Oil Spike Extends Inflation Repricing as Markets Lean into Energy Hedges | Weekly Recap: 09-13 March 2026

Global markets spent the week repricing inflation risk as an oil spike triggered a defensive rotation across equities, bonds, currencies and commodities.

Economic Overview

Markets spent the week working through the second phase of the energy shock. Brent spiked intraday toward 119 early on and then eased, which kept oil as the dominant macro variable shaping both inflation expectations and interest‑rate pricing. The move was supply led through disrupted Middle East shipping, and it rebuilt “higher for longer” expectations as investors leaned into energy hedges and reduced exposure to duration sensitive assets. The cause was a supply side shock through the oil channel. The effect was tighter financial conditions as term premia rose and risk tolerance fell.

US macro data gave numbers but not a simple message. February CPI rose 0.3% MoM and 2.4% YoY, while core CPI rose 0.2% MoM and 2.5% YoY. These prints were in line with consensus and were recorded before the oil spike had time to pass through. The implication is that disinflation remains in place for now, but headline inflation may prove stickier if higher fuel costs feed into transport and goods prices. Initial jobless claims held at 213,000 in the week ended March 6, which points to low layoffs and a still stable labour backdrop. University of Michigan consumer sentiment slipped to 55.5 in the preliminary March reading as households cited higher gasoline and uncertainty. Together this suggests the economy is not rolling over, but the energy impulse raises the risk that policy easing is delayed if second round effects build.

Outside the US, policymakers stayed cautious. Europe is balancing fragile growth with imported energy risk. The United Kingdom remains sensitive to fuel costs given weak momentum. Across Asia, Japan is monitoring currency volatility and rate spillovers, while China is signalling flexibility to support demand if external shocks persist. The simple hierarchy held. Oil is the transmission channel through which inflation expectations, policy credibility and risk appetite are being recalibrated.

Equities, Bonds and Commodities

Equities traded through the week with a clear risk budget constraint. Markets attempted brief stabilisation rallies early in the week, but these faded as oil prices and sovereign yields moved higher. By Friday, the S&P 500 had declined about 2.4%, the Nasdaq fell about 2.6%, and the Dow Jones lost about 2.5%. The cause was the repricing of inflation premia through higher oil prices. The effect was renewed pressure on equity valuations as higher discount rates and reduced risk tolerance weighed on the major indices.

Rates markets absorbed the shock mainly through the inflation channel. Investors rebuilt term premia linked to inflation uncertainty, pushing the US 10-year yield from about 4.13% to around 4.29% and the 2-year from about 3.59% to near 3.73%. Germany’s 10‑year Bund yield and UK 10‑year gilt yields also rose. The cause was a shared inflation impulse through higher energy prices. The effect was tighter financial conditions and a more cautious tone across rate sensitive equity sectors.

Commodities remained the centre of gravity. Brent crude saw extreme intraday volatility, spiking above 119 early in the week before retracing to finish near 103.14. WTI followed the same pattern, ending near 98.71. The cause was geopolitical risk linked to disrupted supply routes and shipping flows in the Middle East. The effect was a persistent inflation premium across markets. Gold traded with less conviction. Although geopolitical stress normally supports safe haven demand, a stronger dollar and rising real yields offset that impulse, leaving gold slightly lower overall despite notable swings.

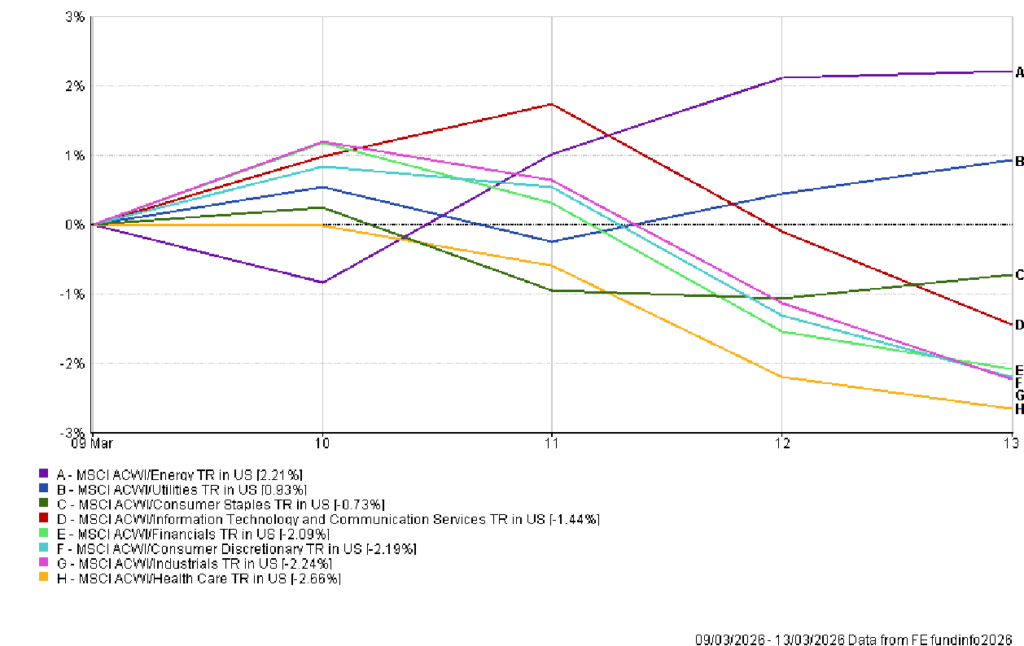

Sector Performance

Sector leadership during the week reflected the market’s attempt to hedge inflation risk rather than embrace cyclical growth. Energy was the clear outperformer, rising roughly 2.2% on the MSCI ACWI sector index. The cause was the surge in oil prices. The effect was investor rotation into companies with direct commodity exposure and cash flows linked to higher energy prices.

Utilities also delivered modest gains of around 0.9%. In an environment where inflation uncertainty and volatility increase simultaneously, investors tend to favour predictable cash flows and regulated earnings structures. Utilities therefore benefited from the broader defensive rotation.

Most other sectors acted as funding sources. Industrials fell roughly 2.2%, reflecting concerns about higher input costs and slowing global demand. Consumer Discretionary dropped around 2.2% as rising fuel prices threatened household spending power. Financials declined about 2.1%, showing that higher sovereign yields did not translate into improved sentiment for banks when macro uncertainty increases.

Technology also softened, declining around 1.4%. The cause was the steady rise in long term yields that raised discount rates applied to future earnings. The effect was continued pressure on growth-oriented sectors that had previously benefited from lower rate expectations.

Health Care was the weakest sector overall, falling around 2.7%. In a broad market de-risking phase even traditional defensives struggled to outperform unless they offered a direct hedge against inflation. Energy therefore remained the dominant macro hedge.

Sector Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 13 March 2026.

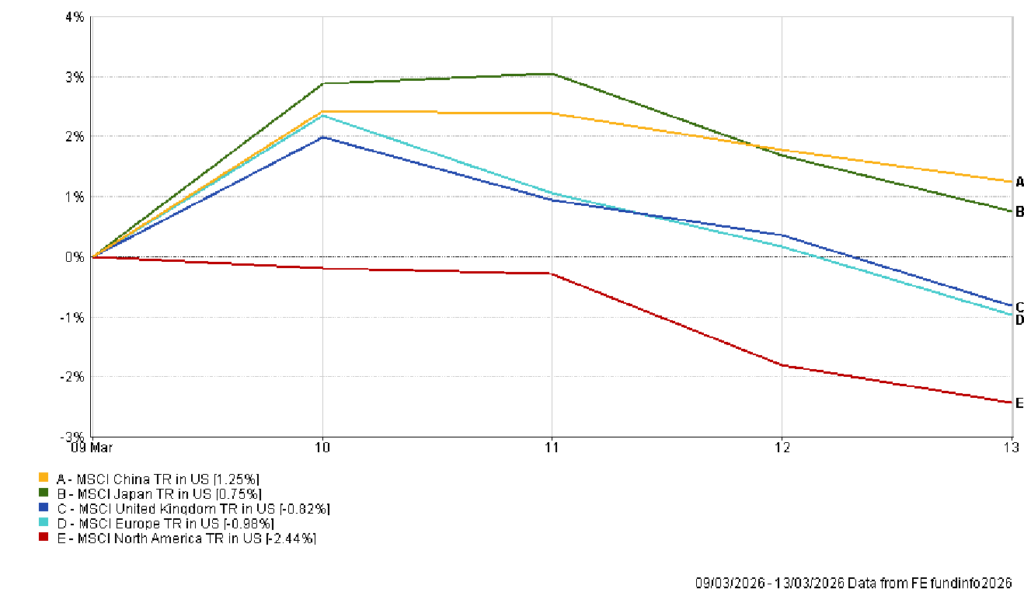

Regional Markets

Regional equity performance reflected a combination of energy exposure and currency translation effects. North America was the weakest major region, falling about 2.4% during the week as US equity indices declined in response to higher yields and inflation risk.

Europe and the UK delivered more stable local performances but still declined when measured in dollars. Europe fell roughly 1.0% while the UK declined around 0.8%. The cause was the strengthening of the US dollar. The effect was that relatively stable local equity performance translated into negative returns for global investors.

Asia was comparatively resilient. China rose approximately 1.2% during the week, supported by policy expectations and relatively lower sensitivity to the energy shock compared with Europe. Japan also gained about 0.7%, as local equities benefited from export sector resilience and supportive domestic policy expectations.

The regional pattern reinforced a clear hierarchy. Markets with stronger domestic policy support or lower immediate exposure to the energy shock experienced smaller drawdowns. Regions more dependent on imported energy faced deeper valuation adjustments as inflation expectations rose.

Regional Performance

Source: FE Analytics. All indices total return in USD. Past performance is not a reliable indicator of future performance. Data as of 13 March 2026.

Currency Markets

Currency markets provided one of the clearest expressions of the week’s macro shift. The US dollar strengthened broadly as investors sought liquidity and yield advantage. Rising Treasury yields and geopolitical uncertainty reinforced the dollar’s role as the global funding currency.

EUR/USD declined across the week, falling from around 1.1637 on Monday to roughly 1.1416 by Friday. The cause was the combination of stronger US yields and Europe’s energy vulnerability. The effect was sustained downward pressure on the euro.

Sterling followed a similar pattern. GBP/USD fell from approximately 1.3440 at the start of the week to around 1.3226 by Friday. Higher oil prices raised concerns about inflation persistence in the UK while the stronger dollar dominated global currency flows.

The Japanese yen weakened further against the dollar. USD/JPY rose from roughly 157.67 to about 159.73 over the week, reflecting widening rate differentials between the United States and Japan. Even traditional safe haven currencies struggled to compete with the yield advantage offered by the dollar.

Cross rates illustrated the same dynamic. GBP/JPY declined modestly across the week, reflecting the relative weakness of sterling despite the broader depreciation of the yen. The dominant trend remained dollar strength.

Outlook and The Week Ahead

The coming week will test whether markets can stabilise around the new inflation baseline implied by higher oil prices. If geopolitical tensions ease and supply routes remain stable, the inflation premium embedded in crude prices could gradually decline. That would allow sovereign yields to stabilise and equity markets to rebuild risk selectively.

If the energy shock persists, the repricing across rates and equities may extend further. Higher oil prices raise the probability of second round inflation effects through transport and production costs. The cause would be sustained supply disruption. The effect would be continued pressure on central banks to maintain restrictive policy settings.

Policy decisions will therefore remain the central focus for investors. The Federal Reserve meeting scheduled for 17-18 March will update economic projections and provide guidance on how policymakers interpret the energy shock relative to recent disinflation progress. In Europe and the UK, investors will be watching for signals that policymakers are prioritising inflation credibility despite fragile growth momentum.

The broader question for markets is whether the current episode proves temporary or structural. If energy volatility fades, the disinflation narrative could reassert itself. If it persists, markets may remain locked in a cycle where oil prices drive inflation expectations, sovereign yields and risk appetite simultaneously.