Energy Volatility and Geopolitical Tensions Drive Market Swings | Weekly Recap: 30 March - 3 April 2026

Global markets saw volatile trading as energy price swings and geopolitical tensions pushed yields higher and tightened financial conditions, while a mid-week improvement in sentiment supported a selective rebound in equities.

Economic Overview

Markets entered the week navigating renewed upward pressure in energy prices, with Brent crude moving above $110 per barrel alongside heightened geopolitical tensions in the Middle East. While the primary catalyst remained the repricing of oil-related supply risks, investor focus quickly shifted to how this inflation impulse could influence central-bank policy and broader financial conditions.

The macro sequence was familiar. The cause was a resurgence in commodity-driven inflation risk. The effect was increased volatility across sovereign yields, currencies and risk assets. The US 10-year Treasury yield rose toward 4.4% as markets reassessed the balance between persistent inflation and a softening global growth outlook.

Central bank messaging remained cautious. The Federal Reserve held rates at 3.50%-3.75%, maintaining a data-dependent stance and signalling that meaningful progress on inflation is still required before easing can be considered. The ECB and Bank of England echoed this tone, highlighting energy costs and wage dynamics as ongoing upside risks.

In Asia, the Bank of Japan continued to manage imported inflation pressures while maintaining an accommodative stance to support domestic stability. Meanwhile, Chinese data pointed to uneven momentum, with the Caixin Services PMI moderating to 52.1 in March.

Overall, the macro backdrop remains defined by a persistent dilemma: inflation risks remain present even as tighter financial conditions begin to weigh on growth, which the ECB currently projects at around 0.9% for the year.

Equities, Bonds and Commodities

Global equities experienced a volatile week as markets reacted to shifting geopolitical headlines and fluctuations in energy prices.

Mid-week, sentiment improved on tentative signs of de-escalation in the Middle East. The S&P 500, Nasdaq and STOXX Europe 600 all posted gains during this rebound. However, the move lacked follow-through, with markets stabilising rather than extending higher into the week’s close, a reflection of continued macro uncertainty.

US equities finished broadly flat after recovering earlier losses. European markets followed a similar pattern, while the FTSE 100 remained relatively resilient, supported by its exposure to defensive and commodity-linked sectors.

In Asia, Japanese equities posted strong mid-week gains before easing into the final session. Chinese and Hong Kong markets remained more cautious, reflecting softer domestic data.

Bond markets reinforced the inflation narrative. Sovereign yields moved higher overall, supported by stronger US labour data, with nonfarm payrolls rising by 178,000 in March. The US 10-year yield moved toward 4.34%, while German Bund yields approached 3.00% and UK gilts remained firm as inflation expectations were repriced.

Commodities were the most reactive asset class. Oil prices experienced sharp swings, with Brent peaking near $119 before pulling back on easing tensions and then rebounding as risks resurfaced. Gold initially benefited from safe-haven demand, reaching around $4,700 mid-week, before moderating as risk sentiment stabilised.

The message remains consistent: energy markets continue to act as the primary transmission channel through which geopolitical developments feed into inflation expectations and financial-market volatility.

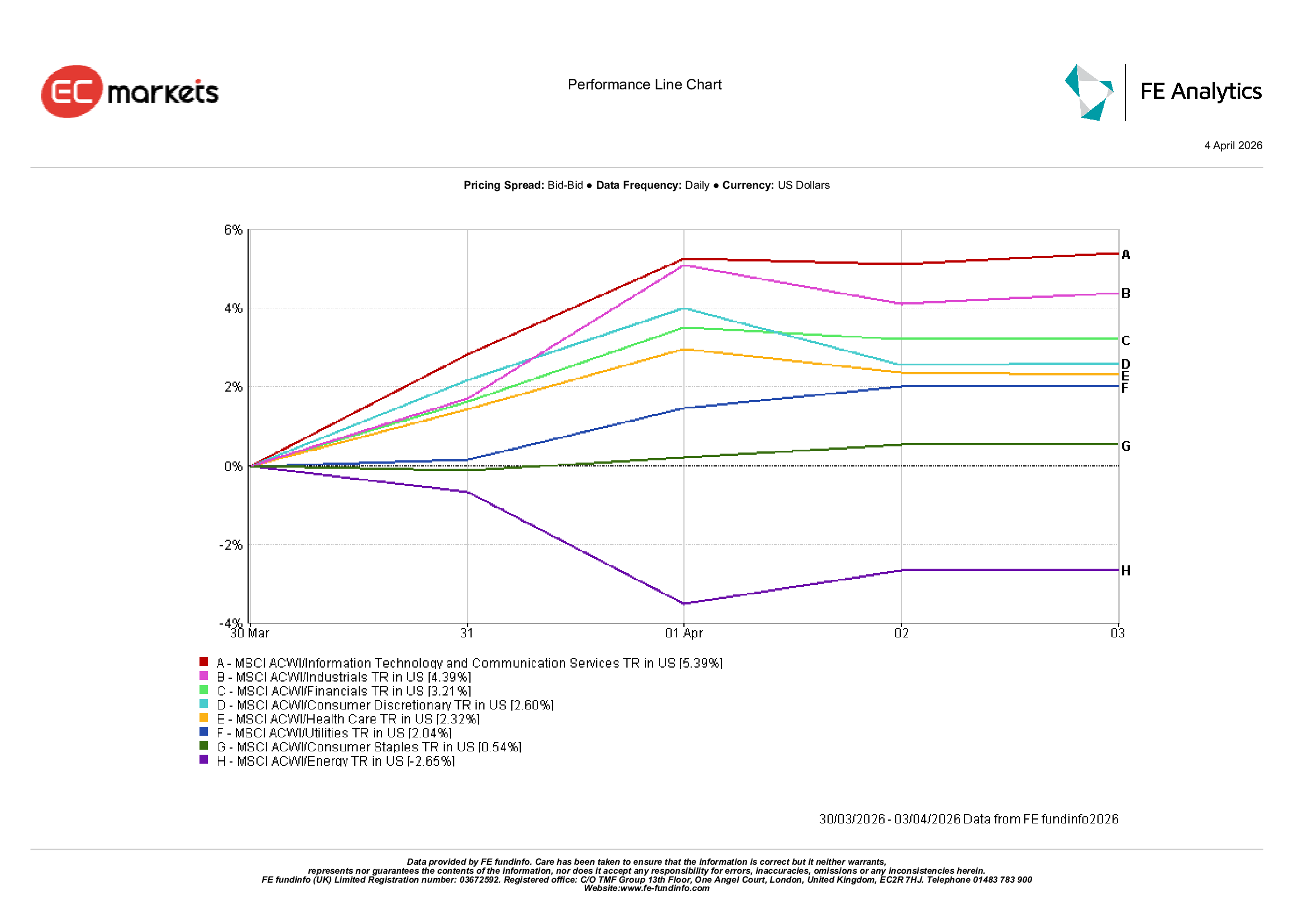

Sector Performance

Sector performance reflected a clear shift in positioning as risk appetite improved mid-week.

Growth and cyclical sectors led the rebound. Information Technology & Communication Services rose 5.39%, Industrials gained 4.39%, and Financials advanced 3.21% as sentiment improved.

Consumer Discretionary added 2.60%, suggesting a modest re-engagement with growth-sensitive areas.

Defensive sectors delivered more measured gains. Health Care rose 2.32%, Utilities increased 2.04%, and Consumer Staples edged up 0.54%.

Energy was the only sector to decline, falling 2.65%, as oil prices pulled back from earlier highs during the week.

Overall, the rotation suggests investors were temporarily willing to look through the inflation shock, reallocating toward growth and cyclicals as geopolitical fears eased.

Sector Performance, March 30th – April 3rd 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 3 April 2026.

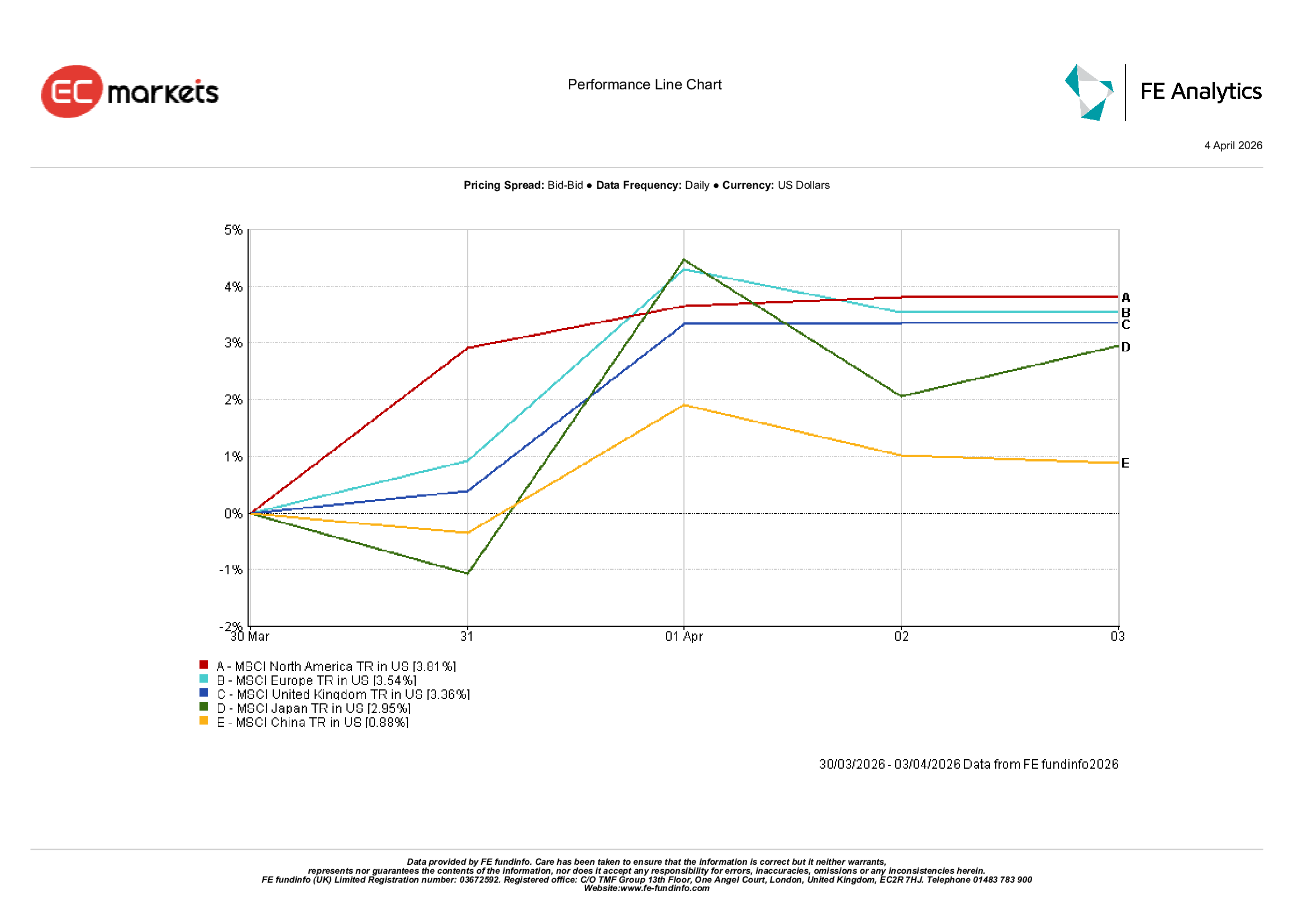

Regional Markets

Regional equity markets posted broad gains, though performance varied.

North America led, with MSCI North America rising 3.81% as US equities recovered from earlier volatility.

Europe followed, with MSCI Europe up 3.54%, while the UK gained 3.36%, supported by its exposure to commodities and defensive sectors.

In Asia, Japan advanced 2.95% as investors rotated into export-oriented names.

China lagged, rising 0.88%, reflecting ongoing caution amid mixed domestic data.

The regional pattern highlights selective risk appetite, with stronger performance in markets supported by sector composition and improving sentiment.

Regional Performance, March 30th – April 3rd 2026

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 3 April 2026.

Currency Markets

Currency markets reflected the push and pull between risk sentiment and interest-rate differentials.

The US dollar weakened early in the week as geopolitical tensions eased, supporting EUR/USD and GBP/USD. However, the dollar regained strength into the week-end as US yields rose following stronger labour data.

Sterling broadly mirrored this pattern, ending slightly weaker as rate differentials once again favoured the dollar.

The Japanese yen remained under pressure throughout, with USD/JPY holding near recent highs as yield differentials continued to dominate.

Crosses such as GBP/JPY were broadly stable, with sterling weakness offset by continued yen softness.

Overall, FX markets reinforced a consistent theme: interest-rate differentials and bond-market dynamics remain the dominant drivers.

Outlook and The Week Ahead

Looking ahead, markets remain focused on the interaction between geopolitics, energy prices and inflation expectations.

If energy prices stabilise, sovereign yields may ease, supporting risk assets and allowing investors to rebuild exposure to cyclicals.

However, sustained geopolitical tensions could maintain a higher inflation baseline. The cause would be continued commodity volatility. The effect would be prolonged central-bank caution and delayed expectations for policy easing.

Key data to watch includes US labour-market updates, inflation releases and central-bank commentary.

The core question remains: can the global economy absorb higher energy prices without triggering a broader tightening in financial conditions?