Rotation Builds as Policy Noise Meets Geopolitics | Weekly Recap: 16-20 February 2026

Economic Overview

It was a week that invited investors to look past the headlines and focus on what really mattered. In the US, the Supreme Court struck down a set of emergency‑authority tariffs, briefly easing some pressure on import costs, but the administration quickly moved toward a new set of across‑the‑board duties. The result was a mixed picture rather than a clean shift, with markets weighing the possibility of some relief now against the chance of renewed pressure later. At the same time, US-Iran developments moved between diplomatic talks in Geneva and news of additional military assets heading toward the region, a combination that kept a modest premium under oil prices without unsettling broader risk sentiment.

Across Europe, the ECB held its course and President Christine Lagarde dismissed speculation about her future, helping keep the focus on data, earnings and the broader macro backdrop rather than political noise.

In short, a blend of tariff news, geopolitical updates and steady central‑bank guidance shaped the week. Yields drifted a little higher, the dollar found a slightly firmer footing, and commodities split along familiar lines, energy lifted by geopolitics, while gold held its role as a measured hedge.

Equities, Bonds & Commodities

Equities advanced selectively rather than in a straight line. US indices posted mixed‑to‑positive weekly prints, with style tilts doing most of the storytelling rather than a single index move.

Rates behaved the way they often do when policy risk feels slightly more inflationary than disinflationary: the US 10‑year finished near 4.08-4.09% into 19-20 Feb, up from ~4.04% a week earlier; the front end was steady‑to‑firmer, leaving a modest bear‑steepening flavour. Cause → effect: uncertainty about any replacement tariff framework plus geopolitics nudged term premium and capped duration gains.

Commodities told a two‑part story. Oil firmed as U-–Iran risk stayed live: Brent ~US$71.75 and WTI ~US$66.24 by Friday, broadly +~10% on the month, a tailwind for Energy equities without breaking ranges. Gold edged higher as a measured hedge, ~US$5,106/oz by 20 Feb, helped by the geopolitical bid and only moderate dollar strength.

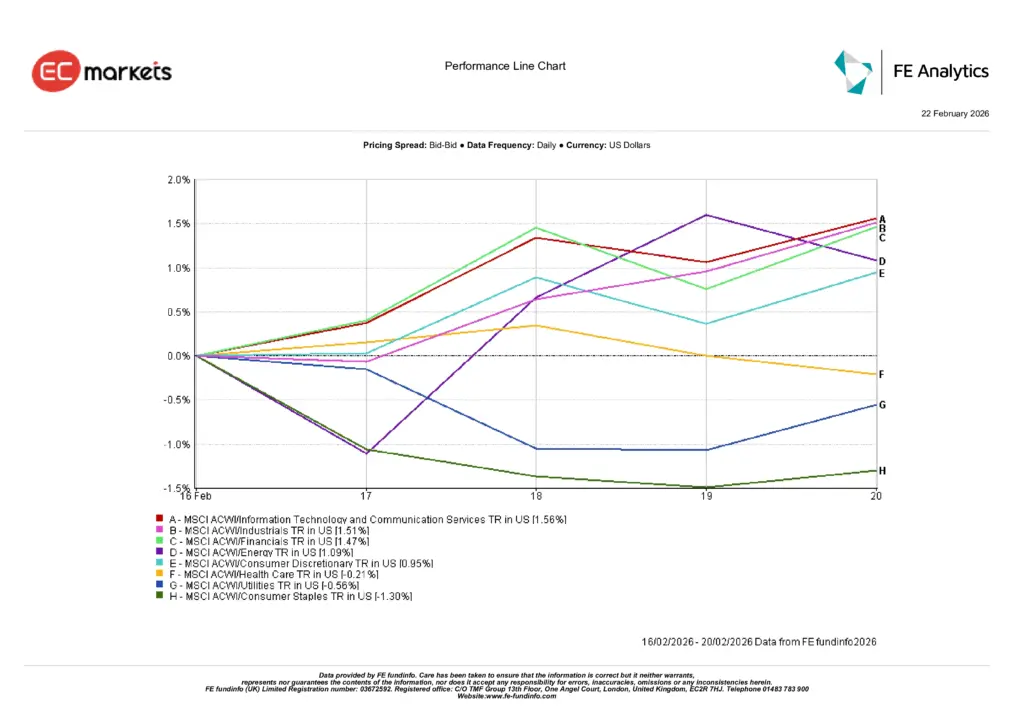

Sector Performance

Cause and effect were clear: the policy‑and‑geopolitics mix steered flows from defensives toward participation.

Information Technology & Communication Services (+1.56%) led as investors paid for earnings visibility even with yields a touch higher. Industrials (+1.51%) and Financials (+1.47%) followed, firmer activity tone and a slightly steeper curve helped, while Energy (+1.09%) rode the crude backdrop. Consumer Discretionary (+0.95%) gained as spending fears eased at the margin. On the other side, Health Care was roughly flat to softer, while Utilities (‑0.56%) and Consumer Staples (‑1.30%) lagged as the market rotated away from “safe and steady.”

Taken together, the week rewarded participation over protection, but with a continued preference for quality inside the cyclical tilt.

Sector Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 20 February 2026.

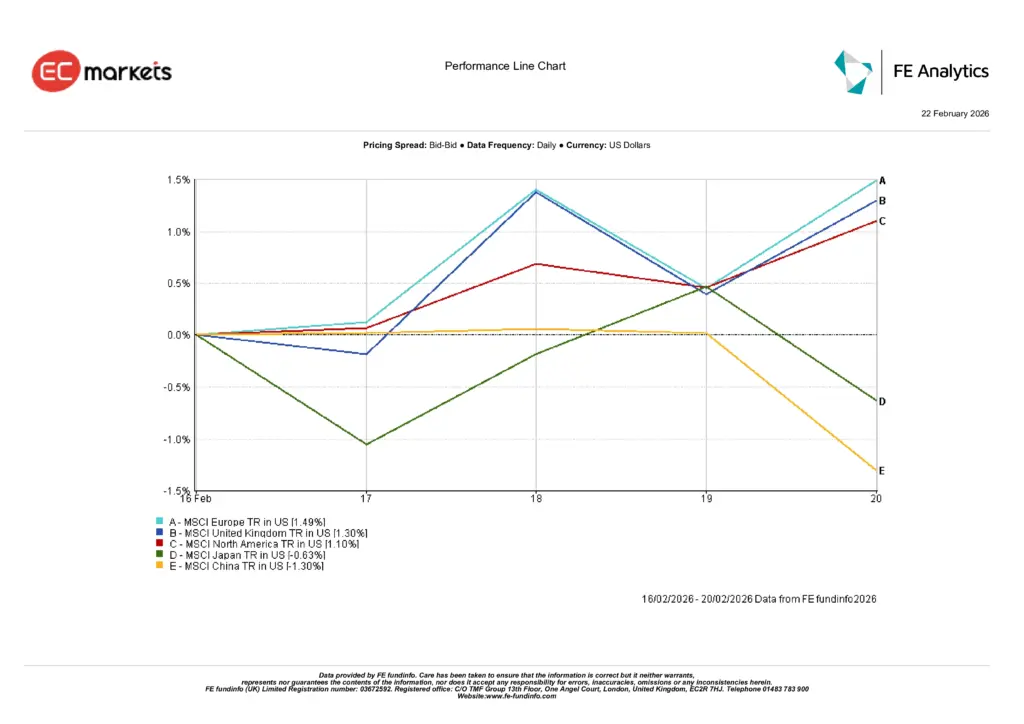

Regional Markets

Regional moves echoed the same selectivity. Europe (+1.49%) and the United Kingdom (+1.30%) led as ECB continuity and a supportive Energy tape helped, while North America (+1.10%) tracked the sector mix described above. Japan (‑0.63%) slipped as domestic data and a late‑week wobble clipped recent strength, and China (‑1.30%) remained a drag, keeping EM exposure selective, not sweeping. Cause → effect: steady policy communication plus an energy bid favoured Europe/UK; US leadership reflected the growth‑and‑cyclicals tilt; Asia underperformed where macro signals were less forgiving.

Regional Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 20 February 2026.

Currency Markets

FX echoed the risk mix and the rates bias. EUR/USD eased from 1.1851 (16 Feb) to 1.1782 (20 Feb); GBP/USD slipped from 1.3628 to 1.3484, moves that align with firmer US yields and modest dollar support rather than idiosyncratic euro/sterling shocks (per your screenshots). USD/JPY rose from 153.51 to 155.07 as higher global yields and a steadier risk tone pressured the yen, while GBP/JPY hovered near 209.10 (vs 209.25), confirming that sterling softness was dollar‑led rather than broad. Cause → effect: bear‑steepening and geopolitics lent the dollar a hand; yen weakness tracked rate differentials.

Outlook & The Week Ahead

The coming week looks less about headline surprises and more about how markets absorb rule‑making and risk‑pricing. If tariff implementation shifts from courtroom drama to clearer, narrower frameworks, and if U-Iran headlines stay in “posture, not action” territory, the measured rotation toward growth‑linked areas can persist, especially where earnings guidance is credible.

Conversely, a sharp escalation or a materially stickier higher‑for‑longer rates path would likely re‑energise defensives and test the recent leadership.

Practically, the message is unchanged: stay patient, stay quality‑focused, and let cause and effect do the work, use pullbacks to upgrade what you own, and size cyclical exposure to the level of policy clarity you actually have, not the clarity you’d like.