerns weighed on sentiment.

Bond markets absorbed the shock mainly through the inflation channel. The US 10-year rose to ~4.39% by Friday, the Bund 10-year to ~3.04%, and the UK 10-year toward ~4.9%-5.0%, reflecting rebuilt term premia and higher inflation uncertainty.

Commodities remained central to the week’s moves. Brent traded roughly $105-$112 and ended near $110. Gold fell sharply as the stronger dollar and rising real yields dominated safe-haven flows.

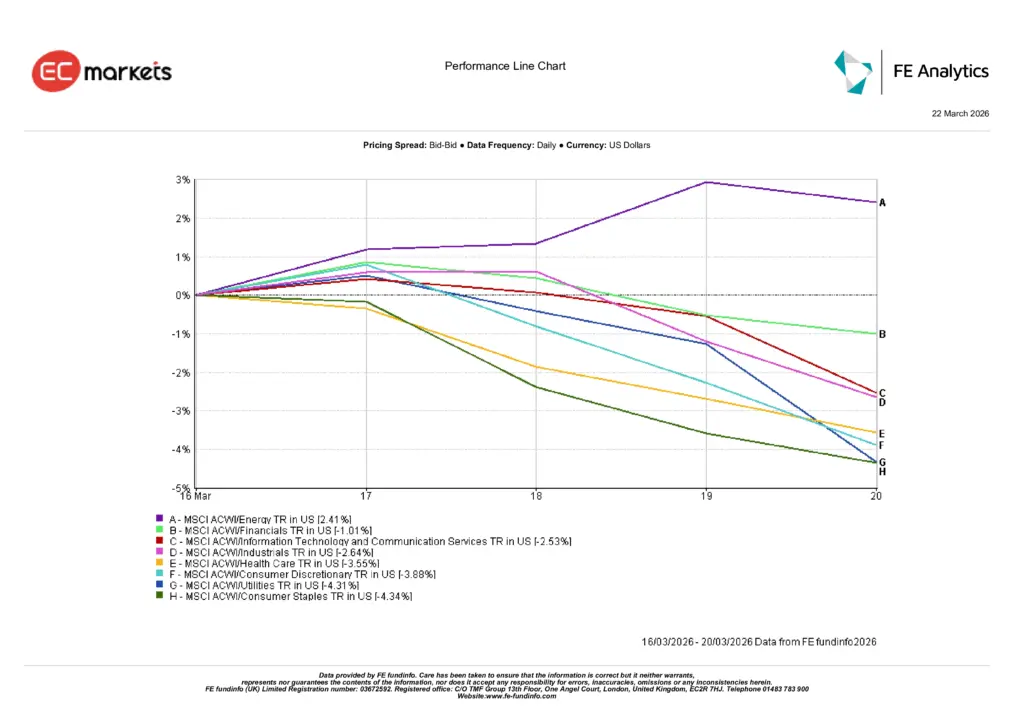

Sector Performance

Sector performance highlighted how investors positioned portfolios in response to the energy shock.

Energy was the clear outperformer, with the MSCI ACWI Energy sector rising about +2.4% during the week. The surge in crude prices supported earnings expectations and drove investor rotation toward commodity-linked cash flows.

Beyond Energy, performance largely reflected varying degrees of weakness.

- Financials: ~-1.0%: Relatively resilient as higher yields supported profitability, though sentiment remained cautious

- Technology & Communication Services: ~-2.5%: Pressured by higher long-term rates

- Industrials: ~-2.7%: Impacted by rising input costs

- Consumer Discretionary: ~-3.9%: Weighed down by fuel-driven pressure on household spending

Traditional defensives also struggled. Health Care fell about 3.6%, Utilities declined around 4.3%, and Consumer Staples dropped roughly 4.4%, highlighting how rising yields can pressure sectors with bond-like characteristics.

📊 Source: FE Analytics. All indices total return in USD. Data as of 20 March 2026.

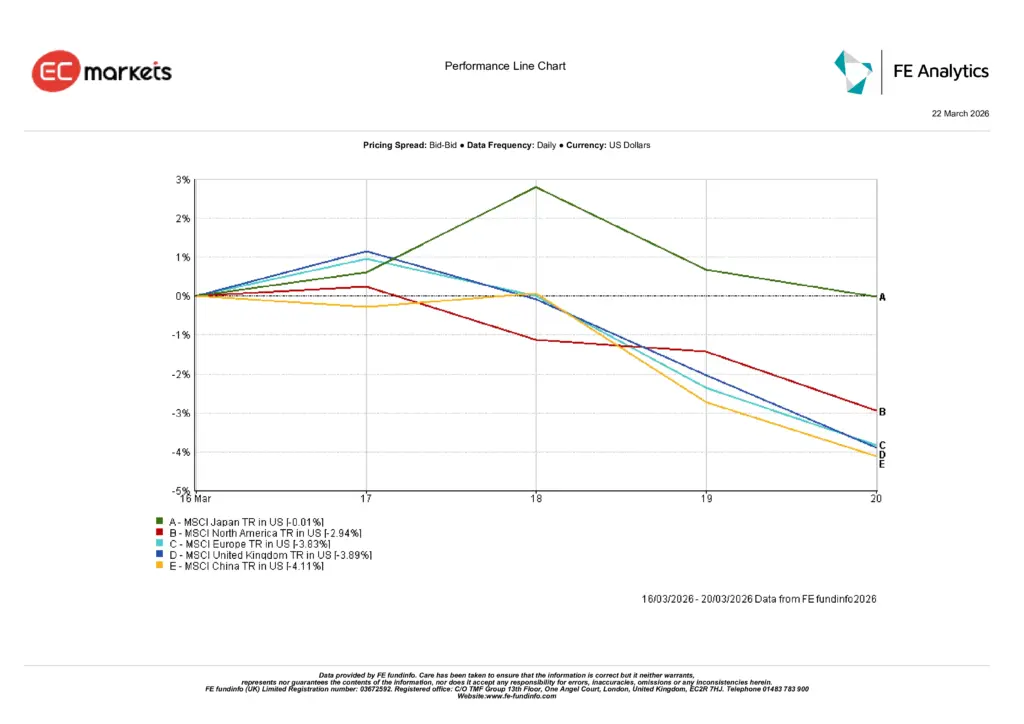

Regional Markets

Regional equity performance showed broad weakness, though differences between regions reflected exposure to the energy shock.

- North America declined meaningfully, with MSCI North America falling about -2.9%, broadly tracking US equity weakness.

- Europe experienced deeper losses, with MSCI Europe declining roughly -3.9%, reflecting the region’s dependence on imported energy and rising sovereign yields. The UK followed closely, with MSCI UK down about -4.0% as higher gilt yields reinforced inflation concerns.

- Asia showed limited resilience. MSCI Japan was broadly flat, supported by occasional rebounds in export-oriented stocks. MSCI China fell about 4.1%, while Hong Kong’s Hang Seng declined roughly 2.2% and the Shanghai Composite dropped around 3.1% during the week.

The regional pattern reinforced a clear message: markets with higher energy dependence and greater sensitivity to rising yields experienced the largest drawdowns.

📊 Source: FE Analytics. All indices total return in USD. Data as of 20 March 2026.

Currency Markets

Currency markets delivered a more balanced signal compared with the previous week.

- The US dollar retained safe-haven support, though it did not strengthen consistently throughout the period. DXY ended broadly unchanged, with elevated intraweek volatility driven by central bank announcements and oil price movements.

- The Euro strengthened modestly, with EUR/USD rising about +0.6%, partly reflecting dollar consolidation after earlier safe-haven flows.

- Sterling also edged higher, with GBP/USD up roughly +0.2%, though the path remained volatile as markets balanced BoE expectations against inflation risks.

- In Japan, USD/JPY finished nearly flat (+0.1%), with notable daily swings highlighting the competing influence of safe-haven demand and rate differentials.

Cross rates reflected similar dynamics. GBP/JPY rose around +0.3%, supported by sterling’s yield advantage relative to the yen.

Overall, FX markets reflected a shift toward short-term positioning driven by policy signals and risk sentiment, rather than a single dominant trend.

Outlook and the Week Ahead

Markets now face a familiar dilemma. The energy shock continues to influence inflation expectations, but its longer-term impact will depend on whether oil prices stabilise or remain elevated.

If geopolitical tensions ease and shipping routes remain secure, the inflation premium embedded in oil prices could gradually decline. In that scenario, sovereign yields may stabilise and equity markets could begin rebuilding their risk appetite.

However, if disruption around the Strait of Hormuz persists and oil prices remain elevated, markets may continue to price a higher inflation baseline. Sustained supply disruption would translate into tighter financial conditions and delayed policy easing.

Central banks have clarified their reaction function. Policymakers are not tightening further, but they are also unwilling to support risk assets prematurely while inflation risks remain elevated.

For investors, the key variables to monitor will be:

- Wage growth

- Inflation expectations

- Evidence of demand destruction

These will determine whether the current oil shock proves temporary or evolves into a more persistent macro challenge.

From a positioning perspective, the message remains clear:

Markets are favouring direct commodity exposure and energy-linked assets while reducing exposure to both cyclical sectors and bond-proxy defensives.