Q2 2026 Global Market Review: Key Trends, Performance and Outlook

This Q2 2026 Global Market Review examines how financial markets performed during the second quarter as easing inflation, resilient corporate earnings and changing central bank expectations shaped investor sentiment.

Few quarters have demonstrated how quickly market leadership can change quite like Q2 2026. After beginning the year dominated by rising energy prices, inflation concerns and defensive positioning, investor sentiment shifted decisively as commodity prices retreated, inflation moderated, and enthusiasm surrounding artificial intelligence reignited risk appetite across global markets.

Equities rebounded strongly, led once again by technology and communication services, while fixed income delivered positive returns as investors increasingly anticipated a more accommodative monetary policy environment. Commodity markets experienced a reversal, with oil recording one of its sharpest quarterly declines in recent years, while traditional safe haven assets such as gold also retreated as investors rotated back into risk assets.

Although geopolitical tensions remained present throughout the quarter, markets increasingly focused on improving economic fundamentals rather than downside risks. The result was a broad-based rally across developed markets, supported by stronger earnings expectations and continued investment in digital infrastructure and AI.

Macroeconomic Landscape

United States Economy

The US economy remained resilient throughout the second quarter despite ongoing uncertainty surrounding the Federal Reserve’s policy outlook. Inflation continued to moderate as lower energy prices helped ease headline inflation, while core inflation also showed signs of gradually cooling. The labour market remained healthy, with unemployment staying low and wage growth supporting consumer spending, although hiring momentum softened compared with earlier in the year.

Financial markets increasingly priced in the possibility of Federal Reserve interest rate cuts later in 2026 as inflation moved closer towards the central bank’s target. At the same time, corporate earnings continued to exceed expectations, reinforcing confidence that the US economy could achieve a soft landing without entering recession. This combination of resilient economic activity, improving inflation dynamics and easing policy expectations provided a supportive backdrop for both equity and fixed income markets.

European Economy

Economic conditions across Europe improved modestly during Q2 as easing energy prices helped reduce inflationary pressures across the region. Lower input costs provided relief for manufacturers, while household purchasing power gradually improved as inflation continued to moderate. Although economic growth remained relatively subdued, business sentiment strengthened as expectations for a more accommodative European Central Bank policy environment increased.

Manufacturing activity showed early signs of stabilisation after several weaker quarters, while the services sector continued to underpin overall economic growth. European financial markets responded positively, with improving earnings expectations and greater confidence supporting stronger equity performance across several cyclical sectors.

Asia & Emerging Markets

Economic performance across Asia and emerging markets remained uneven. Japan continued to benefit from robust corporate earnings, improving shareholder focused reforms and sustained foreign investor interest, making it one of the strongest performing developed markets during the quarter.

Across the broader region, demand for semiconductors, artificial intelligence infrastructure and advanced technology exports continued to support economic activity in markets such as Taiwan and South Korea.

China remained the primary area of weakness. Ongoing challenges within the property sector, subdued domestic consumption and cautious business investment continued to weigh on economic growth despite additional government policy support.

Elsewhere, emerging markets generally benefited from improving global risk sentiment, although performance remained highly differentiated and increasingly dependent on domestic economic conditions rather than broad regional trends.

Equity Market Recap: Growth Returns to the Forefront

Global equity markets staged an impressive recovery during Q2, reversing much of the weakness experienced during the first quarter. Investor confidence improved as inflation pressures eased, recession fears moderated and corporate earnings generally exceeded expectations.

The rally reflected improving inflation data, resilient corporate earnings and growing confidence that major central banks were approaching the end of their tightening cycles.

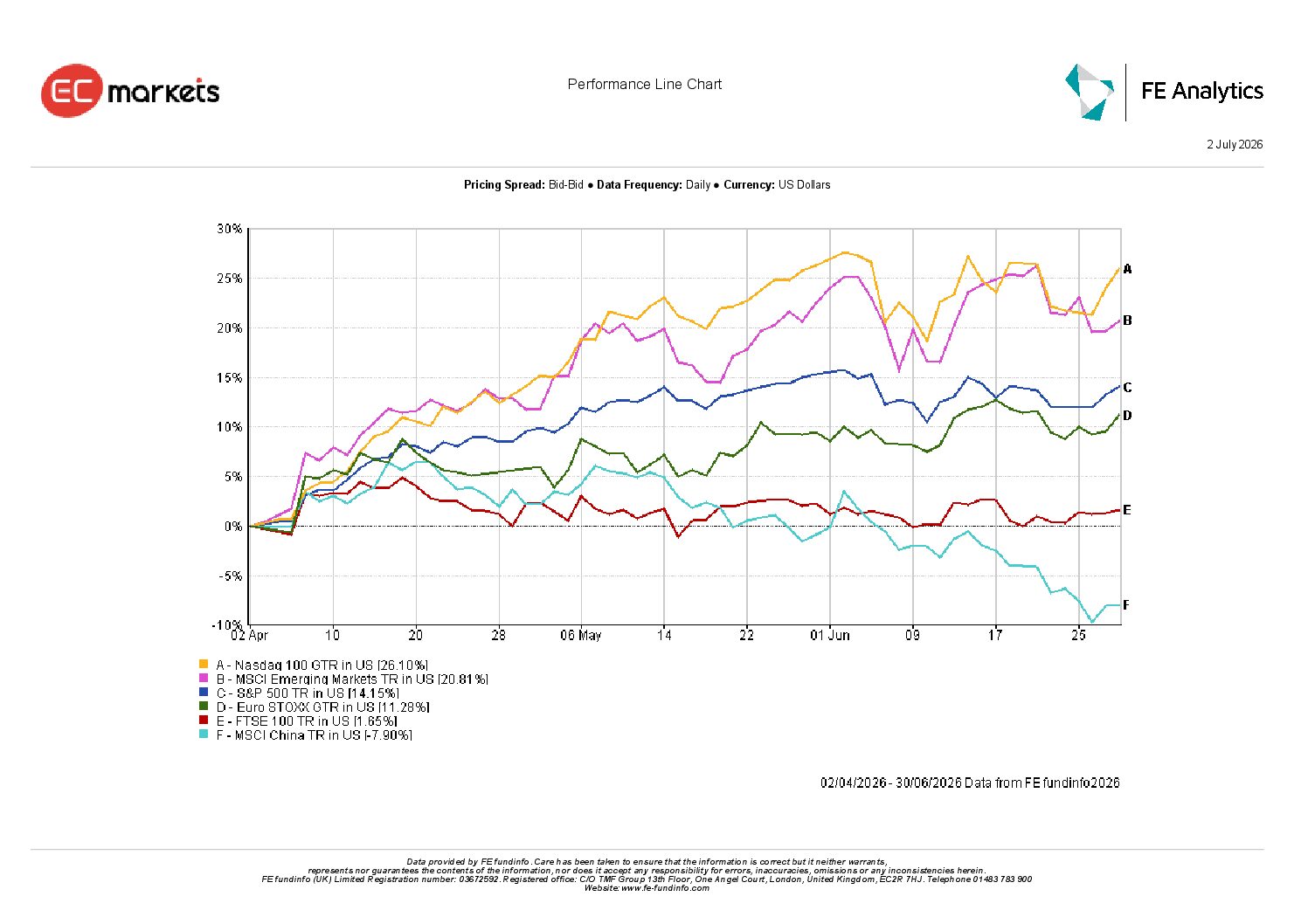

United States

US markets led global performance, with the Nasdaq 100 surging 26.10%, driven by renewed strength across mega cap technology companies and continued optimism surrounding artificial intelligence. The S&P 500 gained 14.15%, supported by broad participation across growth sectors.

Europe

European equities also delivered strong returns. The Euro STOXX index advanced 11.28%, benefiting from improving economic data and renewed investor interest in cyclical sectors, while the FTSE 100 posted a more modest gain of 1.65%, reflecting its heavier exposure to commodity related companies that struggled as oil prices declined.

Asia & Emerging Markets

Regional performance highlighted the growing divergence within Asia. MSCI China declined 7.90%, extending its period of underperformance as investors remained cautious over the country’s structural growth challenges.

The quarter also highlighted a broadening of market participation beyond the largest technology companies, with industrials and financials also contributing meaningfully to overall market gains.

Global Equity Market Performance, Q2 2026

Sector Rotation and Market Themes

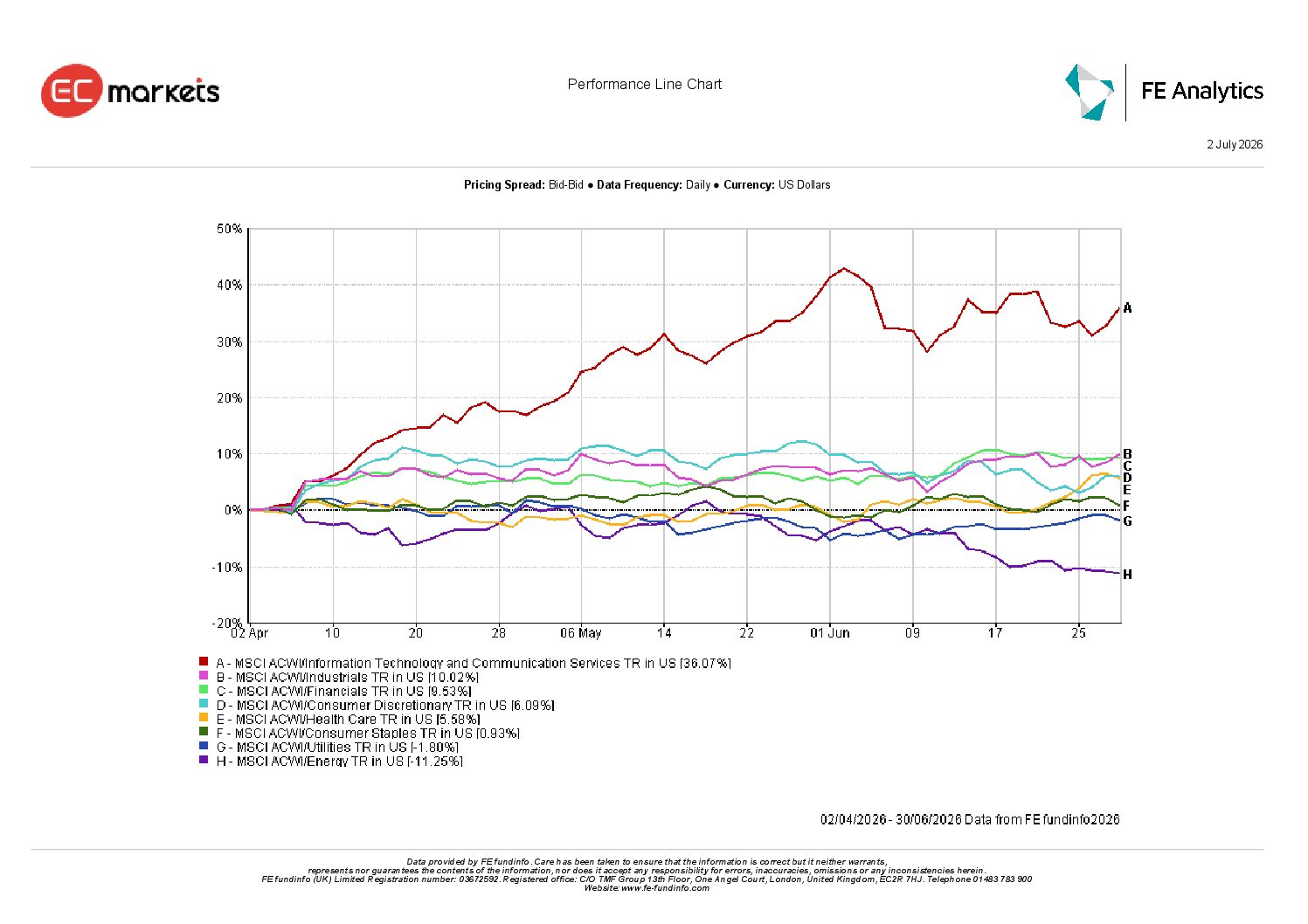

Technology Reclaims Leadership

Technology once again became the dominant market leader during Q2. The MSCI ACWI Information Technology and Communication Services sector delivered an exceptional 36.07% return, reflecting continued investment into artificial intelligence infrastructure, cloud computing and semiconductor technologies.

Strong earnings from several large technology companies reinforced confidence that AI driven investment remains one of the market’s most important structural growth themes.

Industrials and Financials Continue to Perform

Industrials gained 10.02% as improving business confidence and continued infrastructure investment supported global manufacturing activity.

Financials also advanced 9.53%, benefiting from resilient economic conditions, healthy credit quality and expectations that lower interest rates could support lending activity without materially impacting profitability. Consumer discretionary companies rebounded 6.09% as improving household confidence encouraged stronger spending.

Energy Gives Back Q1 Gains

The strongest reversal of the quarter came within the energy sector. Following exceptional gains in Q1, energy declined 11.25% as oil prices fell sharply amid improving supply conditions and reduced geopolitical concerns.

Utilities also underperformed, while consumer staples generated only modest gains as investors increasingly favoured higher growth opportunities over traditional defensive sectors.

Global Equity Sector Performance, Q2 2026

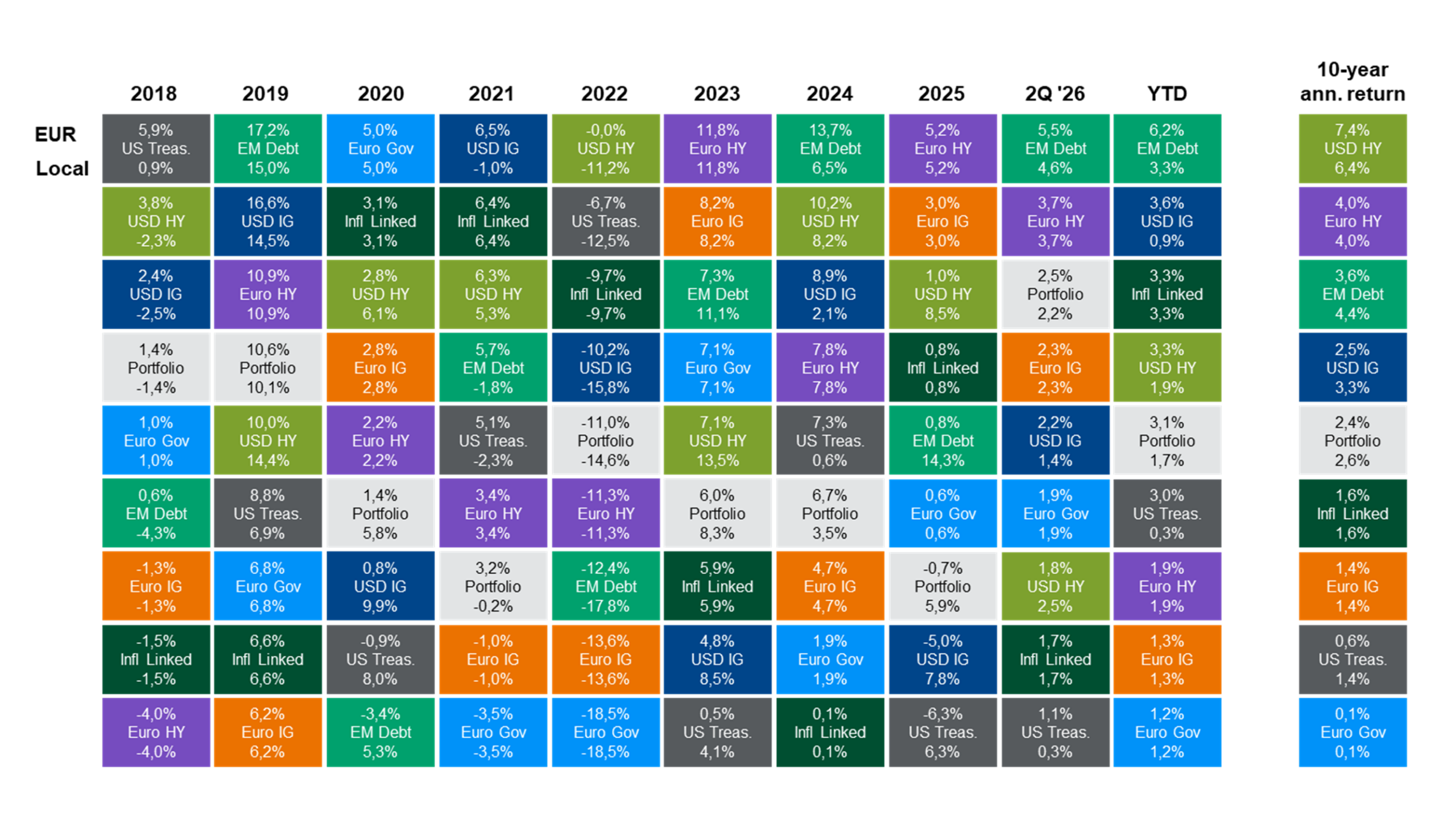

Fixed Income: Stability Returns

Bond markets delivered a more constructive performance during Q2 as moderating inflation and improving confidence around monetary policy supported demand for fixed income assets. Government bond yields generally moved lower during the quarter, producing positive total returns across several major markets.

European high yield bonds returned 3.7%, while emerging market debt gained 5.5%, making it one of the strongest performing fixed income segments. US investment grade credit also generated positive returns as tighter credit spreads reflected improving investor confidence and resilient corporate balance sheets. The recovery reinforced fixed income’s role as both a source of income and portfolio diversification following several volatile years for bond investors.

Credit spreads continued to tighten during the quarter as default expectations remained subdued and investor demand for higher yielding assets strengthened. Improving risk sentiment encouraged investors to move further along the credit spectrum, supporting both investment grade and high yield markets.

The return of positive bond performance marked a notable shift after the challenging environment experienced by fixed income investors during the previous two years.

Global Fixed Income Performance, Q2 2026

Commodities and Currencies

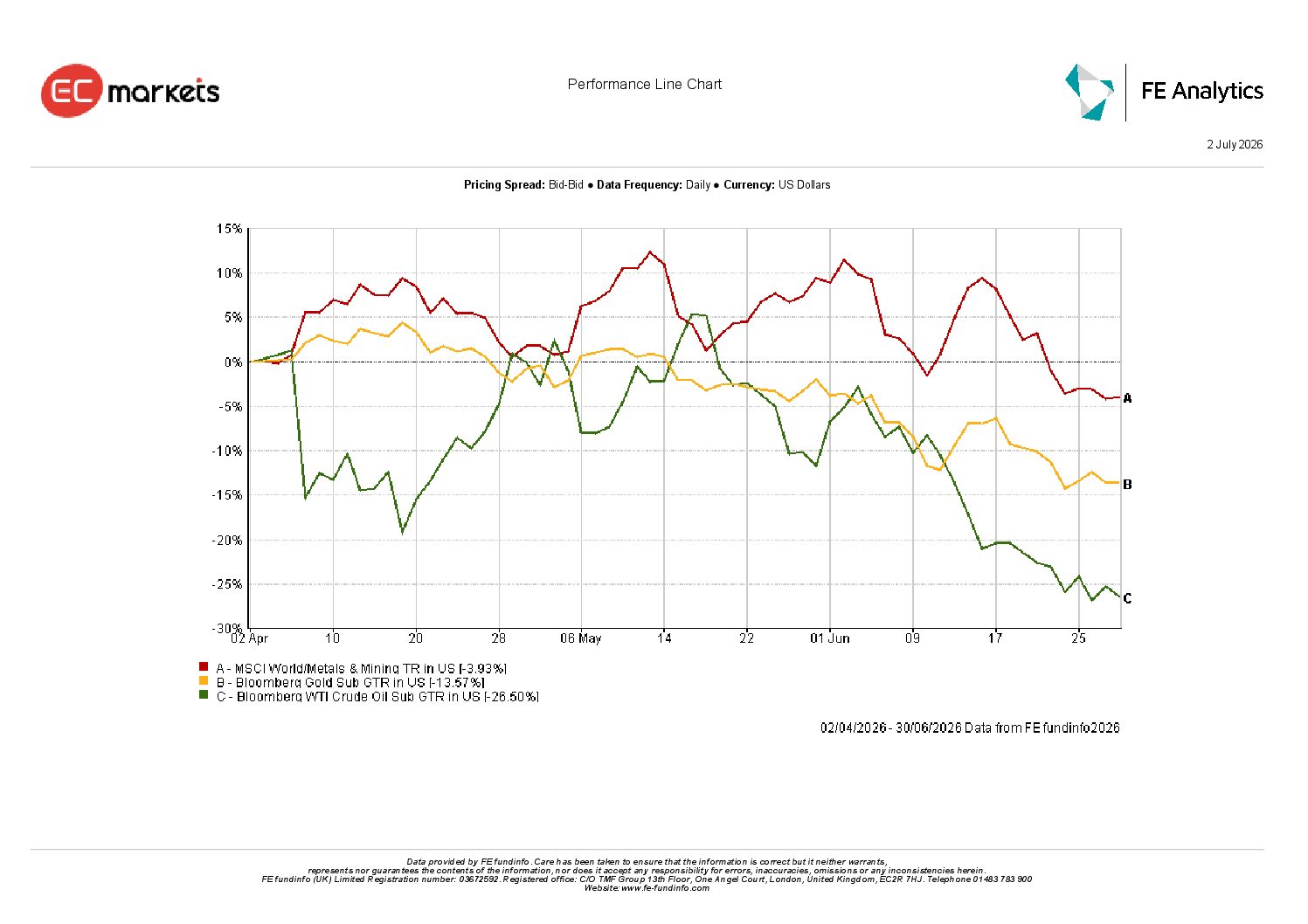

Commodity markets experienced a notable reversal from the previous quarter.

Oil

Oil prices fell sharply, with Bloomberg WTI Crude Oil declining 26.50% as supply concerns eased and geopolitical risk premiums unwound. The decline in energy prices also contributed to improving inflation expectations globally. The sharp fall in oil prices contrasted with the first quarter, illustrating how quickly market leadership rotated during 2026.

Gold

Gold also corrected, falling 13.57% as investors reduced allocations to defensive assets in favour of equities and other higher risk investments. Industrial metals proved comparatively resilient, supported by continued investment in technology infrastructure despite softer energy markets.

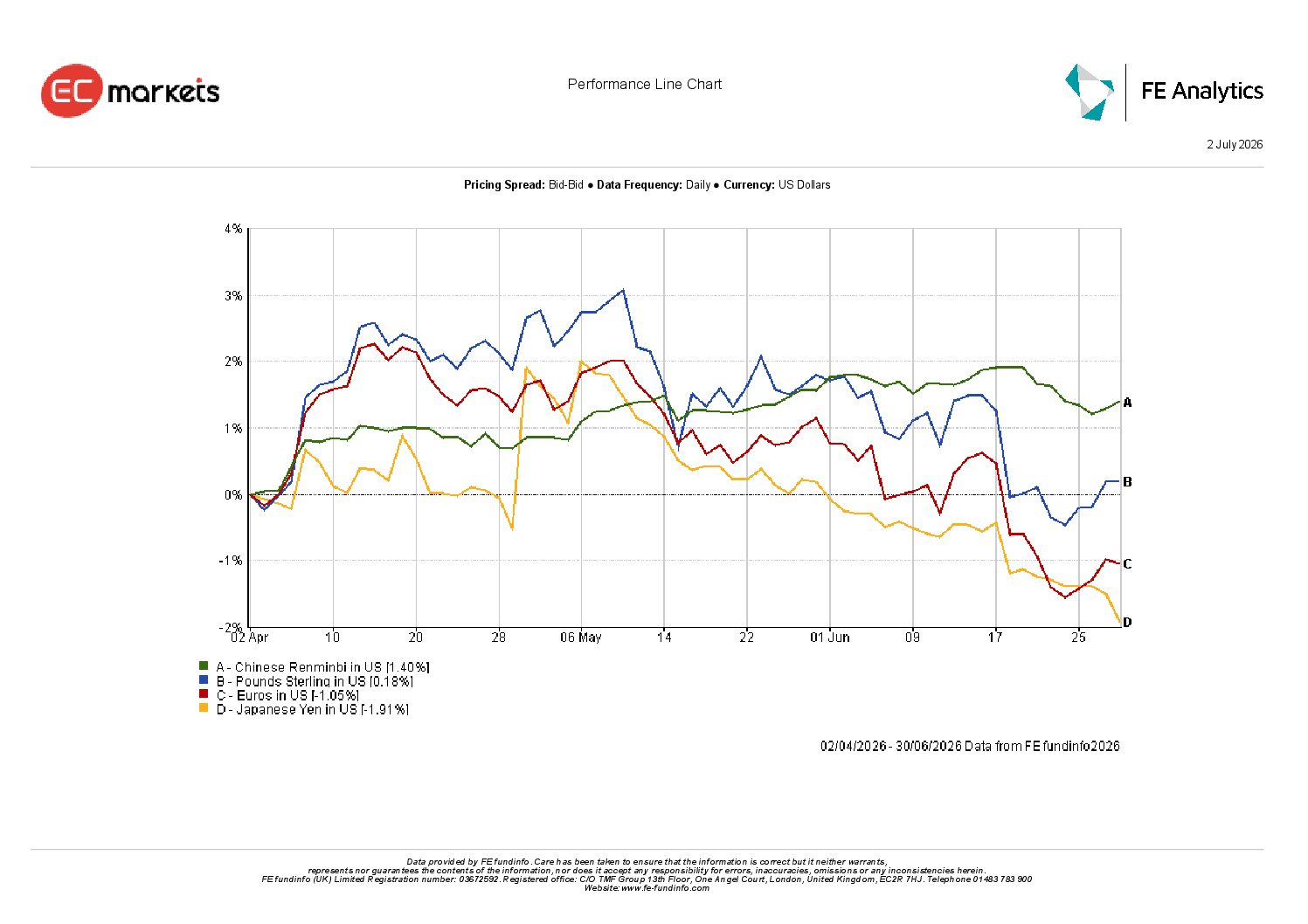

FX

Currency markets remained relatively stable. The Chinese Renminbi appreciated 1.40% against the US dollar, while Sterling finished broadly unchanged. The Euro weakened modestly, declining 1.05%, and the Japanese Yen remained under pressure as interest rate differentials continued to favour the US dollar. Overall, currency movements were relatively contained compared with the significant shifts seen across equity and commodity markets.

Commodity Market Performance, Q2 2026

Major Currency Performance, Q2 2026

Outlook and Positioning

As markets enter the second half of 2026, investor attention is expected to remain focused on three key themes: the trajectory of inflation, the timing and pace of central bank policy easing, and the sustainability of corporate earnings. While economic growth has proven more resilient than many anticipated at the start of the year, valuations have become more elevated following the strong rally, increasing the importance of earnings delivery over the coming quarters.

The continued expansion of artificial intelligence investment is likely to remain a powerful structural driver of equity markets. However, leadership may begin to broaden beyond the technology sector should economic activity continue to stabilise and borrowing conditions gradually improve. Industrials, financials and selected cyclical sectors could benefit from improving business confidence, while fixed income may continue to provide attractive income opportunities as interest rate expectations evolve.

Maintaining diversified portfolios remains essential. The sharp rotation witnessed between Q1 and Q2 serves as a reminder that market leadership can change quickly as macroeconomic conditions evolve. Investors should remain balanced across growth and value opportunities while maintaining exposure to high quality fixed income, which continues to offer both attractive yields and portfolio diversification.

Although risks remain, including geopolitical developments, trade policy uncertainty and the potential for inflationary pressures to re-emerge, the broader investment backdrop has improved. Lower energy prices, resilient corporate fundamentals and expectations of gradually easing monetary policy provide a constructive environment for long term investors.

Conclusion

The second quarter reaffirmed the resilience of global financial markets following a volatile start to the year. Falling inflation, easing energy prices and renewed confidence in corporate earnings created a more supportive backdrop for investors, allowing risk assets to recover strongly after a challenging first quarter. Technology once again emerged as the dominant market leader, fixed income regained momentum, and falling commodity prices helped ease inflationary pressures across major economies.

While regional and sector performance remained uneven, the quarter demonstrated the importance of maintaining a disciplined, diversified investment approach. Markets continue to reward companies with strong earnings, resilient balance sheets and exposure to long term structural growth themes, while areas facing persistent economic headwinds have continued to lag.

While uncertainty remains, the second quarter demonstrated how quickly market sentiment can improve when inflation moderates, corporate earnings remain resilient and monetary policy expectations become more supportive. Although investors should continue to expect periods of volatility, maintaining diversified portfolios and focusing on long-term fundamentals remains the most effective way to navigate changing market conditions.

Quarter 2 Market Outlook FAQs

Sources

This quarterly market review draws on publicly available market and economic data from recognised financial institutions and data providers, including: