Oil Shock Reprices Inflation Risk as Markets Rotate Back to Defence | Weekly Recap: 02-06 March 2026

Economic Overview

Markets spent the week re-sorting the hierarchy of risks as geopolitics moved from background noise to a direct macro input. Growth softened at the edges, but the jump in energy linked inflation risk set the tone because the Israel and Iran escalation and disruptions in the Strait of Hormuz revived an oil premium. When shipping flows look vulnerable, inflation expectations rise and rates reprice higher, which tightens financial conditions and pressures equities.

Positioning amplified the move. Investors had been leaning toward a benign disinflation path and a later year policy pivot. The oil shock forced a reassessment of supply side fragility, so breakevens and term premia moved first, then equity risk appetite and volatility adjusted. The cause was a sudden external energy shock. The effect was a rebuild of higher for longer premia that overshadowed softer growth signals.

US labour data added complexity. Payrolls fell by 92,000 and unemployment rose to 4.4%, with strike activity weighing on health care employment. Normally this would ease policy expectations. With an oil shock in the background, it tilted the narrative toward a stagflation lite mix, because softer labour momentum collided with renewed inflation risk.

Policy signals outside the US stayed stable but vigilant, as China highlighted flexibility, Japan monitored external volatility, and Europe focused on pass through risks rather than reacting mechanically to oil.

Equities, Bonds and Commodities

Equities traded under a clear risk budget constraint, with broad drawdowns and brief rebounds that faded whenever oil moved higher or yields pushed up. The S&P 500 closed the week at about -2.1%, the Nasdaq at -1.6%, and the Dow at -2.9%. The VIX finishing at 29.49 signalled a shift from simple de risking to hedge first behaviour. The cause was the rebuild in inflation premia and the jump in uncertainty. The effect was a preference for optionality rather than outright exposure.

Rates absorbed the shock through an inflation lens. The US 10 year moved from 4.052% to 4.132% and the 2 year from 3.487% to 3.556%. Europe saw a sharper move as Bund and gilt yields rose, which tightened financial conditions for rate sensitive equities. The cause was a supply driven energy impulse that central banks cannot easily offset. The effect was higher discount rates that weighed on duration heavy assets.

Commodities remained the centre of gravity. Brent rose from $77.74 to $93.04 and WTI from $71.23 to $90.90, while gold finished lower as a stronger dollar and higher real yields muted safe haven demand. The effect was a broad risk off rotation and a reset in inflation linked premia.

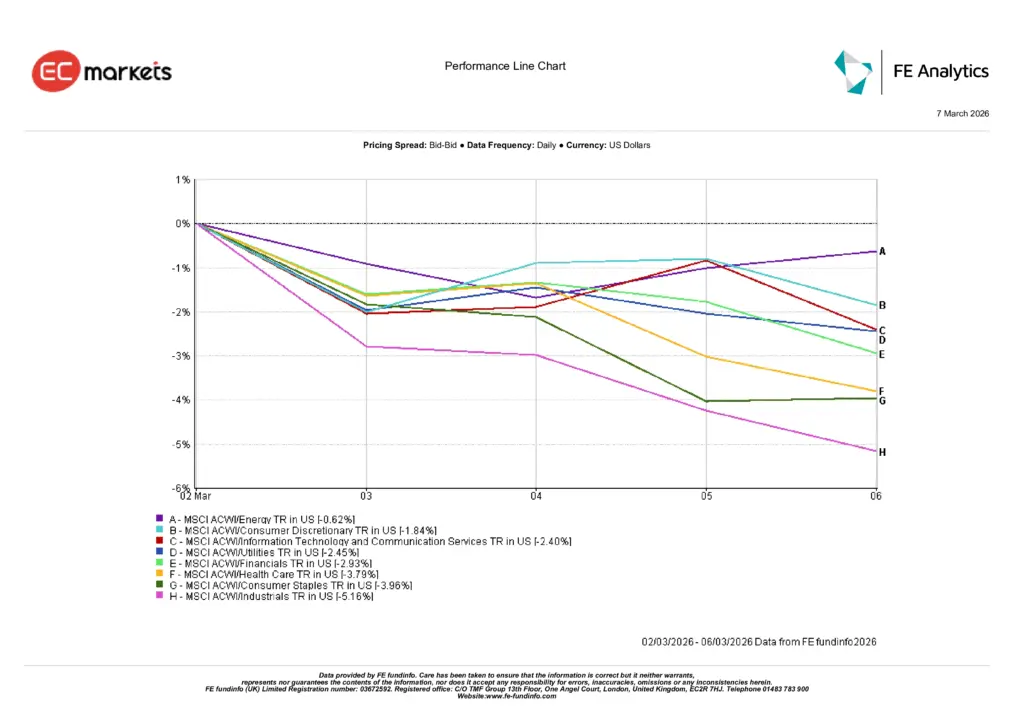

Sector Performance

The sector pattern stayed aligned with a market repricing inflation through rates rather than earnings. Energy held up at -0.62%, supported by stronger crude and the hedge it provides when inflation risk rises. Most other sectors acted as funding sources because higher discount rates reduce the present value of future cash flows and raise the hurdle for risk.

Consumer Discretionary at -1.84% and Information Technology and Communication Services at -2.40% reflected weaker risk appetite and a higher rate regime. The effect was clear underperformance in longer duration growth and consumer names sensitive to financing conditions. Utilities at -2.45% and Financials at -2.93% showed that higher sovereign yields did not translate into cleaner net interest margins, producing middling results.

Health Care at -3.79% and Consumer Staples at -3.96% demonstrated that defensives did not shield performance in a rates driven selloff. Industrials, the weakest at -5.16%, showed the impact of higher energy costs and fading growth expectations, leaving Energy as the only reliable hedge.

Sector Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 6 March 2026.

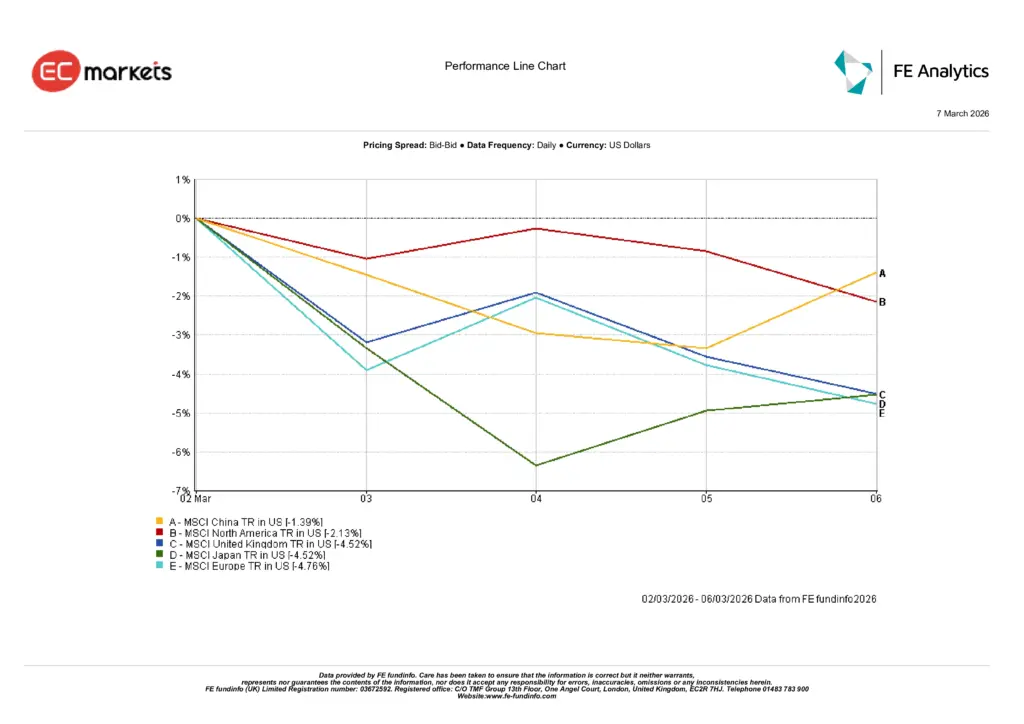

Regional Markets

Regional moves tracked energy exposure and duration sensitivity. China was the relative outperformer at -1.39%, supported by policy signals and a lower external beta, so the effect was a more contained drawdown. North America closed at -2.13%, broadly matching the global risk off tone while avoiding the heavier losses seen in energy vulnerable markets.

The United Kingdom and Japan both finished at -4.52%, reflecting margin pressure from higher input costs and sensitivity to the rates move. Europe, at -4.76%, was the weakest major region. The cause was elevated energy vulnerability combined with a sharper sovereign yield repricing. The effect was deeper de rating as investors priced tighter conditions and second round inflation risks.

Together, the regional pattern reinforced a simple message. When an energy shock lifts inflation premia and pushes yields higher, regions with higher import dependence and greater equity duration lag, while those with credible policy support experience more measured declines.

Regional Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 6 March 2026.

Currency Markets

FX reflected a straightforward risk off preference for liquidity. The Dollar Index rose across the week as investors sought safety and funding flexibility. The cause was a jump in uncertainty tied to oil and rates. The effect was broad based dollar strength that overshadowed idiosyncratic stories. The euro eased against the dollar in line with Europe’s energy sensitivity. Sterling finished near flat on the week after intraday swings that traced changing Bank of England expectations. Yen crosses moved higher because rate differentials and global dollar demand outweighed safe haven dynamics by the close.

Outlook and The Week Ahead

The next step depends on whether energy stays a risk premium or turns into a pipeline shock. If shipping flows and insurance conditions around the Strait of Hormuz stabilise, the premium can fade and rates can settle. If disruption persists, inflation expectations will pull term premia higher and equities will keep trading with a hedge first bias. The cause is the condition of physical flows and freight risk. The effect is the path of rates and the willingness to hold equity exposure.

The near term focus is on US CPI on Wednesday 11 March. If price gains broaden beyond energy sensitive components, policy easing hopes will be pushed further out. If the impulse stays contained, the market can re build risk selectively. The Federal Reserve meeting on 17 to 18 March will update projections and show how policymakers are weighing softer labour momentum against renewed supply side inflation risk. In Europe the watchpoint is whether the ECB maintains its good place framing if energy volatility persists, because a live energy shock raises the bar for risk and supports a premium on quality and cash flow visibility.