為什麼現金流比盈餘更重要

投資人經常在評估公司時關注營收成長和每股盈餘。這些數字固然重要,但它們並不總能反映企業實際產生了多少現金。因此,有經驗的投資人往往會特別關注現金流。盈餘在帳面上可能很亮眼,但公司仍然需要現金來支付供應商、員工、利息成本和債務。在高利率環境下,這種區別更為重要。

盈餘與現金流並不相同

盈餘是根據會計準則計算的,包含估算、時間差異和非現金項目。相比之下,現金流則追蹤實際進出企業的現金。

這意味著公司即使報告有利潤,仍可能在產生現金方面遇到困難。例如,企業在完成銷售後可能就記錄了營收,即使客戶尚未付款。在損益表上,這筆銷售會提升盈餘,但在現金流量表上,這筆錢其實還沒進來。

這也是為什麼現金流通常能讓投資人更清楚地了解財務實力。它顯示利潤是否真正轉化為可用現金。

為什麼自由現金流很重要

自由現金流是指公司在支付營運成本並完成維持或擴展業務所需的投資後剩下的現金。簡單來說,就是公司在維持營運後可自由運用的現金。

這筆現金可以有多種用途。公司可以用來發放股息、回購股票、減少債務或投資未來成長。強勁的自由現金流讓管理層在經濟環境變得艱難時擁有更多彈性。

自由現金流也被廣泛認為是衡量企業質量最清晰的指標之一。會計盈餘可能受到估算和時間差異的影響,而現金產生能力則更能反映公司為股東創造價值的能力。

擁有強勁自由現金流的公司,通常更有能力維持股息、回購股票、減少債務,並在經濟低迷時持續投資。相反,現金產生能力較弱的企業可能需要增加借款或籌集額外資金。

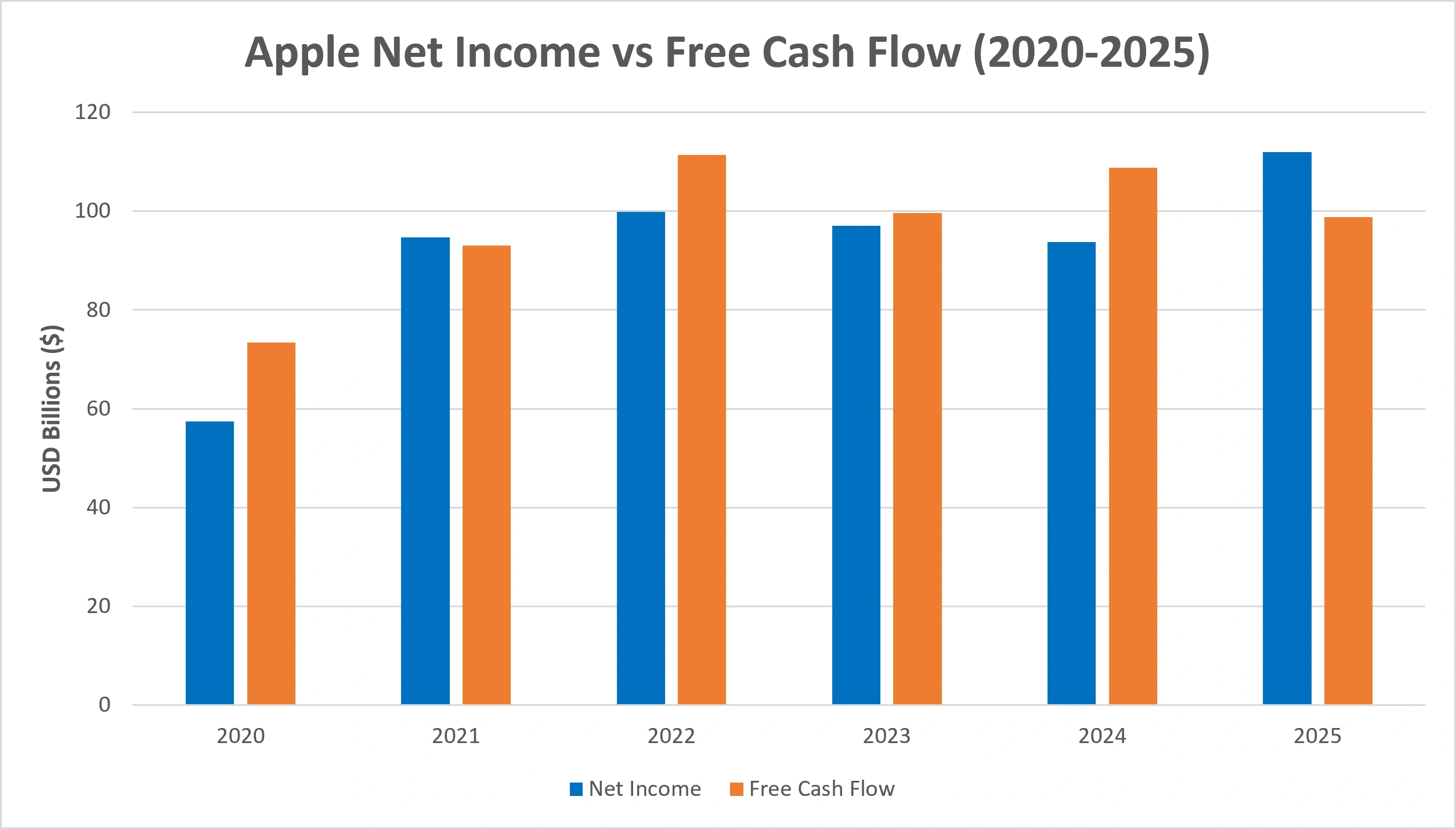

蘋果就是一個很好的例子。在2025財政年度,該公司產生了約1,115億美元的營運現金流,並在資本支出上花費了約127億美元,最終自由現金流約為988億美元。蘋果也透過股息和股票回購向股東返還了大量資本。

微軟同樣凸顯了現金產生能力的重要性。在2025財政年度,該公司產生了約1,362億美元的營運現金流。雖然資本支出因大力投資雲端和人工智慧基礎設施而上升至約646億美元,但自由現金流仍接近716億美元。

這些例子說明,強勁的現金產生能力能同時支持股東回報與未來成長的資金需求。

蘋果淨利與自由現金流(2020-2025)

資料來源:Apple Inc. 年度報告(2020-2025)。自由現金流計算方式為營運現金流減去資本支出。數字以十億美元計。過去表現不代表未來表現。

蘋果強勁的現金產生能力持續支持了投資、股息和股票回購。請注意2025年的變化,當時因AI基礎設施的高額資本支出,雖然淨利創新高,但自由現金流略有壓縮。

為什麼利潤與現金流可能不同步

盈餘與現金流不一定同步,因為企業運作存在時間差異。

公司今天可能賣出商品,但要過一段時間才收到款項。也可能在客戶購買產品前先建立庫存,或在投資產生營收前就大量投入工廠、技術或數據中心。

這些因素會造成報告利潤與現金產生能力之間的落差。公司看似有利可圖,但如果現金被綁在應收帳款、庫存或大型投資案中,實際上的彈性可能比盈餘數字顯示的要小。

例如,公司可能報告銷售成長強勁,但如果客戶要好幾個月才結清帳款,企業仍可能陷入困境。利潤看起來健康,但如果現金不足,企業仍可能面臨流動性壓力。

為什麼在高利率環境下這很重要

利率上升改變了投資人重視的重點。在低利率時代,市場往往願意支持即使尚未產生大量現金、但承諾高速成長的公司。

這種環境在2022和2023年各國央行為對抗通膨而升息後發生了變化。隨著借貸成本上升,資本取得變得更昂貴。投資人越來越重視獲利能力、資產負債表質量和穩健的現金產生能力,而不是不計代價的成長。

現金流之所以重要,是因為它能幫助企業保持韌性。能夠產生強勁內部現金流的公司較少依賴外部融資,通常更有能力在經濟環境變得艱難時持續投資、管理債務並支持股東回報。

獲利公司仍可能遇到困難嗎?

會的。獲利並不代表現金隨時可用。

公司可能報告正向盈餘,但如果客戶延遲付款、成本快速上升或債務到期,仍可能面臨流動性壓力。企業需要現金來應付日常支出。沒有足夠現金,即使是獲利公司也可能陷入困境。

這也是為什麼投資人常常比較盈餘、營運現金流和自由現金流。如果盈餘上升但現金流疲弱,這可能表示利潤沒有表面上那麼強勁。

為什麼負現金流不一定是警訊

自由現金流疲弱不一定代表有問題。年輕且快速成長的公司可能會刻意在當下大量支出,以支持未來擴張。

例如,投資於新數據中心、研發或技術基礎設施的公司,短期內自由現金流可能較弱。亞馬遜過去多年大舉投資物流中心和雲端運算能力,這些投資在後來才轉化為更強的獲利和現金產生能力。

關鍵問題在於這些支出是否創造長期價值。如果投資能支持可持續成長,短期現金流較弱是合理的。但如果反映的是營運資金管理不善、成本上升或需求惡化,投資人就有理由擔憂。

這也是為什麼現金流不應取代盈餘分析,而是應該兩者搭配使用。

重點總結

盈餘顯示公司根據會計規則取得的成果,現金流則反映公司實際擁有多少財務彈性。

對投資人來說,這個區別很重要。強勁的盈餘固然有價值,但強勁的現金產生能力才能顯示企業是否有資源投資、減債、發放股息並承受更嚴峻的經濟環境。

在高利率時代,現金流已成為衡量企業質量更重要的指標。它幫助投資人超越表面利潤,了解企業成長是否真正建立在堅實的財務基礎上。