Banking on Yields: How Higher Rates Reshape the Financial Sector

For more than a decade, money was cheap — maybe too cheap?! Now that era is gone. Rates and bond yields have jumped back to levels we last saw before the financial crisis, and the adjustment is shaking things up. Some financial firms are thriving, others are struggling to catch their breath. And investors? The ripple effects go well beyond bank earnings. It’s easy to think higher rates are automatically “good for banks.” The reality is that it’s messier!

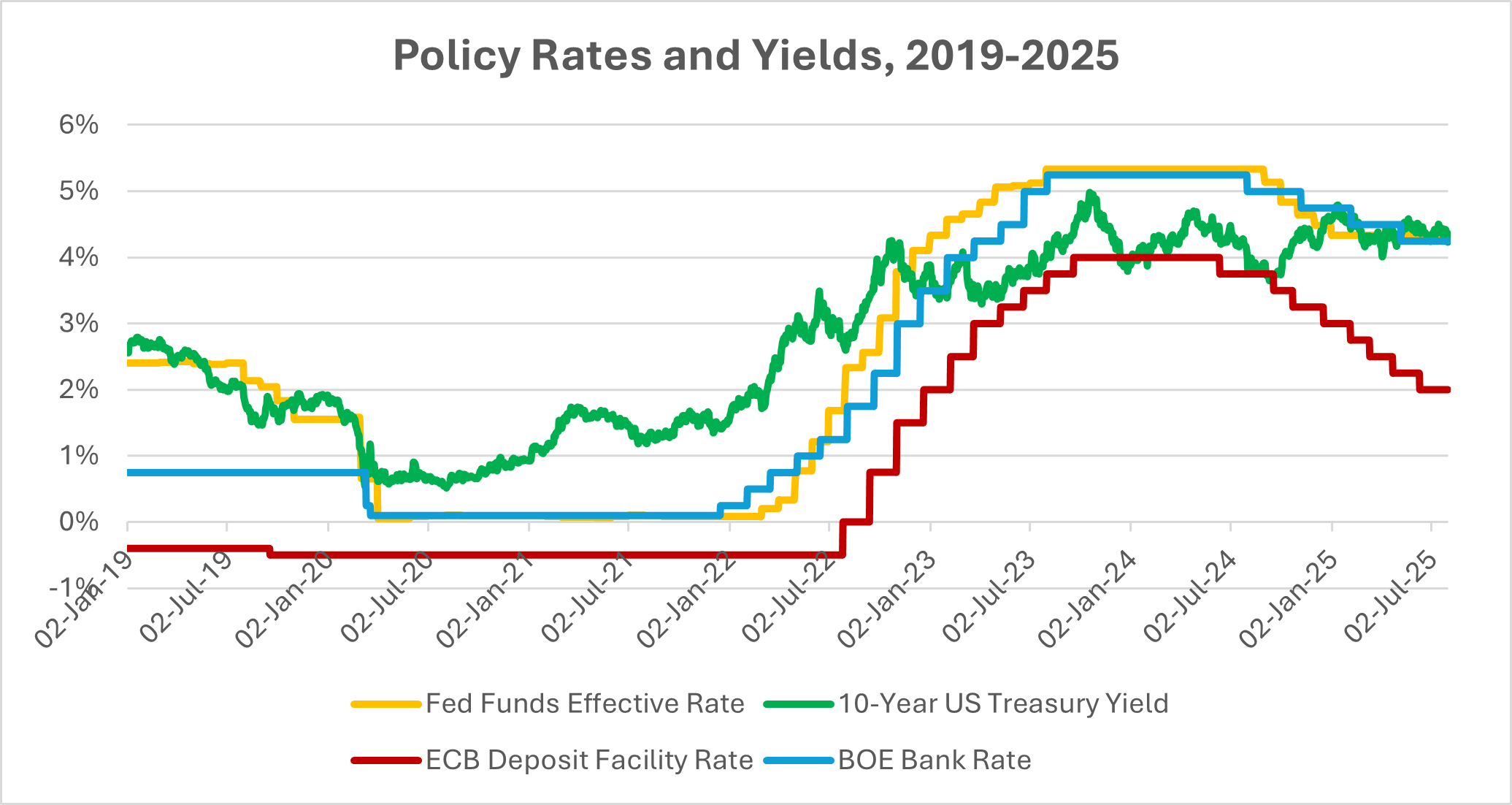

From 0 to 5 in Record Time

The shift has been brutal in speed. The Fed moved from near 0% in 2021 to above 5% in just two years, that’s the sharpest climb in decades. The ECB and BoE followed the same path. Bond markets didn’t take it quietly: prices tumbled, yields spiked. Suddenly, 4-5% on so-called risk-free assets felt normal again. Sounds like a relief for savers? Sure! But for the financial system, the question is different. What does that reset actually mean?

Sources: Board of Governors of the Federal Reserve System (US) via FRED®; European Central Bank via FRED®; Bank of England Database. Data as of 26 August 2025.

Policy rates and long yields reset sharply after 2021, establishing a higher-yield regime across the US, Eurozone and UK.

The Early Winners

Banks were the first to feel the upside. Loan rates shot up faster than deposit costs, and margins fattened, at least in the early stretch before customers started demanding more on savings. Bank of America (BoA), for instance, pulled in 14% more net interest income in Q2 2023. That doesn’t sound ground-breaking until you remember: for a bank its size, that’s billions in extra income, basically overnight. BNY Mellon saw a 33% leap too.

Insurers, meanwhile, finally got a break. For years their life products looked anaemic in a zero-rate world; suddenly their investment portfolios were paying real returns again. Analysts reckon industry investment income could rise around 40% in coming years, pushing operating profits even higher. Pension funds and annuity providers, who’d spent a decade starved of yield, also looked a little less desperate.

So yes, the early phase felt like a gift. But, as always in finance, there’s usually a catch lurking a few pages further on.

Higher for Longer

Central bankers now repeat the same refrain: rates may stay up “as long as it takes” to stamp out inflation. That sets the stage. If yields move higher alongside solid growth, financials can cope, even thrive. And in 2023 the global economy showed resilience. With jobs holding up, consumers kept spending, some firms even saw inflation boost revenues in nominal terms.

But there’s another side. Debt service costs are climbing everywhere. Mortgages, corporate loans, government borrowing. Emerging markets face sharper risks still. High US yields tempt capital away and raise refinancing costs, and that stress peaks when big chunks of debt mature.

Winners, Losers, and Ripples Across Assets

Not all banks are equal. Retail-focused lenders with stable deposits came out on top early. Others, like Silicon Valley Bank (SVB), mishandled interest-rate risk, saw bond portfolios collapse in value, and unravelled almost overnight.

Beyond banks, investors changed habits fast. Cash mattered again. Money market funds yielding around 5% pulled in trillions, putting stocks behind. Tech, built on distant profits, got hit the hardest. The Nasdaq fell 33% in 2022 (its worst year since 2008) as discount rates undercut valuations. Gold, which usually struggles when real yields rise, also lost some shine. Real estate faced perhaps the toughest squeeze: office landlords, already weakened by remote work, suddenly faced refinancing at punishing rates. With US banks exposed to about a quarter of commercial property loans, those cracks matter.

Credit Clouds Forming

Here’s where the story flips. By late 2023, defaults were climbing, nearly double the year before. Junk bond yields neared 9%, squeezing weaker firms. Small and mid-sized businesses, dependent on banks, felt the crunch first.

At the same time, deposit pressure grew. Savers wanted better rates or took their money elsewhere, narrowing bank margins. Loan demand cooled. The initial profit surge from higher rates may already have peaked, leaving banks to juggle slower growth, higher funding costs, and rising credit risk.

Takeaway

For investors, the landscape has changed. The upside: income is finally back. Bonds, bills, even cash now compete with stocks, allowing portfolios to be more balanced than they’ve been in years. But staying alert and cautious is just as important.

The playbook now? Stick with lenders and insurers that have strong risk controls and solid deposit bases. Be wary of highly leveraged borrowers, shaky REITs tied to offices, or weaker emerging-market debt. There are opportunities – locking in attractive bond yields, or buying financial stocks that can weather higher funding costs – but also plenty of traps.

Rates have redrawn the map. Whether they remain a tailwind or tip the economy into something harsher will depend on how growth holds up. For now, balance is the name of the game: diversify, keep an eye on credit cracks, and remember that in this new era, yield cuts both ways.