Which Assets Come Out On Top When Inflation Rises?

Inflation does more than increase everyday costs. It also shapes how different financial assets perform over time. While some assets may struggle to keep pace with rising prices, others have historically shown the potential to grow beyond inflation. Understanding these differences can help explain market behaviour and long-term trends.

How Inflation Affects Cash and Savings

Cash is often seen as stable and low risk. It is easy to access and does not fluctuate in value like markets do. However, its main limitation is that it may not keep pace with inflation.

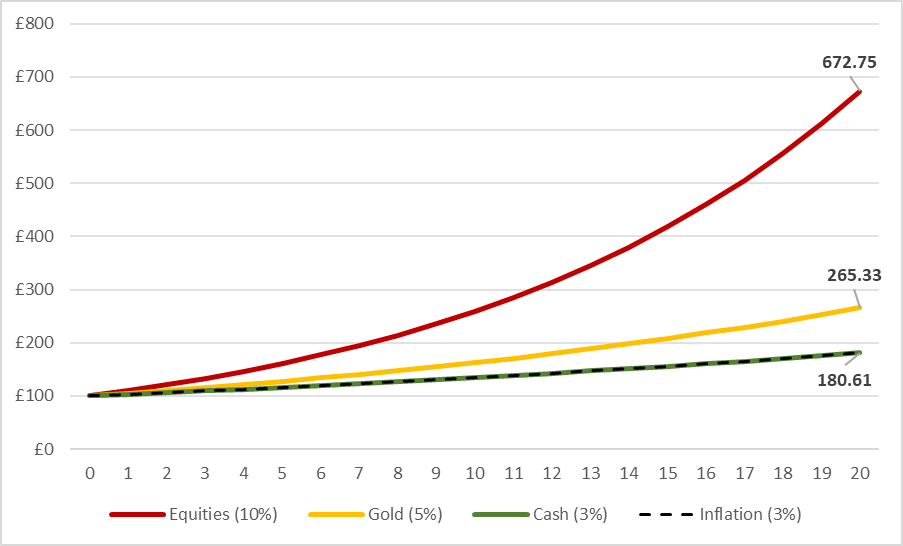

Historically, returns on savings have often been close to inflation levels. If both inflation and interest rates are around 3%, £100 could grow to roughly £181 over 20 years. While this looks like growth, the purchasing power remains broadly the same in real terms.

If interest rates fall below inflation, cash can gradually lose value. In practical terms, this means savings may grow in nominal terms, but what they can actually buy may not increase.

How Inflation Affects Equities

Equities, or shares in companies, tend to behave differently. Over longer periods, stock markets have historically delivered higher returns than inflation.

For example, broad equity markets have averaged around 10% annual returns in nominal terms over time. After adjusting for inflation, this is closer to around 7% in real terms. At this rate, £100 invested over 20 years could grow to around £673 nominally, or roughly £372 after accounting for inflation.

One reason for this is that businesses can sometimes pass higher costs on to consumers by increasing prices. This can help revenues and earnings grow alongside inflation. However, this is not always straightforward. In the short term, rising inflation can lead to higher interest rates, which may put pressure on stock prices and increase volatility.

How Inflation Affects Gold and Commodities

Gold and commodities are often discussed in the context of inflation because of their link to real-world prices.

Gold is commonly viewed as a store of value. When inflation rises and currency purchasing power falls, gold prices often move higher in nominal terms. For example, £100 invested in gold over 20 years might grow to around £265. After adjusting for inflation, this is roughly £147 in today’s terms.

Other commodities, such as energy or agricultural products, can also rise during inflationary periods because they are directly linked to production costs. However, these assets can be volatile and influenced by factors such as supply disruptions, geopolitical events, and currency movements. They do not always move in line with inflation in a predictable way.

Growth of £100 Over 20 Years Across Different Assets

This becomes clearer when viewed over time, where the impact of compounding returns and inflation can lead to significantly different outcomes across asset types.

The Risks of Different Assets During Inflation

No asset consistently performs best during inflation.

Cash can lose purchasing power if returns remain below inflation. Equities can be volatile, particularly during periods of rising interest rates or economic uncertainty. Gold and commodities can experience sharp price swings and may not always provide consistent protection.

Understanding these trade-offs is important, especially when looking at how different assets behave over time.

Is It Suitable for Everyone?

Different assets serve different purposes, and their suitability depends on individual goals, timeframes, and risk tolerance.

Cash may be more appropriate for short-term needs where stability is important. Equities are typically associated with longer-term growth, but require the ability to manage short-term fluctuations. Commodities and gold may play a role in certain situations, but they are not always predictable.

There is no single approach that fits everyone, which is why understanding how these assets behave can be more useful than focusing on any one option.

Bottom Line

Inflation gradually reduces what money can buy, but not all assets respond in the same way.

Cash offers stability but may struggle to keep up with rising prices. Equities have historically delivered growth above inflation over the long term, although they can be volatile. Gold and commodities may rise during inflationary periods, but they are influenced by multiple factors and are not always consistent.

Understanding these differences can provide useful context when interpreting market behaviour, particularly during periods of rising prices.

Inflation and Asset Performance FAQs

How does inflation affect different assets?

Inflation affects assets in different ways. Cash may lose purchasing power over time, while equities have historically offered growth potential above inflation. Commodities and gold may rise during inflationary periods, but can be volatile.

Which assets perform best during inflation?

There is no single asset that consistently performs best. Equities have historically delivered long-term growth, while commodities and gold may react more directly to inflation changes.

Does cash lose value during inflation?

Yes. If inflation is higher than interest earned on savings, the real value of cash can decline over time.

Why do equities sometimes struggle during inflation?

Rising inflation can lead to higher interest rates, which may increase borrowing costs and reduce equity valuations, particularly in the short term.

Is gold a good hedge against inflation?

Gold is often viewed as a store of value, but it does not always move consistently with inflation and can experience periods of volatility.